The automotive retail sector is sufficiently dynamic and innovative to adapt to a predicted weakening in the market conditions that have led to a perfect scenario for PCP growth in the market.

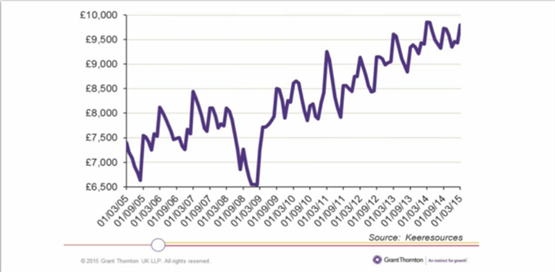

Low interest rates and inflation, a strong pound to the Euro, gradual increases in new car prices, high consumer confidence and strong residuals (see graph below) have combined to create a positive market for new car retailing, allied to an emerging trend of vehicle use rather than ownership amongst the newest generation of buyers.

But, while there are fault lines occurring in the bonded positivity, the industry will adapt.

This was the key message in a webinar hosted by Grant Thornton on the topic of PCPs today.

It was hosted by Paul Burrows, Grant Thornton’s automotive director responsible for M&A, with Richard Parkin, associate director of its strategy group, Bill Parfitt, former managing director and chairman of General Motors UK and now automotive advisory consultant for Grant Thornton, and Colin Tourick, its professor of automotive management at Buckingham University.

The weak point that could be predicted, particularly by industry watchers, was a ‘softening’ of residual values and with the reduction in the equity value of car for a consumer on a PCP, who was more than likely expecting this to be a deposit at the end of the contract term – particularly when the dealer called part-way through this with an enticing offer to renew for a new car, while paying no more each month.

Parkin said that not until the end of this year and into 2016 will there be a “normalisation” of vehicle supply.

“What we’ll end up with around the end of this year and into next will be supply growing at a faster rate than demand. At auction we’re still seeing trading on three year values at slightly higher values than they were a year ago. But they may well have peaked.

“Additionally, forecast values being used for PCP products, are changing. CAP has forecast values recently (in Gold Book) much higher than it had historically. It looks like it’s becoming increasingly unlikely that the level of equity people have so far enjoyed will be available in a vehicle.”

However, Parkin cited Manheim research that suggested 80% of customers expect there to be equity in the PCP when it reaches full term.

“The residuals on PCP deals will mean early redemption will not be possible.”

He said there wouldn’t be a massive, overnight increase in supply, but a slow trickle from the September plate change. “Most people expect the current levels of RVs are not sustainable, and I expect a correction of around 10-15% over about a year to 18 months.”

Increased manufacturer support

But the continuing strength of the pound in the climate of a weak European economy would mean manufacturers were willing to increase the level of their support in finance products, helping to mitigate the impact of softening residuals.

It was said in the webinar that more than 80% of Ford’s private sales were on PCP, 70% of Hyundai’s and about 40% of Vauxhall’s.

Parfitt said: “Customers have got used to low deposit and monthly payments and if they have sufficient equity they will renew the PCP agreement, locked into finance packages for some time. Individual contracts will get longer as residuals weaken - we’re already seeing five year terms,” he said, based on research he had done of around 30 dealer groups.

And Tourick said: “If we get to a situation in a year or 18 months when customers don’t have a lot of equity, something has to give and its normally accepting that the agreement will have to be longer.

“If a consumers gets to a point at three years where there is no or negative equity it makes sense to extend a contract term because the monthly payment is the same, but the level of depreciation in absolute terms is diminishing – you’re playing catch up.”

New vehicle registrations and the alternative to PCP

If the early churn of current PCP deals reduces , it follows that new car registration totals would reduce the panel agreed. “But it depends on reliance on the PCP product and reliance on it based on a manufacturer’s residuals,” Parkin said.

Tourick said manufacturers will then behave “rationally”.

“If customers are aware of not having any equity in their vehicle, the manufacturer will still want to hold onto them,” he said. Tourick suggested personal contract hire (PCH) deals could provide an alternative: “PCH gives the manufacturer’s captive finance company an advantage: on a shorter term deal, it gets the profit at the end of it; with PCP the profit is given away to the customer. So, you can retain the customer, potentially keep the profit and churn vehicles with PCH.”

So, if PCPs get tough, manufacturers will start pushing this alternative product, Tourick predicted.

The average disposal values of the top 100 fleet cars

Rising residuals have created sufficient equity for customers, that captive finance houses have been encouraging dealers to bring customers back into dealerships after around 25 - 28 months, offering them the chance to have a new car, for the same monthly payment for another three or four years.

Jeremy has been a journalist for 30 years, 20 of which have been in business-to-business automotive.

He was a writer and news editor on AM-sister brand Fleet News for three years before setting up the AM website.

For the last seven years he has been Bauer B2B’s head of digital helping to manage the digital assets of Fleet News, together with AM and RAIL.

In 2025 he was an Association of Online Publishers awards judge.

Bob Sherman - 24/04/2015 14:58

Nonsense. Why would PCH make sense if PCP doesn't? Why would PCP not make sense if rates and inflation are continuing to be low? Why show RVs as pound-note values not % of OTR? This is a very strange and poorly judged piece.