By Dr Richard Parkin

The UK new car market has been somewhat of an enigma in recent times, given its relative buoyancy versus the Eurozone countries. A combination of better economic growth, lower unemployment and PPI pay-outs have provided the consumer confidence and means for many to acquire a new car, which for some is a new experience.

|

||

|

Dr Richard Parkin is director of valuations & analysis at Glass’s, where he coordinates the editorial and analysis team. Prior to joining Glass’s in 2012, he spent six years as a strategy consultant at Ernst & Young, with a focus on the automotive industry. |

||

Seeing the obvious opportunity, UK national sales companies (NSCs) have aggressively pursued a strategy of affordable new cars for all, chiefly through various forms of cash discounts sewn into Personal Contract Purchase plans (PCPs). The attractiveness to dealers is that such sales can engender customer loyalty as it becomes much harder to walk away from the brand: existing customers can always be enticed to extend their contract with a new car for similar money before the end of the original term, although such tactics only apply to the original owners. However, the downside of such a strategy is that the residual value (RV) can be damaged, especially for a nearly-new example.

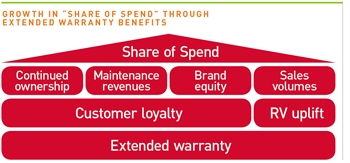

But market share can be maintained or even increased by using other forms of discounting that don’t involve reducing the price paid per se, but provide additional benefits instead. More optional equipment as standard is one way of achieving this; another is to provide reassurance to the buyer in the form of an extended warranty, as illustrated below.

Unlike “cash-like” forms of discount, provision of extended warranties not only supports customer loyalty through good customer experience, but it can provide a demonstrable uplift in RVs. Indeed, EurotaxGlass’s has previously shown in Germany that RVs for otherwise identical 36-month-old models improved by 1-3% with an extended warranty bundle, provided the benefit is transferable to a subsequent owner when the vehicle enters the used marketplace.

Another challenge for OEMs and franchised dealers alike is to keep the servicing and repair revenues in the network for as long as possible, as this is where the margins are often being made. The problem is that peak maintenance spend on a car typically lies inside a vehicle’s second or third ownership cycle, where owners are more likely to use independent garages – and non-OE spares – for repair and servicing work. However, extended warranties can help retain a link between the dealer and subsequent owners, thereby keeping more of the aftermarket spend in the network and ensuring that OE parts are used.

Another challenge for OEMs and franchised dealers alike is to keep the servicing and repair revenues in the network for as long as possible, as this is where the margins are often being made. The problem is that peak maintenance spend on a car typically lies inside a vehicle’s second or third ownership cycle, where owners are more likely to use independent garages – and non-OE spares – for repair and servicing work. However, extended warranties can help retain a link between the dealer and subsequent owners, thereby keeping more of the aftermarket spend in the network and ensuring that OE parts are used.

In the future then, expect to see more PCP deals offering extended warranties and/or free servicing rather than deposit contributions, as the desired new sales volumes and market share can be achieved without the risk to RVs.

christopher.smith - 03/10/2014 12:42

What's the point of an extended warranty when the majority of PCP terms fit within the 3yr/60k offered by most mfrs?