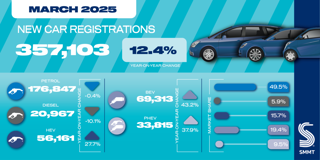

What is your view on how the PCP market has developed and can its growth continue indefinitely?

What is your view on how the PCP market has developed and can its growth continue indefinitely?

It has grown hugely over the past few years and it has pushed the new car market forward. PCPs help keep those customers with the dealership and provides a used car stock for the dealer too. I think specific factors like the VED changes in March gave registrations a boost, but I see no indications that PCP growth won’t continue.

There may be some softening of demand over the year, but PCPs make getting a new car very affordable in comparison to HP or outright purchase. That way of funding their vehicle is very much part of the consumer psyche now.

With the majority of new car purchases funded through PCP, are franchised dealers overly exposed to the product and what happens if the bubble bursts?

I think in terms of how the dealer views PCP volatility, a lot of that risk is taken on by the finance houses.

It does get raised as a topic for discussion, but we don’t see any massive changes to interest rates on the horizon or manufacturers withdrawing support on retail offers. That support from manufacturers has been strong and they still very much want to sell cars in the UK, so my view is that those deals consumers are getting will continue. I would say that if dealers are worried about PCP volatility, they should talk with their finance partners.

Will used car PCPs continue to take off as a product and are there any risks there?

Used car PCPs have a lot of potential.

Historically, it hasn’t been available through the finance houses, but many are starting to offer it. It’s another way to make those younger used cars more affordable than they would be through HP or outright purchase. I don’t think there’s a risk on that market with the replacement cycle as customers can still replace with a younger used car when they are into year two. If you add a service plan to that used car PCP package you are fixing your motoring costs and I think that’s something customers want.

Is the way PCPs are sold on the Financial Conduct Authority’s (FCA) radar? Should dealers be concerned?

There are some concerns the FCA will look at PCPs in the same way they have looked at GAP insurance sales in the market. However, we have seen no indication the FCA views PCPs as a problem area, but it’s something that could happen.

How widespread is the problem of customers clocking PCP cars to avoid excess mileage charges?

It’s an issue we have raised with Government when asking for odometer fraud to be outlawed. However, it is difficult to get an idea of the scale of the problem, although we do know it is happening. We will continue to campaign to outlaw clocking, but dealers can also help by identifying how many miles a buyer generally drives each year and ensuring customers set realistic miles on their contracts. We are currently waiting for the Government to respond to a recent consultation on motoring services which should be imminent.

Have GAP sales been negatively impacted by the FCA’s new regulations? Should dealers be worried about commission disclosure?

We haven’t seen a negative impact. It’s quite interesting as we have seen from members that their GAP sales have actually increased on average. Putting a structured and FCA-compliant process in place around GAP brings it to the front of the sales process and customers walk away feeling very informed. Adhering to that process has gone pretty smoothly. The latest guidance we have seen around commission disclosure also looks as though that’s not going to go ahead. It’s something we will continue to watch, but at the moment it doesn’t look imminent.

How good is the FCA’s communication and understanding of the industry?

Communication has improved, but there’s always room to go further. The huge struggle is the administrative burden for record-keeping in the wake of the FCA regulations. Dealers need to be on top of that and while the larger groups can cope, it’s difficult for smaller and medium-sized businesses. Keeping up with the compliance is a tricky area and the majority of dealers are having to employ or outsource for compliance specialists and that’s a direct result of the FCA regulations. A reduction in red tape in this area would be welcome.

How is the NFDA working with dealers to improve relations with the FCA?

We have an ongoing relationship with the FCA, but we tend to meet on specific issues. We did a lot of work with them around the changes to GAP.

I think the FCA still has a problem understanding what franchised dealers do and how that differs to brokers, finance houses and manufacturers. At the moment they see the industry and everyone the same way, with everyone facing the same issues and problems. We need to keep working with them and we’re spending as much time as possible to educate them about how the industry works.

")

Login to comment

Comments

No comments have been made yet.