The explosion of used car trade and retail activity witnessed in January was almost as remarkable as the market nosedive last April.

Every measure of market conditions saw a big positive swing as auction halls filled with buyers and forecourts buzzed with retail interest.

However, this cannot be interpreted as an end to the used car market downturn because most of the under-lying factors that drove it are still in place.

Rather, it seems that something of a waiting game for many retail buyers has now come to an end and that January’s positive conditions represent the release of some pent up demand that had accumulated during the uncertainty of the second half of 2008.

In other words, people who were seriously intent on changing their car waited until the economic outlook was clearer and Christmas was out of the way.

It also seems likely that the oft-repeated message ‘cars have never been such good value’ has hit home for many people. For example, CAP itself contributed to the message in last month’s Granada TV ‘Tonight’ programme in which viewers were strongly urged to take advantage of today’s deals.

Another factor working in the used car market’s favour is the weakness of the new car sector.

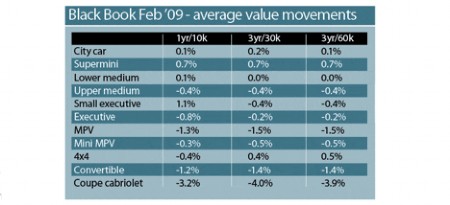

Analysis for the February edition of Black Book highlights the remarkable ‘bounce back’ of 4x4s, which outperformed most of the rest of the market in terms of trade values for the second month running. This is perhaps not surprising in view of the sheer value on offer now against a background of reduced fuel prices.

Also helping is the low level of trade car supply. Even cars requiring some refurbishment have been attracting solid trade attention.

However, even though some dealers have described the past few weeks as their best time for several years it would be unwise to call this a recovery.

The UK banking sector remains in crisis and it is not at all clear when it will be out of the woods or if there are further shocks to come. Rising unemployment is bound to further damage overall consumer confidence.

The bigger picture is now slightly better understood by the retail public but credit remains severely restricted and is likely to be so for some time even if government initiatives gain traction.

Looking at the sector performance analysis for Black Book, values were largely stable moving into February and it is notable that some of the vehicles that were under most pressure have enjoyed a resurgence.

Small rises were noted for average 4x4 values and for later plate compact executive cars an average rise of 1.1%. Convertibles are under the seasonal cosh and coupé cabriolets are severely underperforming, no doubt as discretionary ‘fun’ purchasing gives way to favouring more practical transport.

It remains to be seen where the market is heading but CAP’s view that conditions will generally continue to deteriorate until stabilising around the summer remains unchanged.

production line")

Login to comment

Comments

No comments have been made yet.