By Philip Nothard

In researching what drives the market, I always ask, is it down to what manufacturers want to sell or is it about what the customers want to drive? Whether the answer is one or the other – or a combination of both – what might be the impact on profit margins throughout the network?

It is difficult to ascertain whether consumers are really in the driving seat when it comes to car choice. Manufacturers have priorities in terms of what they want to push at any given time, so there is a large element of buyers being steered by incentives and availability. Used car dealers are in a similar position, but the stakes are arguably higher. Not only do they have to compete with each other, this competition often pushes prices up – as we have seen again in recent weeks.

|

||

|

Philip Nothard joined CAP in 2010 as its retail and consumer price editor, analysing pricing data and interpreting strategic market trends. In his role, he is able to apply two decades of experience gained in franchised motor retailers, which culminated in running dealerships for the likes of European Motor Holdings, Lythgoe Motor Group and Arnold Clark. |

||

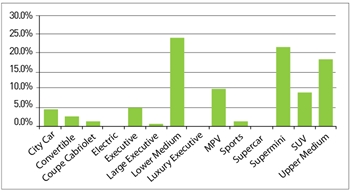

One of the ways to see whether what is available in the trade is automatically reflected in the retail market is to compare auction sales with retail advertisements. Clearly, the overall results would not be expected to diverge a great deal, but an interesting factor in current market data is the upper medium sector. Here we see a significant 5.5% more cars in the trade than are advertised for retail. Contrasting with this is a slight shortage of city cars in the trade, compared with what is being advertised.

Instinct may suggest there is more of a glut of upper medium cars in the trade because they are unwanted by the typical used car buyer, who is more concerned with economy. But it would be a mistake to write off upper medium cars as a poor stocking choice because further evidence reveals they have delivered higher average margins over the past 12 months than the more ‘in-demand’ city car.

Generally, the market shares of the different sectors have been steady over the past 12 months. SUVs, for example, have increased month-on-month from 7.8% in January 2013 through to 9.5% in January 2014 in trade volume share and 10.1% to 11.3% in retail over the same time period.

These small disparities between percentage share at trade and retail suggest dealers do not simply settle for what’s available in the open trade market and are increasingly looking elsewhere to source vehicles to fine tune their stock profile to meet customer demand.

The other interesting factor we find is the dominant sectors – upper medium, lower medium and supermini – are all in the bottom quartile of profit margins among the 14 sectors. Clearly, this is the main retail battleground and it is where margins come under the most pressure.

Trade share by sector – January 2014 |

|

|

|

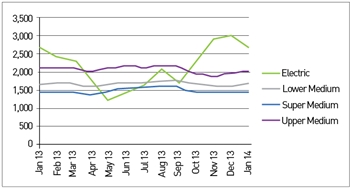

Retail margins - advertised retail to CAP clean (£) |

|

|

My research suggests dealers are increasingly looking to develop and diversify their stock profiling to improve margins. They see that when every dealer buys the same stock and offers the same vehicles to customers, competing on price offers ever decreasing returns.

One of my dealer contacts sums it up neatly: “We have counter-balanced by larger margins and better return on some of the more expensive and newer, lower mileage stock, which is just that bit different from what our competitors have.”

On average, since January 2013, the overall profit margin across all sectors has increased by about £227. However, for SUVs, margins have declined slightly, which you would expect when SUVs have become increasingly mainstream and therefore generate more competition.

The lesson – which many of my dealer contacts are already learning – is that one of the best ways to protect margins is to step outside of the crowd. Instead of buying what is immediately on offer, it is more profitable to cast a wider net and create your own niche.

Michael Moorey NFDA and Trusted Dealers - 20/03/2014 10:55

This reminds me of a conversation with a salesman stating that they "never did any good with Omega's", yet just 8 miles away another Vauxhall site were making hay from that very model. When asked how many they had in stock the salesman replied "None"