By Philip Nothard

This year has been extraordinary for dealers, whether their principal focus was on new or used cars. Almost nothing about 2014 represented business as usual.

Sky-high new car business has been the biggest distraction for most of the year, but if you were trying to sell anything in Scotland, the September referendum killed business altogether for a time. Even the pattern of used car trade values has proved slightly different, with rapidly spreading alarm among dealers about how seemingly dramatic the trade and retail slowdown felt, when it came.

|

||

|

Philip Nothard joined CAP in 2010 as its retail and consumer price editor, analysing pricing data and interpreting strategic market trends. In his role, he is able to apply two decades of experience gained in franchised motor retailers, which culminated in running dealerships for the likes of European Motor Holdings, Lythgoe Motor Group and Arnold Clark. |

||

The response of dealers to the usual post-September slowdown has been particularly curious. At the end of November, my phone was ringing non-stop with dealers saying “Is it just me, or has the market gone off a cliff for everyone?”.

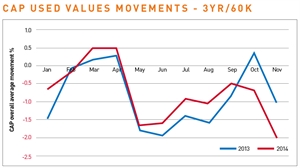

Yet analysis of trade values over the course of 2014 showed that, at the end of November, values were slightly ahead year-on-year. That represents a reduction (at three years, 60,000 miles) of 8.3%, compared with 9.4% to the same point in 2013.

Car dealers have become accustomed to a strong market

What seemed to be happening was that dealers have become so accustomed to a strong market that any softening in demand felt especially painful. There is also probably a psychological impact when the market does not perform as it did the year before, because everyone is now measuring performance more than ever before. So, as the chart shows, October of last year actually brought a modest increase in trade values while this year has not seen trade values increase since April. But, before we get carried away, the gap between values this year and last has rarely wandered wider than about one half of one percentage point.

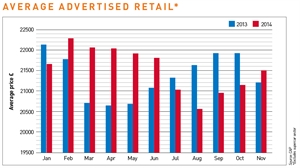

Possibly of more curiosity value has been the performance of advertised retail values. From February to June, advertised prices were ahead of last year by up to £1,500. But then the situation reversed in July, so that average advertised prices were almost £1,000 lower in August 2014 than a year before. Further work is required to identify whether these figures represent like-for-like vehicles – and therefore actual value changes – or whether there were simply more smaller, cheaper cars in the market.

However, the real elephant in the room for used car dealers is the relentless push of new product by manufacturers. For the first time, it really has become possible to argue to a consumer that they can be better off every month for buying a new car instead of a used one.

However, the real elephant in the room for used car dealers is the relentless push of new product by manufacturers. For the first time, it really has become possible to argue to a consumer that they can be better off every month for buying a new car instead of a used one.

One certainty about the coming year is further change. Dealers have fresh FCA legislation and the Consumer Bill of Rights to contend with, which means more time spent focused on compliance. All of this is against a backdrop of burgeoning PCP and PCH business, which is turning the traditional car buyer on to the concept of not owning a vehicle.

Perhaps only one thing is really guaranteed in this climate; the only area in which the used car specialist has total control is the experience they deliver to the customer. My view is that quality of customer service will become an even bigger differentiator for used car dealers than we know it already is.

Perhaps only one thing is really guaranteed in this climate; the only area in which the used car specialist has total control is the experience they deliver to the customer. My view is that quality of customer service will become an even bigger differentiator for used car dealers than we know it already is.

tjwiegand - 09/01/2015 17:04

My comment which I include here comes from a discussion within the "Loyalty Agent" LinkedIn Group of which Mr. Nothard is a valued member > http://tiny.cc/xkf7rx. I highly recommend everyone read this article of Philip's. It's important to YOU! The ending is most important, BUT don't start at the end, start at the beginning. It matters not that Philip is writing about UK facts. They apply everywhere. The "elephant" he speaks about is what it is, does what it does, and all must deal with it. After writing on facts and stating circumstances of business and the current climate of business, Mr. Nothard reaches an unexpected conclusion that most will overlook. I can’t allow you to overlook it, since it is the most important part of the article. He converts every challenging fact and figure of business to be resolved by YOU and me as persons! What? Yep! We, as human beings can better it all! You can Google this to validate my point, that we live today in the "Customer Experience Economy." Likewise, you should take a few minutes and Google: 'customer experience statistics.' The amazing thing you'll find is that EVERY “Customer Experience” statistic is B2C (Business2Customer). There are no statistics measuring "Person2Person Customer Experience." NONE! "So what," you say! Well, let's insert YOU, a person of business into all these B2C “Customer Experience” measurements, into proper context. YOU are nothing more than a COMMODITY! How do you like not being regarded as a valued human being? You are just a commodity within these statistics. Yet, here is Mr. Nothard matter-of-factly concluding the very real and necessary means of bettering everything is for YOU personally to quit being a commodity and become the highly valued Personal Brand you can be. But only you can convert yourself from a commodity to a trusted and valued Personal Brand that people freely choose to do business with, refer and recommend. Make no mistake, I am very pro business! Nevertheless, business concerns itself first and foremost on itself. And, when business exists to make a profit (which it deserves), placing numbers and money first as its form of existence, it leaves customers and team (you) secondary to the end result of money and profit. It's just a plain, hard, cold fact. Deal with it. Yes, yes, yes; deal with it, indeed! What I share here is not a threat in any way to business, but a major, major boost. YOU must commit to becoming a valued Personal Brand for your customers, prospects and yourself, representing the business you serve. When you do this your value will soar, both with customers and with the business you serve. No one, no business, can convert you from a commodity to a highly valued and respected Personal Brand but YOU. If you commit to convert your future is very, very bright no matter what any elephant does, and the business you serve will be stronger and better for it! Thank you, Mr. Nothard. Well written and very timely!