Consultation and not dictation is the way Volkswagen sets targets, says Alex Smith (pictured), the brand’s UK director of passenger cars.

Smith, who until July 1, 2014, was director of Volkswagen Commercial Vehicles, defends his target-setting and retailer margins, outlining how talking to his network fosters appreciation of his goals and helps to establish a consistent, customer-focused sales agenda throughout the brand’s 208 dealerships.

Jeremy Bennett: How would you describe Volkswagen, encapsulating what it stands for?

Consultation and not dictation is the way Volkswagen sets targets, says Alex Smith (pictured), the brand’s UK director of passenger cars.

Smith, who until July 1, 2014, was director of Volkswagen Commercial Vehicles, defends his target-setting and retailer margins, outlining how talking to his network fosters appreciation of his goals and helps to establish a consistent, customer-focused sales agenda throughout the brand’s 208 dealerships.

Jeremy Bennett: How would you describe Volkswagen, encapsulating what it stands for?

Alex Smith: Globally, as well as in the UK market, VW stands for brilliant products and fantastic engineering. But it’s not technology for technology’s sake: it’s technology for the customers’ benefit. In terms of our approach in the UK, I think we are balanced. I think we are thoughtful and everything we do, we do with a view to long-term sustainability.

JB: What would be an example of this approach?

JB: What would be an example of this approach?

AS: The investment we have been making over the past few years in the digitisation of the sales and service process – the blended retailing concept, assimilating digital technology and the physical showroom experience. We knew it might not pay back in the first month or the first three months, but over the long term it gives us – and, very importantly, our network and our customers – real customer and commercial benefits.

In 2011, when we were originating this project, we never thought it would win us headlines or deliver stunning, visible business results in the first few weeks or months. It was a huge amount of effort for long-term gain and we are seeing some of those gains now.

Another example is our strong residual values. If you compare them with other brands in the volume car market, our residual values are good and that has clear customer benefits in terms of cost of ownership.

JB: You’ve highlighted a strength. What are the weaknesses, and therefore the opportunities?

AS: We grew unit volume by more than any other manufacturer last year. We have fantastic new products coming and we’ve got a very loyal ownership parc, which has grown significantly out of the recession.

So one thing we have to be very conscious of is that, in our network, we are resourced both in terms of numbers and skills to ensure we continue to give really high quality customer experiences because this business has grown and the throughputs per retailer in the past few years has grown very strongly.

JB: How significant would you say the growth has been?

AS: If you look at retail numbers now, compared with during the depths of the financial crisis, throughput per retailer is almost 50% up. While I don’t see it as a weakness – customer satisfaction levels are showing a strong, upwards trend – it’s something I have to be exceptionally conscious of because the scale of each individual business has changed very significantly in the past three years.

JB: Are you concerned the network is able to cope? Has it grown in its skills and abilities to match the demand of throughput?

JB: Are you concerned the network is able to cope? Has it grown in its skills and abilities to match the demand of throughput?

AS: It has. If you look at the various elements of customer satisfaction on the sales side, we are seeing decent upward trends.

JB: Is it as simplistic as being confident that, in the face of increasing throughput, each customer gets the right amount of attention from the dealer every time?

AS: That is part of it. But it’s also important to recognise that what a customer needs from a dealer has changed quite significantly over the past few years.

Certain elements of the traditional sales process are now far more important than they were and others less so. I’m sure everybody has got their view on the exact number, but in the past four to five years, the number of people walking in through the doors of a retailer and making an enquiry about a new car is broadly half what it was.

So, perhaps qualification and detailed product demonstration are less important to some customers because they have accessed the information via the web. But other parts of the process – explaining finance options, which has to be done extremely carefully in a highly regulated environment – perhaps require more time and emphasis.

Ensuring each customer gets the right amount of attention, not just while they are in the showroom, but also in that period between placing the order on the car and receiving the vehicle, is still paramount. It’s the basics of retailing.

JB: How do you ensure dealers meet your and the customers’ requirements?

AS: The first contact the majority of customers will have with the manufacturer is the website. So making the website easy to use, making the right information easy to access and very clear, gets a huge amount of attention from us. We have also got further developments this year in terms of how intuitive and how customer-focused our configuration tool is.

Once you move into the physical network, we’ve engaged a huge amount with our network, co-developing tools that lead to a fantastic ‘blended retailing’ experience.

We’ve said to dealers: “You are closest to the customers physically, so what tools do you need in order to meet the expectations of a modern retailing experience?” They have given us fantastic feedback and led us to close down some projects we thought might be tremendously important and focus on others that maybe hadn’t occurred to us. We have taken a huge amount of feedback from our network and have co-developed the 15 or so tools that make up the ‘blended retailing’ experience.

We also have a programme called ‘Volkswagen Voice’, which enables good monitoring and proactive feedback from coaching of telephony skills within the retailing network, and a number of structural programmes that help with finance renewals and other sources of sustainable business.

The traditional answer a few years ago might have been: ‘We send the area manager in and they take a look at resource and they do some coaching and give their opinion and they write it in the visitor report and then maybe, we’ll come back in two weeks to review.’

Now, it is much more structured. That’s not to say the area manager still doesn’t have an important role. They have a crucial role in maintaining the relationship between manufacturer and the retail network.

However, we now have a number of co-developed structural programmes, which give the retail network really good intelligence on where the pressure points are in the business and where the opportunities to develop are.

JB: Is there clear evidence ‘blended retailing’ is working? Is it delivering a return on investment?

AS: I’m not going to give you exact figures, but we have very strong evidence that customers who experience ‘blended retailing’ rate us higher for customer satisfaction. There are also commercial benefits.

JB: Andrew McMillan, the former head of customer service at John Lewis, suggested asking a customer what use they are going to put their new car to, instead of what car they want. Then, considering their lifestyle, guide them on a choice of vehicle that takes into account children, caravan, bikes, golf clubs, baby buggies, etc. Is this an accurate description of the Volkswagen approach?

AS: Exactly. Assuming the first contact with the car brand will generally be a website, most car configurators are set up the way a manufacturer would build a car. This makes the assumption a customer knows you have a Tiguan Match and a Tiguan R-Line, whereas in fact, they may not even know that you’ve got such a car.

But if they need space, a high driving position, and 4x4 capability occasionally, then the right vehicle for them may well be a Tiguan. You have to lead people through a configuration process, through a consultancy and sales process, based on their needs from the vehicle, rather than how a manufacturer would assemble a vehicle in a factory.

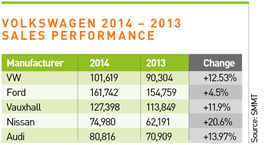

JB: What drove the extraordinary success in the UK new car retail market for Volkswagen – PCPs, consumer confidence, pent-up demand, great products and offers? Or a combination? The market share of your two biggest rivals, Ford and Vauxhall, may be higher, but they have not proved as resilient.

AS: I think shortening of the trading cycle because of the prominence of PCP offers did have an influence, allied to greater consumer confidence.

Then if you compare our first- and second-half performance, the latter was particularly good. The revised Polo, introduced around the middle of the year, really started to fly and still is.

JB: Why did it resonate in a market full of new, refreshed or facelifted cars?

AS: There are lots of very loyal Polo customers probably anticipating the revised model with better economy and a real step-up in infotainment quality.

In that segment of the market where PCP is particularly prominent, there were lots of people who bought Polo two or three years ago who were, because of its fantastic residual value, in a position where the cost to change was very low.

More holistically, we are not over-reliant on one particular channel in the market – rental, fleet or retail – and it means we go to market in a stable and sustainable way.

We won’t mask our performance: ‘the market share hasn’t grown because we had a new product which was particularly successful in retail, so we decided to take a few thousand units out of rental because we didn’t really feel like we should be doing those anyway’. This is not how we operate. We are not over-represented in any channels. So, if we see genuine performance improvement on model life-cycle measures, they’re reflected in the market share.

JB: What are you predicting in growth terms for 2015?

AS: A slight improvement. When you go into an election year there is always a little consumer uncertainty. Considering the macroeconomic factors, we have relatively low unemployment, a low inflation forecast and slight wage inflation – but there is no real fundamental shift between the 2015 outlook and 2014.

JB: What are the threats to your business plan’s success?

AS: The most fundamental threat to anybody’s business is complacency and that is something we work very hard to eradicate from the business. The competition is not going to lessen, so you get up every day and think of things you could do better. You work harder at them and you work collaboratively with the network, ensuring that you get better at customer satisfaction and become even more efficient in your processes.

JB: Through AM’s meetings with dealers and roundtable discussions, there have been a lot of comments about the forcing of the market – targets are being brought forward, with huge financial incentives tied to them. Are you insisting on targets that some retailers would say are unreasonable and not appropriate to the genuine, retail market?

AS: We are not doing that. The reason objectives or targets are important and the seasonality of those targets is important is because it enables us to plan production and get the right vehicles into the country at the right time.

The way we plan our objectives is really, really straightforward. We look at historic performance and then we will either build in or exclude a number of effects, which will be generally related to the life cycle of the vehicle and our positioning in each of the channels we are competing in.

For example, we’ve had a view for a number of years that we could probably do better with Tiguan. So we looked at its historic performance and talked to the dealer council, telling dealers we were going to reposition it versus its key competitors and therefore expected we would get a certain volume growth from it.

In addition, we ran a two-week SUV campaign in February. We knew from historical performance this would lead to a sales uplift. So if we take our base performance, the repositioning and the amount of campaign activity we were going to put into it, we forecast a target figure. In this case, the dealer council said: ‘We buy that in terms of the volume, your aspirations. But it is still quite a big jump, so what we would like you to do is give us some surety about supply and bonus conditions on the vehicle’. A debate takes place.

So if you look at where the objectives are for 2015 in the Volkswagen retailer network, they are very similar to the trajectory we were on in the second half of 2014. The key is, what is our order entry position and our forward order bank coverage because that is the best indication of the business’s health.

JB: Are Q1 2015 targets up on 2014?

AS: The objectives are higher. We have a very young, revised Polo, the new Passat and we, with our network, decided we were going to focus on our SUVs in Q1.

JB: Is the network more profitable than a year ago? Is there a squeeze on dealer margins to support the PCP offers?

AS: Our dealer margins are consistent year on year. It is difficult to talk about dealer margins without thinking very carefully about what I am saying, but I would refute what you are saying.

The profitability in the Volkswagen network over the past two years has been very consistent. Beyond new car sales, the progress the network has made in used vehicles over the past three years has been stunning. Dealers have done a very good job of investing in the Das Welt Auto branding, their own retail sales processes and becoming very market-intelligent in the way they market our approved used cars.

JB: What’s new in the blended retailing concept?

AS: There are improvements coming later this year. A major focus is digitisation of the service process, making sure service has the same prominence in our digital thinking, in our connected journey, as sales has had for a couple of years. We are developing a digital service reception that we will roll out this year.

The service process has been unchanged for a long time. It generally involves walking into a service department and sitting down at a desk, there being a big computer on the desk and things being keyed in and dot matrix printers whirring. It doesn’t need to be like that. Why wouldn’t the service experience match the smoothness and interactivity of any other retail experience?

JB: Talk me through the journey as an aftersales customer.

AS: If your service is coming up, traditionally, you may get a postcard with a service reminder on it, an SMS message or a phone call. But isn’t there a way in which you can achieve a greater level of personalisation and appropriate timing in the communication of the service experience?

We have the solution and it is in pilot at the moment with six retailers of differing sizes and locations. The customer feedback is really good. I’ll be able to reveal details in Q3.

JB: Isn’t blended retailing a compromise – a fudge – because you don’t know what the future will mean for retail, whether it will it be digital or whether it will be premises? You are putting investment in both, because you are not really sure which way the market or the customer requirements will go.

AS: Human interaction is still fundamentally important, whatever the purchase is. I don’t think there comes a point, in my lifetime, in which the human is taken out of the sales process, but the emphasis and their importance at different parts of the sales process has changed and is changing very, very rapidly.

Technology and digitisation of the sales process is really important because I think there are some things you can’t demonstrate with words. It is massively helpful in order to demonstrate what a vehicle can do and how it’s enhancing your driving experience without you even being aware of it.

And the retail environment you invite customers into is important. There wouldn’t be a retail interior design industry if it wasn’t important.

Displaying vehicles really well and using technology in the showroom to explain their characteristics, then ensuring that the customer can drive what they want to drive before they buy it, is fundamentally important.

Volkswagen's technology in action

Parking assist

The new Volkswagen Passat uses ultrasonic sensors to help motorists park in the tightest of spots.

Area view

Wide-angle ‘invisible’ camera technology allows drivers to see the entire space around their car.

Side assist

Sensors that eliminate blind spots and warn of approaching traffic before changing lanes.

City emergency braking

Automatic collision-avoiding technology can brake if the driver does not.

Login to continue reading

Or register with AM-online to keep up to date with the latest UK automotive retail industry news and insight.

Jeremy has been a journalist for 30 years, 20 of which have been in business-to-business automotive.

He was a writer and news editor on AM-sister brand Fleet News for three years before setting up the AM website.

For the last seven years he has been Bauer B2B’s head of digital helping to manage the digital assets of Fleet News, together with AM and RAIL.

In 2025 he was an Association of Online Publishers awards judge.

Login to comment

Comments

No comments have been made yet.