William Blake once said “The road of excess leads to the palace of wisdom.” And it seems the industry is learning lessons as it manages records volumes of new registrations and used car volumes.

The first quarter of 2016 has seen registrations beating an already record year in 2015, which in turn followed four years of strong growth.

New car registrations in February posted an 8.4% increase over the same month last year, with 83,395 cars registered, the largest February since 2004. Year-to-date registrations were up 4.7% compared to the first two months of 2015.

Private registrations continued to drive the increases, with an increase of 22.6%. For consumers taking a car on a PCP, maybe the appeal of a new plate is diminishing.

March is likely to be another record month with pre-registration, or tactical, activity accounting for a significant proportion of new registrations. In a survey conducted by cap hpi, pre-registered cars could account for up to 20% of Q1 registrations, a figure that could rise in Q2.

Nearly half (46%) of the respondents said they expected between 11-20% of cars to be pre-registered in Q1, and 17% expect the volume of pre-registrations to be over 21%.

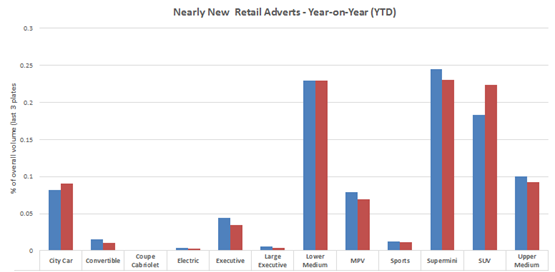

While strong demand is driving up used values across the industry, it is important to keep an eye on late-plate volumes, particularly those generated by pre-registrations. There are some signs of weakness in the nearly new sector, which is not showing the gains of other sectors.

There are some big manufacturer discounts to be had on new vehicles that may further impact values. Within the overall figures, there were vehicle ranges that performed strongly and moved up in value, whilst for others, supply outstripped demand and values did drop. It was not a wholly consistent picture.

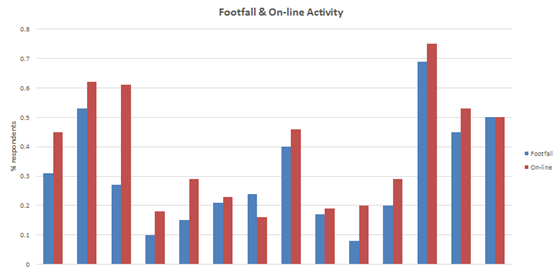

While dealers reported strong demand on the forecourt and online, as the chancellor outlined in his budget, a number of known unknowns exist for the rest of 2016 that could provide a challenge to the economy.

Storm clouds may be gathering but all the indicators are pointing to strong consumer demand continuing to drive the industry forward. The Cap HPI dealer survey reports positive outlooks on retained margins.

With demand is rising some dealers have voiced concerns about stock availability. Data from Cap HPI has shown a 14% increase in cars sold through auction during March, compared to the previous year. And the used vehicles are finding retail buyers with a 7.7% increase in the number of used cars sold so far this year against the same period in 2015.

Reflecting the supply and demand sentiment, 83% of dealers in the cap hpi survey are anticipating an increase in used car volumes/supply in March, although market feedback raises the question of will it be the right stock and when in March will it arrive.

Dealers are bullish about achieving their March targets, with 71% reporting they will. 72% of both the franchise and used dealers believe the March registration will see growth in 2016 compared to 2015.

Whatever the rest of 2016 holds, it is sure to be a year like no other.

production line")

Login to comment

Comments

No comments have been made yet.