By Philip Nothard

We have previously discussed how independent dealers are becoming ever more ‘scientific’ in their stocking policies. The days of just buying a ‘nice’ car at the ‘right’ price are gone. Many dealers are doing more research than ever to identify the cars that will sell best for them. That means understanding what customers are looking for, not just relying on what is available in the open market. The questions dealers are asking include:

|

||

|

Philip Nothard joined CAP in 2010 as its retail and consumer price editor, analysing pricing data and interpreting strategic market trends. In his role, he is able to apply two decades of experience gained in franchised motor retailers, which culminated in running dealerships for the likes of European Motor Holdings, Lythgoe Motor Group and Arnold Clark. |

||

♦ What are my customers driving?

♦ Do they want to change brand or just switch to a newer car?

♦ How much do they expect for their own car sale or part-exchange?

♦ What kind of price range will attract the most people?

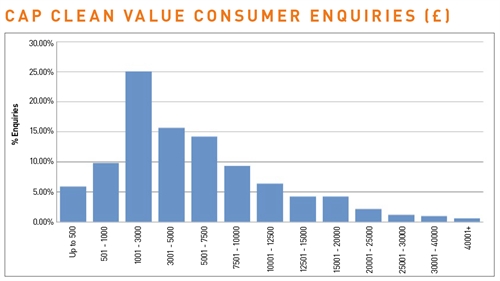

CAP collects data from consumers investigating their next vehicle purchase and our recent analysis indicated that one in four were looking to trade out of a car valued between £1,000 and £3,000 and more than half were looking to pay up to £7,500. It is hardly a surprise that the extreme ends of the value scale are hardly investigated at all. So, fewer than 1% are looking at cars valued above £40,000 and just 5% are interested in selling or buying a car under £1,000.

The majority are therefore looking at cars that average just over £4,000, which makes this ideal retail stock – when a reasonable margin is applied – for much of the independent dealer network.

More interesting data emerges from analysis of the specific brands and models that consumers are looking at.

It should be noted that there will always be a degree of curiosity underpinning some of the research conducted by consumers in the market, which means disproportionately high enquiries in relation to the values of the most prestigious models are filtered out in our analysis.

|

|

|

| Click graphs to enlarge |

What we then find is that consumer interest quite closely mirrors the new car market share of manufacturers, with Ford in the number one position and Vauxhall a close second. But after those two, it is the four big German brands – BMW, Volkswagen, Audi and Mercedes-Benz – that have the edge. Not only are these brands now mainstream in the new car sector, used car buyers also see them as a natural choice.

When I speak to dealer contacts, a common theme is that while they know what is generally popular, they are increasingly determined to filter this down to what is popular in their own market. This means understanding tastes in their own geographical region and whether or not it differs significantly from the national picture.

Looking across the UK network, the striking fact is the evenness of consumer tastes. There is very little variation in the level of demand or the types of car consumers are looking to buy. In short, it mirrors behaviour in the new car market. It therefore seems that the answer to the question ‘what should I be stocking?’ can be found by simply looking at what is popular everywhere and keeping an eye on the monthly registration figures.

Login to comment

Comments

No comments have been made yet.