As September draws to a close, the question is what will the second plate change of 2015 bring in terms of new car registrations?

By Rupert Pontin

At the eight-month point, on the back of 42 consecutive months of increases, one may be forgiven for believing all is well – with the year-to-date uplift in registrations currently standing at 6.7% there is definitely cause for celebration.

However, the reality is that there are more challenges in placing these new registrations into the market than one may imagine. Pre-registration is now an integral part of the process of moving excess European vehicle production into the hands of UK consumers and there should be no shame in acknowledging that this is both necessary and difficult to do.

To keep the flow of stock moving is more difficult for some manufacturers than others, depending on the age of their product or their current popularity with the consumer. The newest product offerings generally perform best, but there is little doubt it is effective marketing and pricing that make the difference.

The PCP is a fantastic medium for putting cars to the retail consumer, but the volume of low-rate finance and low deposit offers in place is increasing and will continue to do so in the coming weeks. The cost per month is key and today’s retail consumer is on the verge of being on the receiving end of what is likely to be a frenzy of outstanding offers as manufacturers seek to keep the sales figures above the level of 2014.

The scenario is really very interesting as the nation is on the cusp of beginning to feel the wider effects of the election of a Conservative Government.

There was never any secret that it intends to embark on a programme of further cost-cutting to drive down national debt. Equally, there is little doubt their positive and clear strategy has boosted economic confidence, although retail consumers may have a mildly different view in the coming months as they begin to understand what difference further austerity measures will make to their monthly finances.

Combine this position with a clear indication that bank interest rates are likely to start to increase in the short term and the next couple of months may see a temporary absence of consumers happy to commit to “big ticket” purchases.

Therefore, the market will become more competitive and more importantly there will be an increase in the volume of pre-registrations. This brings two questions, the first being how can we quantify this and secondly what will be the impact on the market and used values as a whole?

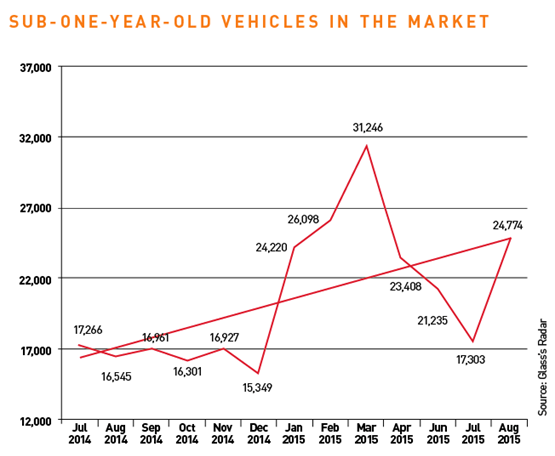

The table above gives an indication of what has happened so far in 2015 and details the number of sub-one-year-old vehicles available for sale by month during the course of the past 12 months. The data is from Glass’s Radar product.

What is immediately clear is that volumes are running considerably higher in 2015 than last year. In fact the volume in July 2015 is 43% higher than in the same period in 2014. There is also a clear change as the year rolled from 2014 to 2015, with a 57% increase in volume from December to January.

This increase of late-plate cars has put downward pressure on used cars at almost every age level and values have been falling faster this year across most sectors of the market than they have done for some time. This is very simply because there must be a financial gap between a new car, a pre-registered version, a true used car and then the same model as it runs back through the registration plates. Consumers have to be able to see “value” in older models, whether it be the front-end screen price or the monthly payment, and that can only be done by a reduction in values that is driven by the trade buyers.

Consumer confidence in the final quarter of the year will dictate what will happen to used values, but pre-registrations are a certainty as the manufacturers push franchised dealers to ensure that production volume to which they are already committed is vented into the market.

Login to comment

Comments

No comments have been made yet.