Mercedes-Benz took the UK premium brand crown in 2017 due to gains over competitors in the fleet market.

AM has reviewed fleet and retail detail figures from last year to take a closer look at the UK’s premium market.

While BMW saw a 4.1% drop in registrations last year to 175,101 units and Audi had a flat year, down 1.31% to 174,982 units, Mercedes-Benz saw growth of 6.56% in total to 180,970 units, driven by 13.94% of growth with fleet customers.

Mercedes’ retail volumes actually declined in 2017 by 2.4%, but it was big gains with the A-Class in fleet specifically, up 20.32% to 29,114 units that pushed the brand forward.

It also helped to offset the drop in C-Class fleet sales which saw a 6.15% drop (but still represented the second biggest chunk of Mercedes’ fleet registrations at 25,563 units).

The biggest growth segment for Mercedes-Benz was its G/GLE/GLC Class products, up 45.3% in the fleet market to 10,136 units.

Its fleet performance also meant the brand made it into the top 10 volume sellers for 2017 in the UK with the C-Class and A-Class both on that list.

BMW’s fleet volumes dropped by 7.84% in 2017 and like Audi’s total registrations, its fleet performance was also flat (down 1.58%).

BMW’s biggest loss in fleet came from the 21.43% drop in X3, 15.36% drop in its 1 Series and 13.39% fall in 2 Series volumes with fleets.

![]() The biggest model in fleet for BMW is still the 3 Series at 26,445 units, but this also saw a 5.94% drop. The arrival of the new 2018 X3 should help BMW claw back business this year.

The biggest model in fleet for BMW is still the 3 Series at 26,445 units, but this also saw a 5.94% drop. The arrival of the new 2018 X3 should help BMW claw back business this year.

BMW did slightly better in the retail market, growing volumes by 2.47% to 67,845 units and this was delivered by gains with 1 Series up 30.1% to 16,673 units and 3 Series up 9.77% to 9,459 units.

Audi saw its biggest fleet loss from a fall in A6 registrations, down 26.68% to 8,204 units and the A1, down 12.3% to 8,492 units. The A1 is an important conquest vehicle for Audi and for many, their first way into the brand, so the new generation model due to arrive this year will be vital for fleet and retail volumes.

Audi’s biggest volume seller overall is the A3 and this saw a 5% fall in registrations in fleet to 21,822 units and a significant 22.68% drop in registrations in the retail market to 16,104 units.

The Q2 delivered big retail growth for Audi, with a full year of sales in 2017 propping up this side of the business with an additional 8,843 units.

A5/S5 registrations also increased with retail customers, up 48% to 5,980 units.

Jaguar Land Rover

While the big three German manufacturers are playing around the 180,000 unit volume mark, there is still a wide gulf between the rest of the premium players in the UK.

Land Rover is the closest competitor at 82,653 units in 2017. Combine its SUV line-up with Jaguar’s range of saloons and SUVs at 35,544 units, it takes JLR as a whole to a volume of 118,197 units.

Land Rover was second to Mercedes last year in terms of a volume growth spurt, growing the brand by almost 4% in total. Retail was the biggest growth area, up 5.21% to 48,329 units, but Land Rover also increased its fleet volumes by 2.16% to 34,324 units.

While AM does not have access to the model breakdown from Land Rover, it’s clear almost a full year of new Discovery sales would have been beneficial to the registrations success.

Volvo

Volvo really cemented its position in the premium market with its new XC90 back in 2014. While registrations were flat in 2017, down slightly by 1.19% to 46,139 units, Volvo has ambitions to increase sales to 60,000 units over the next two years.

The XC40 crossover is expected to help push Volvo towards its goal of a 2% market share by 2020, but last year it was big gains in the retail market that held up the brand from a negative performance.

Fleet registrations fell by 15.91% to 23,831 units, while in complete contrast retail was up 21.54% to 22,308 units.

Fleet registrations fell by 15.91% to 23,831 units, while in complete contrast retail was up 21.54% to 22,308 units.

S70/V70/XC70 fleet volumes fell off a cliff last year by 97.4% from 1,422 units to just 37 and there were also double digit losses from fleet from XC60 to 7,870 units (down 28.3%), V40 to 7,097 units (down 17.9%) and S60/V60 to 3,071 units (down 21.24%).

Volvo’s retail fortunes were boosted heavily by the new S90 saloon which saw registrations increase from 268 from the previous S80 model to 1,723 units to the new generation.

Retail demand for XC60 was also strong, up 67.53% to 8,432 units, making it Volvo’s most popular model by volume, followed by the V40.

Mixed fortunes for Audi

Audi lost share in almost every segment of the retail premium car market in 2017, as it failed to defend against a Mercedes-Benz onslaught and strong activity from BMW.

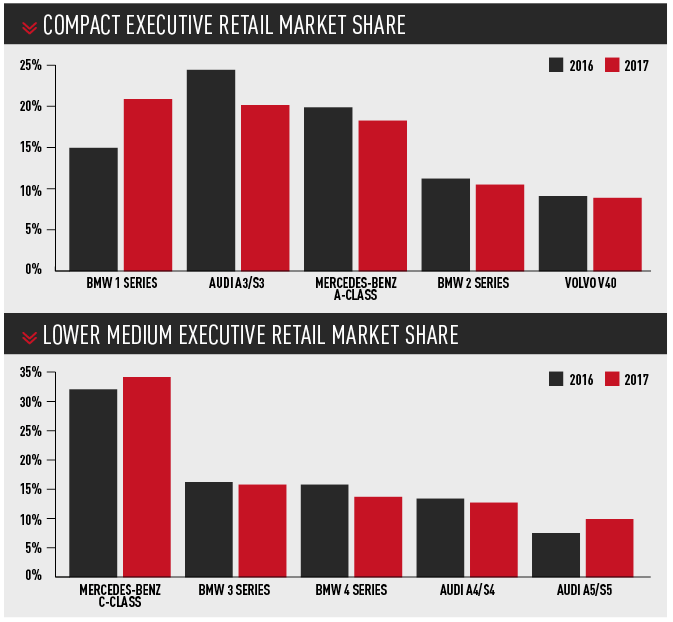

Audi’s A3/S3 range lost 4ppts share and lost the lead of the compact executive car segment, where it had accounted for one in four sales in 2016.

It was knocked into second place by the BMW 1 Series, whose segment share rose 5.9ppts to 20.9%. Mercedes-Benz A-Class dropped 1.5ppts in retail share, however grew significantly in fleet to more than compensate.

In the upper-medium executive car segment the Audi A6/S6 slumped 7.5ppts to record a 14.5% retail share and the A7/S7 lost 1.6ppts to settle at 3.25%. The Mercedes-Benz E-Class, already top of the class, stretched its lead by 0.7ppts to 33.2% share.

Mercedes’ flagship S-Class has led the large executive car market for many years, but in the retail market in 2017 the Porsche Panamera ate into its lead. S-Class share dropped 15ppts to 34.3%, while Panamera gained 21ppts to record a 26.5% share, overtaking BMW’s 7 Series (23.5%) in the process and leaving Audi’s A8/S8 far behind with 5.2%.

The SUV market was where Audi fought hardest. Its new Q2 took the lead of the small premium SUV retail market, rocketing to 18.9% share and leaving the Mini Countryman in second place with 13.1%. And in the compact premium SUV class, Audi’s Q3 gained 3.5ppts to secure a 26.5% retail share, narrowing the gap to the segment-leading Range Rover Evoque’s 39.5%.

Login to comment

Comments

No comments have been made yet.