By Rupert Pontin

Much has been said of the dramatic increase in new car registrations over the past few years. As an industry, we are in an enviable position – few market sectors have the traction and momentum that the UK motor trade looks like it will benefit from over the coming 12 months. The new and used car trade is vibrant and although used car sales have slowed a little, retail activity will generally remain consistent.

However, it is important that we review key areas of our market from time to time. We can all learn from highs and lows and use trends to improve what we do. Therefore, it is prudent to take a clear view on what has happened with new car sales and the impact on the ‘late-plate, low-mileage’ market that is so closely linked.

The UK’s continued increase in new car sales has been driven by product availability. Manufacturers look at volume planning and factory growth seven to 10 years in advance. Factories are currently producing cars based on forecasts approved by management before the 2008 economic meltdown. Such was the investment deemed necessary seven to 10 years ago, it has been reported recently that European vehicle production capacity will increase by a further 17% in the coming five years.

With European and world markets performing poorly and manufacturers struggling for sales, the UK has been almost the only light at the end of the tunnel, as it provides a vent for European overproduction.

UK manufacturers have been tasked with finding buyers for products originally intended for many other marketplaces. This has been achieved via creative pricing and a focus on PCP deals attractively designed to meet the UK consumers’ fascination with monthly figures rather than overall cost. Buyers have been effectively packaged into both desirable and unpopular models with incredible efficiency.

Consequently, there has been an impact on the used car market, which is unsurprising considering the volume of new cars involved. UK buyers have been resisting the urge to purchase cars for some time so, although overall sales volumes have been good, it is the ‘late-plate’ area of the market that has been adversely affected. New car deals have been so attractive that a buyer originally conditioned to understand that it is better to buy a late-plate, low-mileage car to avoid the initial depreciation, has now been tempted to buy the new model.

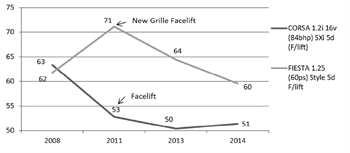

Residual value percentage at six months old | |

| |

This buyer behaviour has a direct impact on residual values in the small car sector. The data in the graph, right, represents the percentage of original cost of a six-month-old car with standard mileage in the month of September.

The residual value percentages have dropped from the peak of 62%/63% in 2008 to the current market position. Given that used car sales have been strong for several years, one would have expected a much stronger figure for a used car, even accounting for the impact of model life cycle.

production line")

Login to comment

Comments

No comments have been made yet.