Car dealer networks are likely to be cut by more than a quarter by the end of this decade.

This will be driven by the need to restore dealer profitability in the face of changing customer buying behaviour, and to finance innovations in sales channels such as online and smaller satellite outlets in prime shopping areas, according to the International Car Distribution Programme (ICDP) in the new edition of its 'European Car Distribution Handbook' (ECDH).

The axe will fall most heavily on the networks of the traditional European volume brands that have the densest dealer networks and have come under pressure from growth brands such as Hyundai and Kia, and premium brands such as Audi, BMW and Mercedes moving into lower price points.

Mainland European markets will see more consolidation than UK or Nordic, as markets have been more depressed, dealers have suffered heavier losses, and many dealers are below the minimum viable scale to be profitable. The restructuring process will be progressive, and include a consolidation of investors to create regional and local networks of outlets under centralised management control.

Some key findings from the 'European Car Distribution Handbook 2014', include:

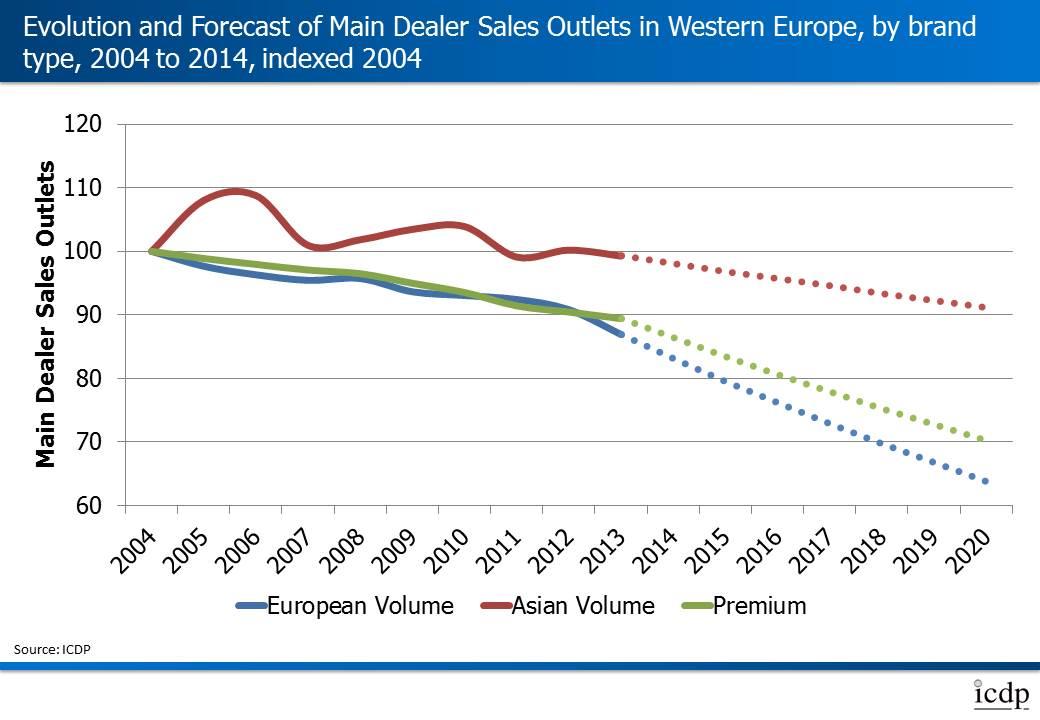

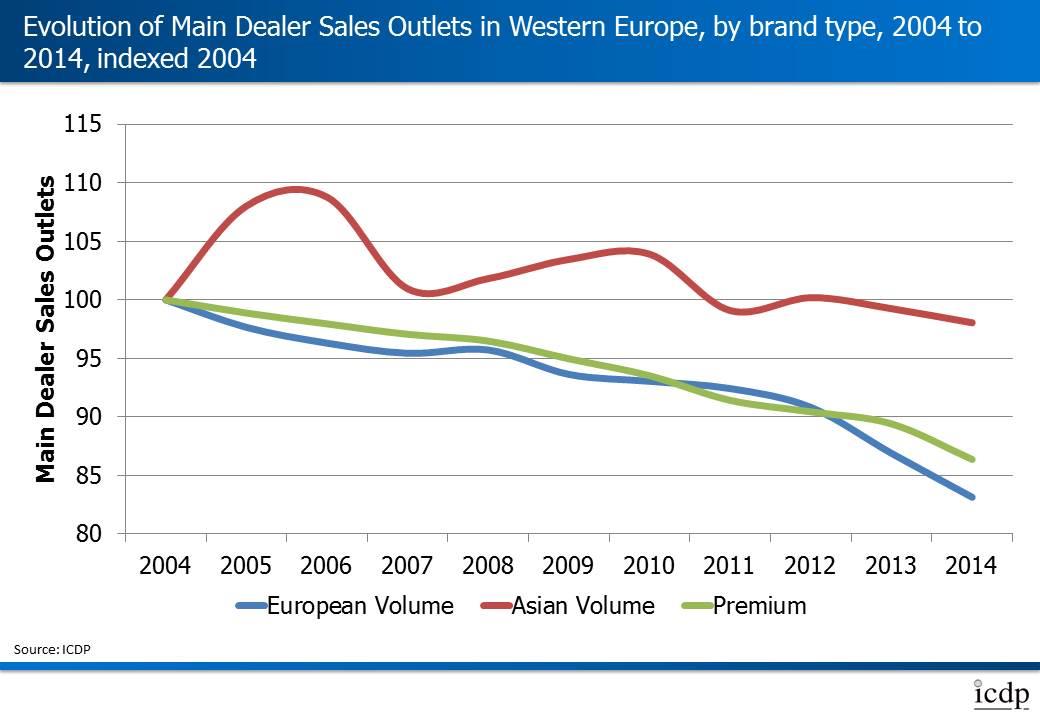

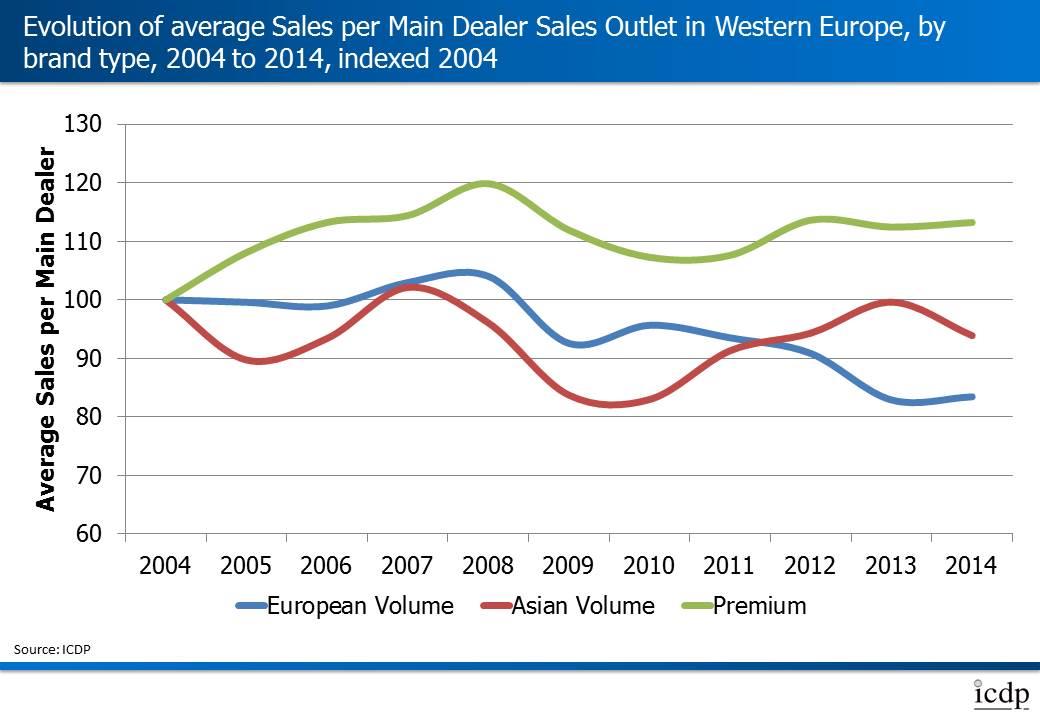

> In Western Europe, between 2004 and 2014, there was a net decrease in main dealer sales outlets, for 30 continuing brands, of 14%; a decrease that has been accelerating in recent years as a result of the financial crisis. Despite this, average new car sales per main dealer have also fallen 10% from 288 to 257 over the same period

> If the recent rate of decline continued, this will result in a further reduction of 23% for European volume brands by 2020, and of 19% for premium brands – equivalent to a reduction of 8,499 dealers from 42,408 in 2014 to 33,909 in 2020

> For the two leading Korean brands – Hyundai and Kia – their networks have grown by 13% over the last decade, and if they maintain that trend, they will add 236 main dealers to their Western European networks by 2020

> ICDP consumer research this year has shown that as customers continue to do more of their car buying research online, the number of dealer visits has fallen to only 3.2 visits to 2.4 showrooms with 45% only visiting dealers of the same brand

> This changing behaviour and the need to reprofile sales networks to match, mean that the actual reduction in traditional dealer networks is likely to exceed the trend numbers, creating a “property timebomb” as surplus dealer properties come to market, depressing values and hitting dealer balance sheets and bank loan books

> Elsewhere in Europe, there are mixed fortunes, as short term economic problems in for example Hungary or Russia are balanced against a positive outlook for long term growth in the car market. For Central and Eastern Europe, Russia and Turkey, main dealer numbers grew by 50% over the last 10 years, and will continue to grow to 2020.

By rationalising networks by the forecast figures, many brands can expect an increase in the average sales per main dealer if sales volumes remain at 2013 levels, and therefore an improvement in dealer viability and their ability to invest in and support new channels and capabilities.

European volume brands would be expected to increase the average sales per main dealer by 30% from 339 in 2014 to 441 in 2020 if the predicted 23% network decline occurs, whilst premium brands could experience a 23% increase from 250 to 307.

Steve Young, managing director of ICDP, said: “The car industry is not immune from the general trends in retailing, and the current dealer network model has passed its 'use by' date.

"Pressures that have built up during the crisis years must now be released, and we anticipate that the next five years will see the biggest shake-up in the traditional dealer model in Europe that there has ever been.

"This will bring welcome changes for new car buyers, and opportunities for new and existing investors to build scale businesses. However, there will also be losers, and manufacturers will need to manage the transition with care to strengthen their position, as opposed to losing share and damaging their brand.”

About the European Car Distribution Handbook:

Updated annually since 1996, ECDH is a guide to the franchised sales and service networks of all significant car brands in Europe, covering 36 markets in the European Union, European economic area, Russia and Turkey. It is available as a single copy in PDF format for €2,700 or through a data portal which allows queries to the database over multiple years. For more information email janetrace@icdp.net.

Jeremy has been a journalist for 30 years, 20 of which have been in business-to-business automotive.

He was a writer and news editor on AM-sister brand Fleet News for three years before setting up the AM website.

For the last seven years he has been Bauer B2B’s head of digital helping to manage the digital assets of Fleet News, together with AM and RAIL.

In 2025 he was an Association of Online Publishers awards judge.

David - 24/01/2015 22:42

You can also be sure that the Chinese will also start to make their presence felt in the UK car manufacturing scene! Their cars may be cheap as Chios at the moment with poor quality, but they are learning quickly, they have the capital to invest and are keen to enter the Western marketplaces. Watch this space!