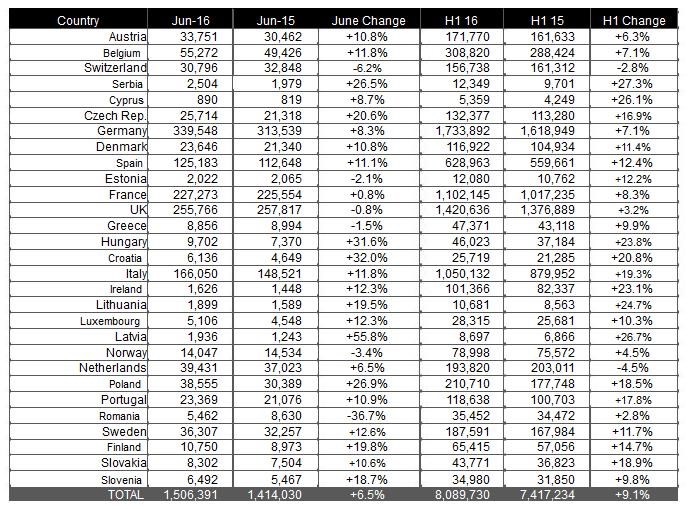

The European new car market increased by 9.1% to 8.09 million units over the first six months of this year, the highest level since the first half of 2008.

According to the latest monthly figures from JATO Dynamics, the growth was down to stronger economic conditions, new products and continuing shifts in consumer taste.

While the registrations were up for the first half, June’s figures showed a slowdown in growth, at 6.5% compared to 15% in May.

JATO said the uncertainty caused by Brexit led to UK new car market growth slowing in June.

Of the big five European markets, Germany was the biggest, posting 7.1% growth over the first half of the year and 8.3% in June. Both Spain and Italy posted double digit growth over the first half of the year and in June, while France saw growth of 8.3% over the first six months and then a flat market in June.

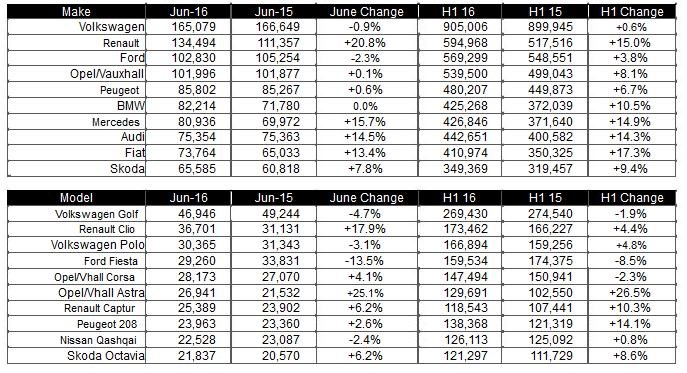

Not all manufacturer brands benefitted equally from the overall growth seen in H1.

Most mainstream brands lost market share, underperforming against the average growth rate especially Volkswagen (+0.6%) and Nissan (-1.5%).

Volkswagen has seen its market share fall almost one percentage point, due to diesel and emissions issues, from 12.1% in H1 2015 to 11.2% in H1 2016, which is their lowest H1 market share since 2010.

Felipe Munoz, global automotive analyst at JATO Dynamics, said: “Volkswagen is not only dealing with the emissions problem but also the brand’s top-seller - the Golf - is well established, while its rivals continue to overtake it with newer products.

“In contrast, Renault’s registrations grew by 15%, making it the second largest car brand in Europe and clearly outpacing its mainstream rivals; Ford, Opel/Vauxhall and Peugeot – who all posted market share losses.”

Fiat was the other big mainstream brand to gain ground during H1, mostly due to good results in its home market, along with good sales momentum from its five year old Panda and the 500X mini SUV.

Audi, Mercedes and BMW were ahead of Fiat, with all of them posting double-digit growth, and with Mercedes outselling BMW. Hyundai and Kia were the also improvers among the top 20.

Other successes included Mazda, Land Rover, Honda, Jeep, Jaguar, Ssangyong, Abarth and Infiniti.

Market trends

The market continued to shift towards SUVs, with the smallest ones – B-SUVs – grabbing the biggest part of the market share gain, from 8.3% share in H1 2015 to 9.4% in H1 2016.

B-segment cars lost the same amount of market share over the same period, going from 22.6% down to 21.4%.

Overall, SUVs accounted for 24.7% of the market and posted the second highest percentage growth at 24%, after the sport cars category which grew by 31%.

The markets with the biggest gains in SUV share were Cyprus, Ireland, Croatia, Hungary and UK. The brands whose SUV ranges gained the most were Bentley, Jaguar, Mazda, Suzuki and Honda.

The model ranking showed that most of the traditional market leaders posted very limited growth, while the latest launches, especially the new SUVs, were the biggest winners during H1.

The Volkswagen Golf was once again Europe’s best-selling car with 3.3% market share, which amounted to 269,400 units.

Their total was 2% lower than its result for the same period last year, which means that, along with the Hyundai ix35 and Ford Fiesta, it was the model that posted the biggest market share drop.

The Renault Clio, Volkswagen Polo, Opel/Vauxhall Corsa and Nissan Qashqai were the other leaders that underperformed against the market’s average growth. These models lost out to small SUVs like the Renault Captur, Peugeot 2008 and Fiat 500X, which all recorded double to and triple growth.

Munoz said the biggest changes are taking place in the SUV segment. He said small SUVs are becoming almost as popular as compact ones (C-SUV) due to their pricing and a greater amount of choice.

During H1, 40% of the SUV sales corresponded to C-SUVs, with B-SUVs just behind at 38.2% share. The fastest growing were the large SUVs (E-SUV) with 145,700 units, up by 30%. The Qashqai (+1%) was still Europe’s best-selling SUV, but its sales were impacted by the arrival of the Hyundai Tucson (which has almost 1% market share), the new Kia Sportage and the Renault Kadjar.

However, the Captur got closer to the Qashqai with its volume growing by 10%, despite the popularity gained by its rivals Fiat 500X, Suzuki Vitara and Jeep Renegade.

In the upper segments Volvo and the German premiums continued to dominate.

Munoz said: “These first half results show a healthy market that clearly favours new products and SUVs.

“The second half will be more challenging due to current uncertainty in the UK, and possible stagnation in other key markets. New launches with innovative solutions for the driving experience will become a key factor for success.”

JATO Dynamics sales by market/make/model

Author:

Tom Seymour

Freelance writer

Freelance writer for AM, Tom Seymour has been a specialist B2B journalist covering the automotive sector for over 14 years. He started his freelance career in 2015 and currently writes for a variety of automotive, business and technology publications.

Login to comment

Comments

No comments have been made yet.