logo")

The UK’s financial regulator has reignited uncertainty across the motor finance industry after outlining the likely scope of a compensation scheme which could see payouts totalling as much as £18 billion for customers potentially mis-sold loans.

While the final cost of the redress scheme will hinge on its eventual design, the Financial Conduct Authority (FCA) warned that the bill is unlikely to come in below £9 billion - and could soar much higher.

The decision follows the August 1 landmark ruling by the Supreme Court which found that certain commission arrangements between motor finance lenders and dealers could have resulted in an unfair relationship with customers - particularly when high or discretionary commissions were not disclosed.

“Our detailed review of the past use of motor finance has shown that many firms were not complying with the law or our disclosure rules that were in force when they sold loans to consumers,” said the FCA which reckons that most car buyers will likely receive less than £950 in compensation.

"Where consumers have lost out, they should be appropriately compensated in an orderly, consistent and efficient way.”

Paul Hollick, chair, Association of Fleet Professionals, voiced the dismay of many in the industry following the August 1 ruling which had initially been welcomed as an excellent outcome, reflecting the critical role and responsibilities of intermediaries, lenders and customers, restoring certainty and clarity to the largest point-of-sale consumer credit market in the UK.

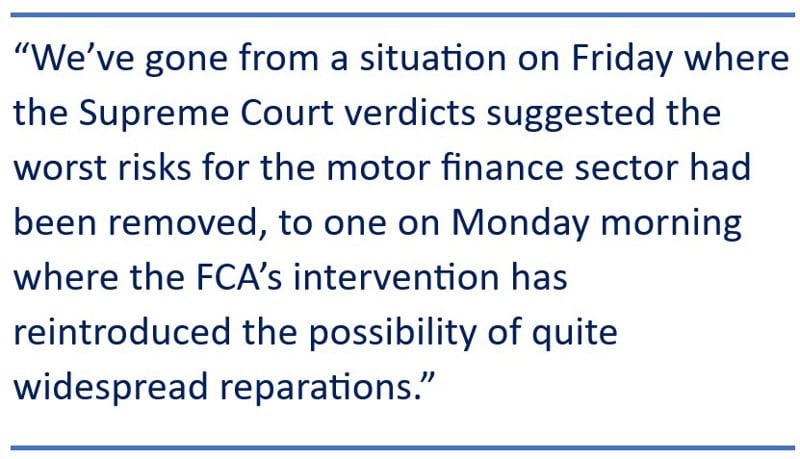

“We’ve gone from a situation on Friday where the Supreme Court verdicts suggested the worst risks for the motor finance sector had been removed, to one on Monday morning where the FCA’s intervention has reintroduced the possibility of quite widespread reparations.

"It means we’re going to remain in a situation of considerable uncertainty until the redress scheme is finalised in October.

“We’d like to see the whole situation resolved as soon as possible. Yes, consumers whose legal rights have been ignored should be recompensed fairly but the motor finance market also needs to return to normal functioning as soon as possible.”

At the heart of the issue are so-called discretionary commission arrangements (DCAs), which allowed dealers to adjust interest rates - often increasing them to receive higher commission payouts.

The Supreme Court found that such practices, if inadequately disclosed, could breach consumer protection laws.

Although not all commission-related features are inherently unfair, the FCA said lenders must now prepare for scrutiny over how arrangements were structured and communicated to customers.

Brian Nimmo, head of redress at financial services consultancy Broadstone, predicted last week that although the August 1 ruling was a partial win for a motor finance industry, providers "were not out of the woods yet".

"DCA cases will now need to be looked at on a case-by-case basis," he said. "The FCA is expected to develop its redress scheme to deal with this development but how it will help them decide if a case is ‘unfair’ is the great unknown.

“As a result, finance companies will still need to review all of their DCA cases, assess whether they are unfair and then calculate potential redress, which will be a significant exercise."

The FCA redress scheme is expected to cover both discretionary and some non-discretionary commission models and will what role factors such as commission size, customer sophistication, and disclosure quality should play in determining eligibility for compensation.

If implemented as planned, the scheme would apply to finance agreements dating back to 2007 - aligning with the Financial Ombudsman’s remit and aimed at avoiding a wave of court challenges.

If implemented as planned, the scheme would apply to finance agreements dating back to 2007 - aligning with the Financial Ombudsman’s remit and aimed at avoiding a wave of court challenges.

The FCA is also weighing whether the scheme should operate on an opt-in or opt-out basis. Either way, firms will be expected to actively notify affected customers.

"The FCA is rapidly messing this up and, if not careful, they will be the target for unfairness claims, never mind lenders and dealers," said automotive legal expert Jonathan Butler of Geldards.

The lawyer added: "Implementing anything other than an arbitrary scheme is one thing - and won't be straightforward - paying out is another. My guess is it will be well into 2026 if not beyond before payouts are made."

Compensation calculations are likely to vary depending on the specific harm suffered. The FCA is considering a method similar to the Supreme Court’s ruling in the Johnson case, where the lender was required to repay the commission in full. Interest payments on redress would be set at a simple annual rate of around 3%, based on average base rates plus 1%.

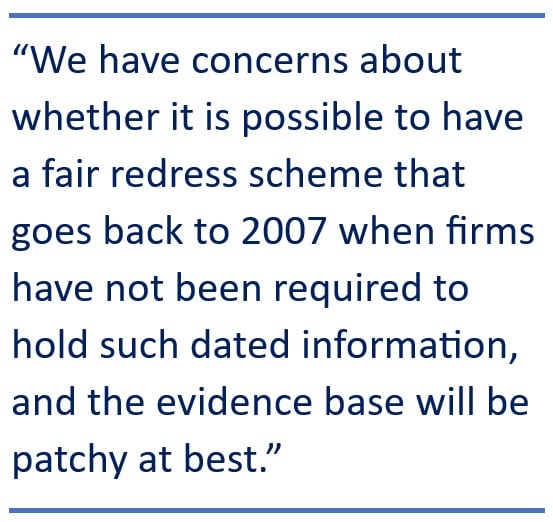

Adrian Dally, director of motor finance at the lending industry body, the Finance and Leasing Association, noted concerns over whether it is feasible to have a fair redress scheme that goes back to 2007 "when firms have not been required to hold such dated information, and the evidence base will be patchy at best”.

Ian Plummer, Auto Trader’s chief commercial officer, pointed out that while it may be some time before the industry knows exactly how the process of disclosing commission will be enacted, striking the right balance will be key.

“A pragmatic solution that minimises the impact on an industry that contributes billions to our economy, but also a consumer centric approach that ensures transparency and confidence for millions of buyers,” he said.

The FCA said it plans to launch its consultation in early October, running for six weeks. Final rules are expected to be in place by the end of 2025, paving the way for payments to begin in 2026.

Until then, firms do not have to respond to motor finance complaints before 4 December 2025 - a deadline that may be extended in line with the scheme’s timetable to prevent a surge in disjointed claims.

Speaking to sector analysts, FCA chief Nikhil Rathi confirmed that an annual 2 million customers rely on motor finance with lending of around £40 billion. “Between 2007 to 2020 … there were 25.9 million motor finance agreements, of which 14.6 million operated with a discretionary commission arrangement with around £8.1 billion estimated commission paid during that period,” he said.

AM Dealer Technology Guide

The AM 2025 Dealer Technology Guide enables UK motor retailers to read about a host of the latest software and hardware available from the industry's dedicated suppliers.

Keeping abreast of technology is a vital part of modern automotive retailing as the demands of customers and staff for rapid and efficient fulfilment only increases.

Industry suppliers have provided their highlights and summaries for the AM Dealer Technology Guide, and we give their web addresses to help you discover more.

Moreover, many of them will be at Automotive Management Live on November 12 at Birmingham NEC. Ensure you register to join us at our flagship exhibition.

Read nowAuthor:

Aimee Turner

Deputy editor

AM deputy editor Aimée Turner has been a specialist B2B editor and journalist covering the international transportation sector for more than 20 years.

She has specialised in the significant safety, regulatory, and environmental issues that impact advanced technology businesses in the pursuit of more efficient, safer and sustainable transportation modes.

Login to comment

Comments

No comments have been made yet.