Ridgeway Garages, the Newbury-based premium brand dealer group, has been sold to Marshall Motor Holdings (MMH) for £106.9 million.

Marshall chief executive Daksh Gupta knows Ridgeway well, having briefly been its managing director in 2008 before joining Marshall when he retained a non-executive role on its board.

He said this is the biggest deal in the sector for more than 10 years - and the fourth biggest ever behind the acquisitions of Vardy, CD Bramall and EMH (see below).

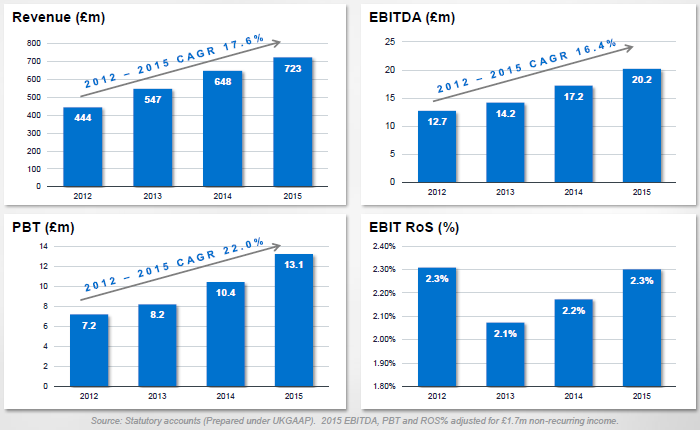

Ridgeway is a £722.6m turnover multi-franchise dealer group operating across the affluent southern home counties of England, Wiltshire and Dorset, representing 12 brands via 30 franchised dealerships.

Its brands comprise: Audi, BMW/Mini, Jaguar, Land Rover, Maserati, Mercedes-Benz cars and commercials, Skoda, Smart, Volkswagen cars and Volkswagen commercial vehicles.

In addition, Ridgeway operates five own branded Select multi-brand used car centres, two trade parts specialists, two service centres authorised by both Saab and Seat and two standalone bodyshops and a PDI centre.

Headed by chairman David Newman, chief executive John O'Hanlon and finance director Dan Taylor, Ridgeway’s consolidated FY15 revenues were £722.6m, adjusted EBITDA was £20.2m and year-end shareholders’ funds were £55.4m including £15.2m of net debt.

Newman and O'Hanlon have stepped down following the sale, however Taylor has transferred to Marshall.

Investors seem to approve - Marshall Motor Holdings share price increased by 22% following the announcement.

Gupta said: "This is a significant strategic and value enhancing acquisition for MMH that will move us from the 10th to the seventh largest UK motor dealer group.

“The acquisition, which is in line with our stated strategy at IPO to grow scale with existing brand partners, further builds on our acquisition last year of SG Smith by cementing our geographic footprint into the affluent southern home counties of England, Wiltshire and Dorset.

“We have funded this acquisition from our existing balance sheet capabilities. The board expects the acquisition of Ridgeway to deliver significant earnings enhancement and returns materially greater than our weighted average cost of capital.

“Ridgeway is a company I have been associated with since 2007. David Newman and his team have built an excellent business with fantastic senior management, great staff, strong performance and a similar culture to MMH.

On implications for staff, he said: "Our stock level goes up 60%, so we can offer customers more choice, there will be more opportunites for career development - it's good news for the Ridgeway and MMH teams. Lots of what Ridgeway does is first class - such as its social media presence - and we will take what each party does best and roll them out across the new expanded business."

“I very much look forward to welcoming our new Ridgeway colleagues to the group and working closely with them again into the future. Finally, I wish to thank all of the OEMs who Ridgeway represent for their support of the acquisition."

The Ridgeway name will be retained for the short-to-medium term Gupta said, before the Marshall name is rolled out across the acquired sites in 2017/2018.

Marshall chief financial officer Mark Raban summed up the significance of the scale of the deal: "This is massively significant in its earnings per share potential since we're adding an business that from a profitability perspective is not that far off Marshalls. Last year we made £23m EBITDA, Ridgeway just over £20m. So, it is almost doubling our earnings. It is transformational in terms of shareholder benefit."

The positive outlook on performance, he said, was based on Ridgeway as a respected brand, in "great" locations, with over 2% return on sales.

"The way we're funding this is also important," Raban said. "We funded a large proportion of the acquisition off our own balance sheet, through releases of equity, in stock and also within our leasing book."

Taking into account the amount of capital on its balance sheet, following its IPO, Marshall's return on capital employed was just under 10%. In 2017, Raban said it will be more than 20%.

There will be some management changes at Marshall: John Head, operations director at Ridgeway, becomes commercial director and Jamie Crowther, while continuing as operations director, relinquishes his commercial responsibilities.

Gupta resigned as a consultant to Ridgeway before negotiations got underway seven months ago.

Ridgeway financials (FY2015)

Revenue: £722.6m

EBITDA: £20.2m

Shareholders' funds: £55.4m (net debt £15.2m)

> Ridgeway's financial history

> AM reveals the new AM100 next month

> The biggest deals in the sector

Pendragon acquired CD Bramall plc in February 2004. Pendragon paid £231.5m for the whole of the issued share capital. CD Bramall had turnover of £1,763m in 2003, RoS of 1.7 % and EBITDA of £51.2m. CD Bramall employed 5,997 people.

Pendragon acquired Reg Vardy plc in February 2006 after a number of offers and counter offers, in competition with Lookers.

Pendragon ended up paying £504.2m for 97 franchised outlets. Vardy had turnover of £1,718m in 2005, RoS of 2% and EBITDA of £58.6m. Reg Vardy employed 5,551 people.

Inchcape acquired EMH in January 2007 for £262.9m. EMH had turnover for 2006 of £754.9m, RoS of 2.4% and EBITDA of £25.3m. EMH employed 2,176 people.

MMH locations and Ridgeway locations

MMH and Ridgeway combined location map

Ridgeway financial summary

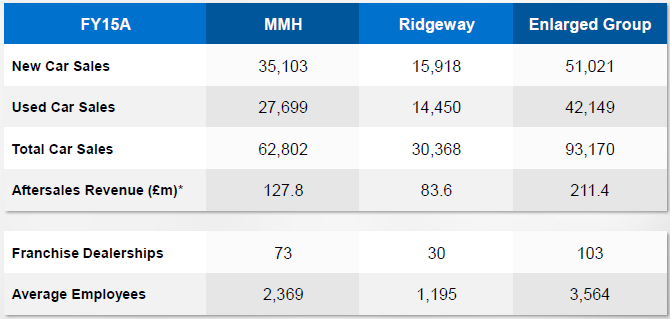

Ridgeway sales performance

As editor, Tim is responsible for the media content, planning and production of AM's multiple channels (AM print and digital magazines, website, social media and contributing to our events planning). He interviews and writes about as many franchised dealer groups and UK divisions of motor manufacturers as possible, to explore the issues facing UK motor retail and understand what solutions dealers and suppliers are using to overcome these.

Login to comment

Comments

No comments have been made yet.