By Richard Yarrow

With a revised new car sales forecast from the Society of Motor Manufacturers and Traders (SMMT), the automotive retail landscape appears to be heading in the right direction. There’s also strong evidence that consumer confidence caused by the continuing low interest rate is translating to solid demand for used vehicles on the franchised forecourts. But what about in the wholesale market? What have the trends at the auction houses been in 2013 and will they continue over the next year? What vehicle types have been popular and will that change? Are there segments to be cautious of and what are the opportunities for growth? We’ve asked some of the industry’s leading lights for their opinions.

“The market has shown a great deal of resilience in 2013,” said Dr Andrew Jackson, head of analytics at Glass’s Information Services.

“While stock and prices have fluctuated, the underlying conversion rates and days on site, especially for those vehicles not being sold the first time through the auction house, have all registered strong performances.”

According to Glass’s figures, conversion during 2012 averaged 76%, but for the January-July period this year, it was up to 78%. The average first time sale price was £4,900, and second time was £4,700.

“These figures are averaged and ultimately only £200 apart,” said Jackson. “However, the gap has been remarkably close in recent months. Looking at 2012, the difference was a much more noticeable £500, which indicates demand for stock is such that vehicles which would not typically perform as well as the most desirable, are now being considered much more favourably by buyers.”

Glass’s also has good news on the age/price differences. In like-for-like YTD sales, every age segment is commanding a higher price than in 2012, with special mention going to 0 to 1.5-year-old vehicles, which on average are trading up £900 to £1,500. Between the ages of 1.5 and six years, the average increase in hammer price is £500, and even on older cars it’s still up by £100. Days on site figures have slightly improved throughout 2013 to about the 8.4-day mark. That’s down from 8.7 days in 2012. “The market is also moving close to 10,000 more cars per month than in 2012, which indicates that there is a clear demand for vehicles in the marketplace,” concluded Jackson.

Simon Henstock, UK operations director at auction firm BCA, said that at the start of 2013 the general view was that the huge year-on-year value increases experienced in 2012 were unlikely to be sustainable into 2013. “In fact we have seen similarly large value increases again this year,” he said.

There is also positive news from independent company SMA Vehicle Remarketing. National operations director Eddie Thomson said the business had seen a steady increase in volumes, but of slightly more mature vehicles. “This is the case for both fleet and retail sources, and there remains a ready market for this stock, as evidenced by our record sales activity achieved in August,” he said.

When will pick-up in new car sales feed through?

CAP’s analysis of the year to date is broken up by the spring plate change. Lack of stock and good demand drove the market until Easter, at which point new car sales were driven by March registrations and campaigns, increasing part exchanges.

“After that, the market returned to a more normal pattern with gentle erosion of used car values each month,” said Derren Martin, senior editor of Black Book Live, adding that strong new car offers are currently the major factor affecting the used car market.

However, for many in the industry, one familiar issue remains a sticking point. The pick-up in new car sales that started last year has yet to feed through to the wholesale used market, and that means a lack of what everyone is looking for.

“The main trend this year has been the continued shortage of prime, good quality, retail-ready stock and the positive impact this has had on values year-to-date,” explained Daren Wiseman, valuation services manager at Manheim Auctions.

“Any peaks in volume have tended to be short-lived and pricing pressures, as and when they have materialised, have lasted weeks rather than months.”

One result has been dealers adopting a more targeted approach to their vehicle sourcing activities. For example, Autotrade-mail, the online vehicle supply network, has reported an increase in the number placing ‘wanted’ adverts on the system.

“These are not generic ads but specific ones to meet consumer requirements,” said Kevin Watson, Autotrade-mail’s operations director. “It’s a clear sign that the used car market is picking up, leading to concern that the shortage of good, clean, quality used cars will only get worse.”

So what stock has been popular in the auctions this year? As always, three and four-year-old vehicles with less than 60,000 miles on the clock tend to be top of dealers’ wish lists.

However, with those in short supply, some retailers are relaxing their stock profiling policies and bidding on five and six-year-old models to try to retain showroom footfall. Anything with a Ford, Vauxhall or VW badge remains popular because it will tick plenty of boxes for the end user. Finally, compact SUVs continue to hold their value well as their popularity continues to rise with motorists. Glass’s figures reveal the current top five vehicles with a retail time of less than 35 days are the Land Rover Discovery, Audi S4 Avant, Citroën Nemo Multispace, Audi S3 and Lexus RX400h.

Autotrade-Mail’s stats show the top five cars currently in demand from dealers are the Range Rover, Porsche 911, VW Golf, Ford Focus and BMW 3-Series, with the Discovery a couple of places lower in seventh spot.

Convertibles still selling well in UK

“The Range Rover moves up from its customary fourth place in each of the last four years, while the Porsche 911 has jumped up from 10th place last year,” said Kevin Watson.

John Davies, chairman of the Vehicle Remarketing Association (VRA), said the British love affair with convertibles was still in evidence, with demand and prices both remaining strong. However, he said smaller cars were making the best money.

“Petrol models in particular are popular, because at Fiesta/Corsa level, drivers don’t cover enough miles to warrant a diesel engine. Any smaller car that is fuel efficient and has a low CO2 rating and therefore low VED is in high demand.”

Eddie Thomson at SMA agrees, but warned: “Supply is tight and as such prices are at a premium, and it’s a premium that may well have been pushed as far as it’s feasible to go in light of some of the offers on new cars that we are currently seeing.”

Anything crossover or MPV with a high degree of practicality for the owner is also proving popular in the auction halls, almost irrespective of brand.

“Cars like the X1, B-Class, Note, Alhambra, Yeti and Forester are all in the top three for their respective manufacturers,” said Glass’s Jackson.

BCA said the budget end of the market has remained strong, particularly in the £2,000-£3,000 bracket. “Older, well-presented cars at sensible mileages will regularly outperform guide values. This sector is typified by cars entered from dealer part-exchange sources,” said Simon Henstock.

The obvious next question is what should dealers avoid when stocking their forecourt. Glass’s states the least popular vehicles on the top 100 of retail cars include the Chrysler Ypsilon and Delta, the Hyundai Veloster and Citroën C-Crosser, so they’re clearly not going to make top dollar in the wholesale arena.

Cars with a gas-guzzling petrol engine can also be slow to sell unless it’s the right car with a high spec and sitting on a London forecourt.

“Anything with more than 100,000 miles on the clock is viewed with suspicion, and so prices have been a little depressed,” said John Davies of the VRA. The only exception is ex-fleet vehicles.

Used car dealers ‘wary of cars under two years old’

CAP said dealers were also wary of cheaper cars with costly road tax, and also anything which is under two years old. Large cars lacking a prestige badge are also less likely to appeal to dealers.

|

Inevitably it’s the older vehicles in poor condition and with high mileages which don’t catch the eye. But that’s not always the case.

“Despite the challenge of retailing such models, the general shortage of premium quality stock has ensured that even the less attractive vehicles have kept attracting bids,” said Manheim’s Daren Wiseman.

Beyond that, it’s the usual suspects – cars considered to be too niche, anything missing the more desirable optional extras and unusual colours inside or out. Poorly prepared vehicles are also sticking out, said Eddie Thomson from SMA. “Buyers are increasingly looking for showroom-ready stock. The benefits in terms of just-in-time stocking and known preparation costs mean anything that requires significant remedial work will see a lower price.”

Kevin Watson at Autotrade-mail said few dealers were prepared to take a risk on something they were not confident about.

“A few years ago, as long as the vehicle had a sensible margin, there were quite a few dealers that would. Today, in a challenging market, they can no longer afford to stock something that they can’t be sure will sell within a reasonable timeframe.”

There’s also a word of warning about city cars from CAP, with advice to dealers to exercise caution when considering what to pay for them.

“Due to the relatively low depreciation the values are quite compacted, so the prospect of retaining a decent margin while offering a saving against a new car becomes very difficult with the later plate used examples,” said Derren Martin at CAP. He said there was evidence some car supermarkets were stocking them because they felt they should, to give customers the choice, rather than from any desire to sell them in decent volumes or to generate a profit.

Opportunities in more unusual used car stock

What are the opportunities for dealers specialising in the more unusual stock? They tend to do solid retail business if they have a loyal local client base – e.g. affluent buyers in and around major cities – but the issue can be sourcing replacement product. However, the growth in digital auctions means retailers seeking niche products can locate them easily online and buy as required.

For those specialising in performance models, the S-badged cars from Audi, particularly the S5, S4 and S3, attract solid interest and high prices.

“Porsche’s Cayman is an outstanding performer for the marque in used car terms, with an average retail time of 41 days, versus the next-best performing model, the Cayman S, at 51 days,” said Andrew Jackson at Glass’s.

Those focusing on 4x4s will continue to do repeat business with loyal, often rural-based customers, though Manheim said it’s anticipating earlier demand this year as retailers stock up before the traditional market peaks of November and December.

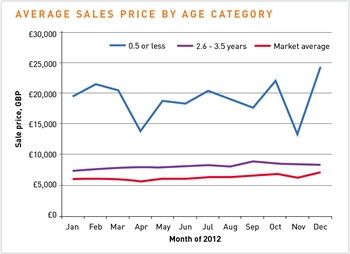

Is a wind of change going to blow through the wholesale market later this year and into 2014? At Glass’s, Andrew Jackson said the signs were that nothing would alter dramatically.

“The 0.5 or less age segment was relatively volatile in 2012, and 2.5 to 3.6-year-old cars struggled relative to the rest of the market over the back half of 2012,” he added. “It will be interesting to see how these pan out, but it’s a safe assumption these sectors should perform better than last year.”

Jackson said there was little chance of the wholesale market becoming flooded with fleet vehicles, because growth in the corporate sales sector has been relatively stable.

CAP believes there will be some pressure on values from the end of September and into October due to part-exchanges generated by new plate registrations. “There is still a lack of stock from fleet companies due to low registrations three years ago, so values should only decline due to seasonality. Values tend to drop in Q4 due to lower demand and more supply than in other quarters,” said Martin.

Stability is also the watchword at the VRA. It believes demand may continue to exceed supply in some areas – such as the B and C segments – which will help wholesale prices to remain strong.

“If the general economy continues to show signs of recovery and unemployment figures continue to fall, consumer confidence is likely to continue to build and more drivers may decide to buy a new used car. This extra demand may then ensure price stability well into 2014,” said John Davies.

Fleet sector confidence can obviously have a significant impact on the quantity of vehicles entering the wholesale market.

Manheim’s Wiseman said with stock levels remaining fairly stable over the past couple of years – and no huge increase in fleet volumes anticipated – the result was predictable: “Values should remain stable and pricing fluctuations are likely to follow the seasonal patterns we have seen over the past couple of years.”

Manufacturers’ new car deals will have an impact on the used car market

With new car data clearly showing manufacturers focused on retail registrations during 2013, there are less returns being generated from the corporate sector. They’re also reducing short-cycle business and what they do have for the wholesale market is mainly returning to the manufacturer, rather than being offered on the open market.

The VRA’s Davies said fleet operators and asset owners had been confident about the used market for the past 12-18 months. That’s because prices and conversion ratios at auctions have been stable. “Generally fleet cars have been coming back older and with slightly more mileage as companies extended replacement cycles on the back of the recession. However, they are still being serviced on time, so the used market is still happy to buy them.”

With restricted supply applying upward pressure on auction prices, it’s clear the current state of the market is going to affect dealers’ bottom lines. The trap to avoid is paying more for a car wholesale then being unable to pass that extra on to the customer, particularly as they are ever more savvy, armed with a wealth of online information and with details of comparable vehicles from other retailers, local or otherwise. Again, OEMs’ attractive new car deals will have an impact.

One final fillip. Many industry insiders say there’s strong anecdotal evidence that the compensation payouts that followed the mis-selling of payment protection insurance (PPI) have encouraged people to change their cars. With a similar story likely to unfold over card protection products (CPP), enhanced retail demand during 2014 could yet have an impact on wholesale used car market values.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

Login to comment

Comments

No comments have been made yet.