By Philip Nothard

How many of us have sat there at some point and asked – why am I doing this?

As we know, 2015 has been a very good year for those in the new car sector – a week doesn’t seem to go by without positive headlines about profits, reinvestments or consecutive new car growth. Who can question any positive news about the car industry in the UK?

However, there are questions about the long-term impact of such large volumes of new cars on the overall industry. Will this level of new car growth, the increasing numbers of pre-registrations and the extremely attractive consumer incentives affect the profitability of used cars – principally the nearly-new sector?

Is the new car boom hurting other sectors?

The one-year-old market is certainly receiving pressure in 2015 from those market dynamics. Many operations are willing to take the risk and enter this sector of the market, as they feel that if managed correctly, in terms of stock profile and turn, there is profit to be made.

With the modern dynamics in the new and nearly new segment of our industry, what is happening elsewhere and how is it having a bearing on our daily business and, most importantly, on profitability?

Sentiment in the network is that a greater ‘cavity’ is emerging between large franchised dealer groups and the privately owned smaller franchised, and non-franchised independents.

Is there actually a divide or are we are seeing bigger economies of scale? As costs begin to increase, profit opportunities are removed, due to factors such as FCA involvement in GAP sales, rate spread, and more recently the Consumer Rights Act. In reality, these new influences are not directed at any specific sector, and are changing the landscape in which all dealers, large or small operate.

Costs are rising, profit opportunities shrinking

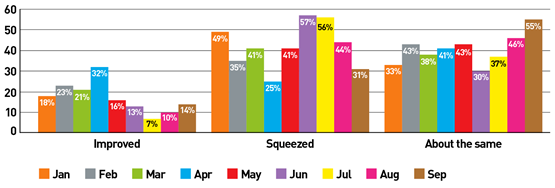

Retained margins compared with previous month

Margins have been under some pressure throughout 2015. As the graph, above, demonstrates, there have been months during the year where half or more of those responding felt they had been compressed again from the previous month. However, in recent months, this has begun to ease.

Costs have continued to rise, driven by the increased expense of advertising vehicles through a multitude of marketing platforms, costs incurred just to purchase the car, transportation, and preparing it to the level of condition that consumers have come to expect.

To put some of this into context, let me share some of the costs involved in the process of a vehicle purchase through to retail. On a £26,000 vehicle through a national auction centre, the administration fees are £565, excluding transport to the site. Then come incidentals, such as a 120-point inspection at £110. If the vehicle remains unsold for 40 days, the dealer stocking fees would be about £240. Advertising costs could be as much as £306. A professional detailed valet, costs on average £78 per vehicle. An eye-watering £1,299 and we haven’t mentioned any SMART repairs, tyres and more. All of this is before any business overheads.

Market dynamics are changing

The market dynamics have altered for many. Legislation surrounding the sale of GAP products has forced some dealers to cease offering it.

Coupled with this, you have controls over rate spread from finance sales and costs continuing to spiral just to have the vehicles on stock.

Subsequently, with the profit opportunities for finance and add-on commissions easing, and the Consumer Rights Act taking effect on Oct 1, which will alter the way in which many dealers prepare and document what they do, in some cases it raises the question whether what they do is enough?

Conclusion

The new car market is showing no immediate signs of easing. CAP and others are watching the nearly new market extremely closely as the consumer incentives continue. Used values held steady through the year, which has added further pressure to the margin between what it costs to take a used vehicle from its raw state to retail-ready, for an increasingly demanding and savvy consumer.

It is clear that margins are increasingly an issue, and we see a reliance on ‘chassis’ profit on the rise. Dealers are searching out alternatives to how they purchase vehicles, in the attempt to alleviate those increased buyer’s fees, and where they advertise them with greater use of social media platforms.

In these increasingly complex times, as was ever the case, what profile a dealer sells and how long they keep it, remains a key driver of profitability.

Login to comment

Comments

No comments have been made yet.