What are the factors affecting dealers' used car margins over recent months?

To help identify these, where better to start than with the dealer networks who are working hard to retain every profit opportunity available?

We asked whether used vehicle profit margins were dir-ectly relative to either the type of vehicle or its benchmark value. The answer may surprise some. Only 20% of dealers we questioned agreed that retained vehicle profit margins are linked to the actual vehicle itself or the cost of it.

A much more significant 55% attributed the level of profit primarily to the actual ‘sales process’ and how that is managed within the business. The remaining 25% put shrinking profits down to either preparation costs increasing or changed customer profile.

The economic circumstances of many consumers will have an impact and one dealer reported that customers were ’skimping’ on servicing costs and routine maintenance to save money. This means an increasing number of part-exchange cars coming through the doors have missed routine services. In some cases, two or three-year-old cars have not had any servicing since the initial PDI.

This view is supported by many dealers, who complain that the problem is not confined to private cars and that a significant minority of cars from other remarketing sources and suppliers are also missing important service history.

All of this impacts on dealers in a number of ways. One of them was very noticeable near the beginning of this

year, when there was very strong competition for those few cars that could really be described as ‘clean’, forcing dealers to pay what many saw as over the odds for reasonable stock. Not only is a more expensive trade price likely to put pressure on a final margin, so too will the increased preparation costs.

Improving the offer

There may be some good news for dealers in these statistics, though. Trade values and preparation costs are out of their hands, but 55% believe the most critical factor is the sales process and that is something over which they do have influence.

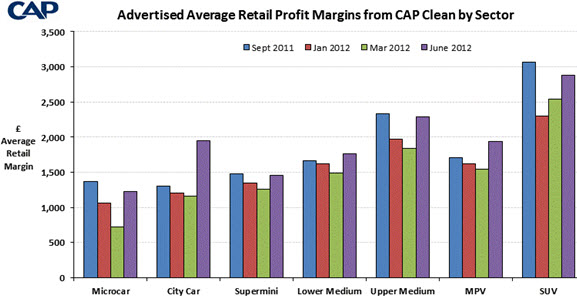

Our graph below demonstrates that during the previous 12 months, the margins between average selling price and the CAP Clean values have been relatively level, with some increases and decreases from certain sectors such as the city car where we have previously written about the increased penetration from more prestige manufacturers.

We are all familiar with statements from inside and outside the dealership, such as “poor quality sales advisers and weak management”, plus observations like “when demand is greater than supply, retailers still discount the first offer to the customer”. But it is a frightening fact that only 5% of customers buy at the first offer from the retailer.

Regardless of whether you are a dealer selling just 20 cars or more than 100 per month, every £100 per unit can make a huge difference to the business. There are always improvements that can be made, support that can be requested and systems that will help, but overall, since the 1980s, not much has changed in the motor trade. In the end, the fact remains that it is people, price, process, promotion and product that drives profit.

Compete on more than price alone

Competition to appear in the search engines as the cheapest is here to stay for many and this has doubtless taken a massive toll on profit per unit. Nor can dealers do anything to avoid the consumer continuing to be better informed – in some cases more so than the professional.

But there are businesses that manage better than others in this area so it is clearly possible to compete on more than just price. It may require harder work, but it is also possible to manage the problem of sourcing cars more smartly and paying the right price, rather than just jumping into a bidding war for stock.

These are some of the things the 55% who rightly recognise process as key are already tackling.

by Philip Nothard, CAP retail and consumer valuation editor

LINGsCARS.com - 12/09/2012 09:03

Price is important to the consumer, but rationalising and adding emotion to the buying decision is far more important. Or else, we would all use the cheapest phone, the cheapest TV and the cheapest sofa. And all drive Kia Picantos. Dealers selling largely identical cars by largely identical methods and identicit company images and "values" in a race for the cheapest price are making a mistake. Far more important is to add emotional value to the sale (either tangible or intangible). If a customer is extremely happy with the car transaction and feels warm inside, price becomes far less important. There are so many aspects to a sale apart from the price and a lot of the time - by poor process, communication, management and experience, the customer will revert to the price as the only justification for buying the car. At that stage, it has gone badly wrong. So many sales methods irritate customers. These methods need surgery. Just get rid of them. Everyone has roughly the same cars at the same prices, so you need to differentiate. Getting to the top of search engines is an example of where dealers lack creativity and intelligence. Throwing money at it, and discounting prices is a recipe for disaster. So is subjugating control to a 3rd party like AutoTrader. That's long term disaster. For instance, my advertising spend and Google spend is £NIL. Customers need to be encouraged by far more than price and the usual asinine claptrap about the cars and the most blatant "CHEAP CAR" Google listing. Dealers should use far more intelligence to make people WANT to click, WANT to talk and WANT to transact. Give customers the control they want and they become happy chappies. Cutting overheads and increasing efficiency and avoiding mistakes is another way of building in profit. Yet few dealers take the Ryanair/LINGsCARS approach to costs. Dealers spend like it is Christmas. Using the web efficiently means an awful lot of overhead can be slashed, while adding emotional value and happiness. But dealers still insist on traditional face-to-face and phone contact with traditional salesmen, and go no further than using email as a 21st century option. This is very poor. Yet dealer spend is big (mainly on sh1te) and many dealer group resources are massive. In my case just two people can manage 300 concurrent customers and with use of technology, an intelligent adult communication sausage machine, good systems backed by multimedia (eg video communication), entertainment (while waiting for new cars for weeks/months), lightning fast responses (current time 2 mins 46 seconds), full written transcripts of conversations, easy methods of document upload and completion, etc etc, (which delight customers) still provide a service the customers regard as the best sales experience they have ever had (never mind best CAR sales experience). When I have the head of retail at Matalan telling me it is "transformational, best sales experience ever", something is right. There is so much more that can be done, but so few dealers do it. Car buying is an emotional experience, so why not deploy emotion? It is free. It's no good just moaning about margins. Ling LINGsCARS