The last two months have seen a distinct cooling in used vehicle values.

And after all we have said over the past year about the key to values being supply and demand it should come as no surprise that rising volume has played a key role in this.

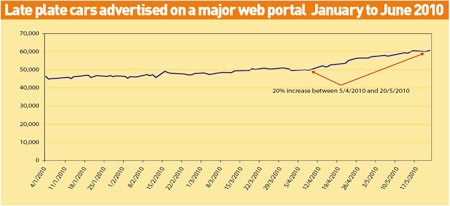

One of the clearest indicators of this has been tracked in the form of late plate vehicles entering the market for retail sale over the past six weeks.

We have measured a 20% increase in volumes in this important part of the market.

This appears to have proved a crucial tipping point after the rises of last year.

We have commented frequently that used car values had – in many cases – become unsustainably high.

In a fragile economy, besieged with consumer caution and political uncertainty, the only ingredient lacking for a downturn was oversupply.

It was always clear that late plate volume was crucial to the fortunes of the market overall.

This is because shortages in the popular nearly-new arena drive demand down through the age bands.

To put it simply, if you can’t buy this year’s plate and you want something as fresh as possible you will buy last year’s. That in turn sucks out volume there and buyers in that market have to look to slightly older cars and so on.

In all our commentaries during the early part of 2010 we inserted the caveat that things would change throughout the market if there was any substantial increase in late stock.

June’s Black Book reduction, averaging 4%, was in part driven by such a change indeed occurring.

Figures shared privately with CAP have shown that mass registrations on the last day of the month have again been taking place.

You can expect to see commentators using phrases like ‘the perfect storm’ if this continues because this has been happening at the same time as an influx of poorer condition cars at three and four-years-old – just as the extent of Government spending cuts pain is beginning to emerge.

The chart illustrates the increase in late plate volume by showing the rise in cars advertised on one major web portal.

For the stability of values it is to be hoped that this does not continue for long or reach the scale we saw before the downturn of 2008.

There have also been numerous observations that leasing vendors have been holding out for CAP Clean on cars which clearly fall below the ‘ready for retail’ standard that the label implies.

Such a policy requires an urgent sanity check because all it achieves is the build-up of greater volume, sparking even more caution among buyers.

On a positive note, we expect June to see three-year-old vehicle volumes returning to more manageable numbers.

But vendors will need to recognise that buyers now have a wealth of stock to pick and choose from, and set their reserves accordingly.

It takes a while for market changes to seep into the psyche, but it really is now time to recognise that today’s market is a very different beast than last year.

In the three years culminating in 2008, when values of 4x4 vehicle plummeted further than any other sector, there was a big question mark over whether there was a place any longer for this type of vehicle in the market.

The public perception of the 4x4 was that it was an expensive-to-run gas guzzler that always overlapped the parking space.

The Government also lined this sector up for some extra tax revenue – an easy target, even if some were built in the UK.

Strangely , the history books will tell a story of how these problems – culminating in the recession – actually helped the long-term future of this sector by leading to new strategic thinking.

In passing, the 2008 downturn also led to a big surge in demand when such vehicles became the proverbial ‘lot of car for the money’.

But the wheels had already been set in motion as traditional 4x4s suffered their bumpy downward trajectory from 2006.

Manufacturers were quick to realise that for this ever popular sector to survive long-term some fundamental changes would have to take place and by this I don’t just mean stop/start technology and lower CO2 emissions.

Something more radical was needed. It was delivered with the emergence of the SUV or sports utility vehicle in the UK

This sector swallows up all the established 4x4 models, but is led not by the larger models but by the compact versions like Nissan’s Qashqai and the Ford Kuga.

This style of vehicle has a very wide appeal. It has all the popular features of the 4x4 such as high driving position and the feeling that you are in a spacious, safe and robust vehicle.

These vehicles also boast great handling and agility. The customer perception is that they are more affordable and are greener even if that might not actually be the case.

The cleverest aspect of the SUV is that it appeals to the traditional urban 4x4 driver without being all-wheel drive, while ticking all the other 4x4 boxes.

Take up on two-wheel drive models is very strong and some leasing companies are saying that the 4x4 versions are being outsold by the two-wheel drive version.

This fundamental change to the profile of this sector will only help to maintain a strong residual value position in the market.

The list of 4x4 type vehicles with a two-wheel drive option is growing and includes BMW X1, Ford Kuga, Honda HR-V, Hyundai Tucson, Kia Sorento, Kia Sportage, Mercedes G Wagon, Nissan X-Trail, Renault Koleos, Toyota RAV4, Volkswagen Tiguan, Volvo XC60/90, Nissan Qashqai and Skoda Yeti.

With Land Rover even planning a two-wheel drive vehicle, my personal view is that the days of calling it the 4x4 sector are numbered and a switch to SUV is probably becoming inevitable.

Login to comment

Comments

No comments have been made yet.