This autumn update of the AM100 takes place against the back-drop of a world heading into a sustained global slump.

For many, this will be their first experience of an economic shock-wave.

For others it will be the latest of a number, taking place with seemingly inevitable regularity once every seven to 10 years.

Most, if not all, economists and analysts accept that these cycles are largely man-made, but the impact on business and individual alike is no less real.

The numbers in the AM100 tables – turnover, return on sales (RoS), return on capital (RoCE) – reflect a world before the impact of the last three months.

Some of the numbers reflect the best estimate of how 12 months to the end of June 2008 have panned out. The rest show the actual outcome, as portrayed by statutory accounts, for 2007.

There are striking changes in the trends.

For years AM has reported on the emergence of a super-league.

We have also emphasised that, far from there being a trend of continuing growth and consolidation, the real numbers demonstrated a conflict between ambition and real difficulty in achieving economies of scale.

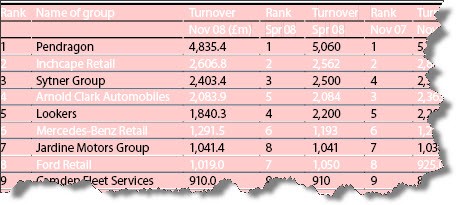

It is still true that in order to move from the bottom of the top 20 to the top 10, it would be necessary to take over a group of similar size to oneself.

However, the top 10 this time has dropped nearly a billion pounds in turnover since last year’s tables were published.

For some, this has been the result of closure of loss-making outlets; for others, it is the outcome of a rationalisation of brand and territory.

The actual top 10 has remained unchanged.

The biggest loser has been Pendragon.

The loss in turnover has been matched by a loss in profitability.

For Arnold Clark and Inchcape, reductions in turnover seem to have been more strategic and have not been matched by similar reductions in profits.

In fact, Arnold Clark has seen an increase in return on sales.

For Lookers, diversity in the aftermarket has cushioned the business from car sales issues.

Many commentators remark on the rapid and increasing pace of change in the consolidation of car retailing. The numbers show a different story.

The largest groups face a common problem – how to make a consistent and acceptable return on a hugely diverse base of different businesses.

They approach it in different ways.

Some indulge in portfolio churn.

Some refocus their investment priorities on chosen partners and particular geography.

The consistent picture is the success of the local heroes, champions of brand and demographics applying clearly defined capabilities.

It is increasingly difficult to deliver the latter and to be large scale. JCT600 defies that logic, remaining in the RoS table but, at the same time, slipping just outside the top 20 on RoCE.

Not all local heroes are successful, but those that are, consistently surpass their larger brethren.

Looking at the RoCE table it is interesting to note a new leader.

For years Porsche Retail seemed unassailable. However, Bramall & Jones has this time shown the way.

The management style of Tony Bramall and Peter Jones has been well documented in its attention to detail.

Deliver the basics every day, all day – these principles should be everyone’s mantra.

The rest of the RoS and RoCE tables show the familiar story.

Volume brand-based businesses such as Peoples, Lifestyle and Drive sit alongside prestige based businesses such as Meteor, Harwoods and Halliwell Jones in producing stronger than average returns.

Stoneacre continues its longest running presence in the RoS and RoCE tables although the brands and territories represented are not all from the obvious selection of high profit performers.

Westover, Ridgeway and RRG have increased scale by acquisition, but have not lost sight of the local hero formula and profit.

And so to the recession.

The next time the AM100 is published the picture is likely to be different.

Dealers who show a relentless attention to detail at a local level should feel the effects of the recession last, least and for potentially the shortest time.

One standout reason is loyalty created through consistently providing value to the customer.

Unfortunately, in a recession some businesses will need to reduce headcount.

And losing some jobs is always a better outcome than losing all jobs.

But this should be recognised for what it is – a strategy for short-term survival.

It should be a catalyst to a complete re-appraisal of every job and every process to ensure it adds to the value chain and maximises profit potential for the longer term.

To be at the head of the emergence from the recession, ask yourself whether you have a consistent and successful method for identifying and solving problems.

For example, understand exactly why you don’t retain more customers, and what needs to change to satisfy more of their requirements more often.

Then return to the people and headcount issue.

The winners from the AM100 tables will be those doing just that.

- This is an excerpt from an in-depth feature and update on the AM100 tables, looking at the largest dealer groups by turnover, in the November 14 issue of AM.

To subscribe to AM magazine click here or call 01733 468659.

Login to comment

Comments

No comments have been made yet.