The Financial Conduct Authority has published its finalised rules for consumer credit companies.

They include a stipulation for commission disclosure to customers before they sign a credit agreement.

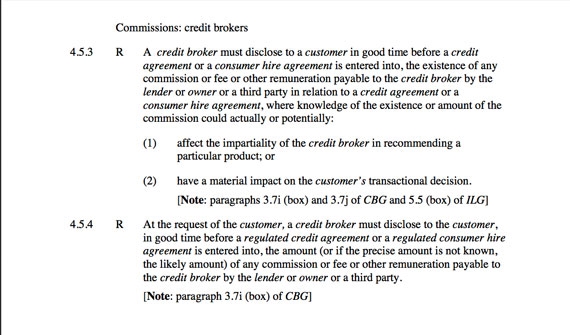

That is required if the dealer is acting as a finance broker and that commission could potentially affect the impartiality of the dealership, business manager or broker in recommending a particular product, such as if it will earn him more than other suitable products, or could have a material impact on the customer's transactional decision.

Separately, if a customer requests, prior to the agreement being signed the dealer/broker must disclose the amount, or likely amount, of any commission, fee or other remuneration payable to them by the lender or third party (view documentation).

The FCA has also clarified that, where practicable, firms should facilitate customers shopping around for credit by offering a quotation search facility.

They should also, when undertaking a credit reference search, not leave evidence of an application on file where that customer is not yet ready to apply, due to it potentially damaging the customer's credit history.

All complaints regarding motor finance, including verbal ones, that cannot be resolved in the same business day must also be logged and reported by firms with full FCA permission.

Dealers with less than £5m annual revenue from credit-related regulated activities will be required to submit reports annually, those with larger revenues will report more regularly. Records must be kept for three years.

Under the new regime, which starts on April 1, consumer credit providers will need to ensure that they give customers the right information to make informed choices, that their services meet consumer needs, and that people in difficulty are treated fairly.

“Our new rules will help us to protect consumers and give us strong new powers to tackle any firm found to be overstepping the line," said Martin Wheatley, FCA chief executive.

"The FCA will take a tough approach to consumer credit with stronger powers to clamp down on poor practice than the previous Office of Fair Trading regime.

"Our supervision of firms will be hands on and we will closely monitor how providers treat their customers, in particular those operating in higher risk sectors such as credit cards, debt management and payday.

"We will respond quickly to any issues that are identified and there will be swift penalties for any firm or individual found not to be putting consumers’ interests first, including possible enforcement action and consumer redress."

He said the rule changes announced today will give consumers additional protection from rogue practices and put the onus on credit providers to ensure that they treat customers fairly at all times.

The FCA also said that firms are expected to comply with the 'spirit' of its rules, and not merely the 'letter' of them.

Commenting on the new consumer credit rules Fiona Hoyle, head of consumer finance at the Finance & Leasing Association (FLA), said: “It is obvious that the FCA has listened to a number of FLA concerns and injected a much needed degree of proportionality into their final rules to reflect the diversity of customers and products in the credit market.

“However, today’s package of almost 700 pages will take some time to analyse before the shape of the regime can be fully judged.

“For the 50,000 firms which have only a month to ready themselves for the new regime, this will be a daunting time.”

Click here to download the FCA's final detailed rules for consumer credit.

An award-winning journalist and editor, with two decades of experience covering the motor retail industry, and accredited by the Institute of Leadership and Management (ILM) plus the National Council for the Training of Journalist (NCTJ)

As editor of AM since 2016, Tim is responsible for its media content, planning and production across AM's multiple channels, including the website, digital reports, webinars, social media and the editorial content of AM's events, Automotive Management Live and the AM Awards. His focus is on interviewing senior leaders of franchised dealer groups and motor manufacturer national sales companies to examine latest developments in UK motor retail.

Bradley Wyatt - 28/02/2014 13:40

Can you direct us to the specific page of the document detailing commission disclosure