Authors: Paul Daly and David Kendrick, partners at UHY Automotive

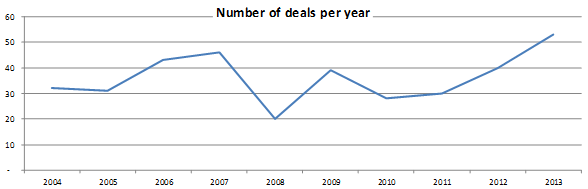

2014 saw a continuance of the buoyant market for transaction activity with certain businesses changing hands for record breaking sums. In this article we examine the factors behind this growth and consider the prospects for 2015. Firstly though, we will briefly consider the transaction market over the last 10 years.

The impact of the recession can be clearly seen with strong growth in the levels of activity from 2011 onwards. Figures to date in the current year (Sept 14) show 24 deals, perhaps indicating that volumes of activity will return to the long term average. However, as we discuss further below, we attribute this to a shortage of suitable businesses for sale rather than lack of appetite from those looking to acquire, and we expect 2015 to be a very busy year.

Analysis of the market

Whilst it is certain that volumes and prices are on the increase, understanding the factors driving this is far more opaque. When analysing the position, it is easier to consider both parties to any transaction.

The buyer

Buyers can be broadly categorised into five main segments:

• The large consolidators such as Lookers, Vertu Motors, Marshalls and Cambria. These companies have well-funded and low geared balance sheets through stock market fund raising or (in the case of Marshalls) significant wealth generated historically from other parts of the business. As a result these businesses have been present in the market throughout the recessionary period and have been responsible for the majority of deal activity in recent years. They appear to hunt with a pack mentality and recent focus has been firmly placed on the prestige brands such as Audi, BMW and Jaguar Land Rover as well as volume opportunities that are located in premises / towns with sufficient scale

Also of interest are recent announcements by Pendragon that it intends to once again commence an acquisition strategy, further increasing competition for the best businesses

• The medium size, fast growing businesses such as Ridgeway, Spire, Swansway, Vantage and Motorline. Such companies have aggressive acquisition based expansion strategies by virtue of strong manufacturer relationships, quality management and excellent access to funding. Similar to the large consolidators, such groups have continued to grow rapidly throughout the recent recession

• Other “Top 200” groups. Typically they have been relatively quiet through the recession and have looked to reduce gearing or focus on operational efficiencies rather than take unnecessary risks. Such buyers are now re-examining their strategies and concluding that maintaining the status quo isn’t really an option. Such buyers have increasingly returned to the market in 2014 and we expect this trend to gather pace in 2015

• The rest of the UK. Typically they will look to expand on an opportunistic or defensive basis (e.g. if a neighbouring territory becomes available). Again, these companies have “battened down the hatches” through the recession although they are starting to emerge again and consider acquisitions as profitability and cash generation improves

• Overseas buyers. Whilst low in volume, actual deal value is relatively significant for this buyer type. They typically view the market differently to the UK based buyer and will often value a business on a different basis as a result. There are no particular trends in terms of volumes of activity from this type of buyer although certainly the current instability in Russia and South Africa is generating interest with wealthy owners in those countries considering a safer home for their asset base

Overall then we are currently seeing strong appetite from all buyer segments and expect this to continue into 2015

The Seller

Considering the motivations of a seller is incredibly complex and in truth every situation will be different. However, we have tried to capture some of the characteristics and factors relevant to today’s market in our comments below.

In broad terms there are five types of seller:

• The strategic thinker. Typically a successful entrepreneur, the strategic thinker has been well advised over a number of years and groomed the business to its optimum position to maximise value. Whilst he or she will have defined a planned exit point that may be at some point in the future, they will consider marketing the business earlier if they feel market conditions are right

• Retirement sale. Typically a business held for many years and may be now feeling a little tired or neglected but with good potential to add value for a buyer. We have seen significant pent up demand for retirement sales and momentum continues to grow in this area. We believe this is due to delayed retirement plans that have been caused by the recession and an increasing perception that franchised motor retail is simply “no longer as much fun as it used to be” with the continuing increases in pressure and the necessity to hit volume targets

• No appetite for brand investment. At any point in time, a number of brands will be implementing a corporate identity refresh or more significant investment due to growth of the franchise. Whilst this is an ongoing process we feel that it is of particular importance moving into 2015 as brand expectations continue to increase as the market improves

• Smaller businesses with low return on investment. Increasingly, less sophisticated smaller businesses are changing their focus from return on sales to return on investment.

Continuing pressures from larger groups who benefit from stronger management, processes and economies of scale mean that achieving an acceptable return can be difficult even in the current strong market we are experiencing. This is causing smaller business owners to continually assess their relevance in the market place. This is of course a long standing phenomenon and we see no relief for the foreseeable future and the consolidation of the sector is inevitable although we do not see it’s pace increasing significantly

• Distressed sale. Throughout the recession, the majority of volume brand disposals represented distressed sales where effectively the business faced closure if it was not sold. In 2014, the volumes of this type of activity have fallen to very low levels and we do not anticipate this trend changing in 2015.

Overall then, we are seeing a continual supply of businesses coming up for sale, with some positive growth driven by retirement sales and investment avoidance offset by falls in the level of distressed sales.

Login to comment

Comments

No comments have been made yet.