Car retailers were unable to take advantage of a milder February on their forecourts as profitability statistics published by ASE showed a £19,600 loss during the month – matching 2018’s performance.

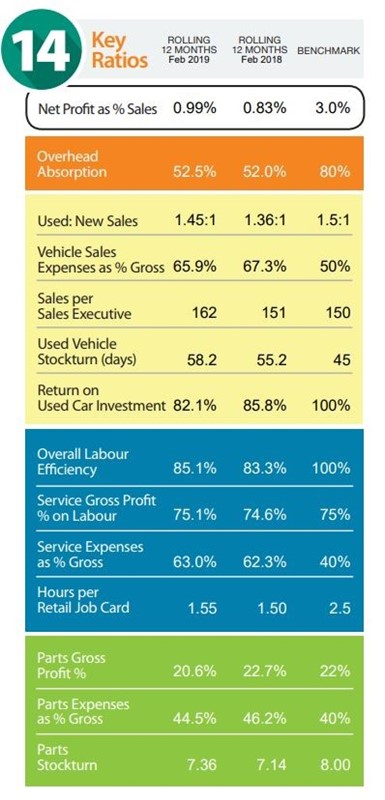

While retailers were able to improve their return on sales figures from an average of 0.83% to 0.99%, profitability remained static year-on-year, according to ASE’s monthly report, as the ratio of used-to-new sales rose from 1.36 to 1.45:1.

ASE chairman, Mike Jones (pictured), predicted a Q1 fall in new car registrations of around 3% as he noted that February is “a tough month for UK motor retailers”, with its shortage of working days, frequently inclement weather and focus on hitting March’s sales targets occupying retailers’ attention.

ASE chairman, Mike Jones (pictured), predicted a Q1 fall in new car registrations of around 3% as he noted that February is “a tough month for UK motor retailers”, with its shortage of working days, frequently inclement weather and focus on hitting March’s sales targets occupying retailers’ attention.

But he added: “Whilst there was no significant snow disruption in 2019, UK motor retailers matched their performance from February 2018, producing a loss of £19,600 for the month.”

Retailers’ added focus on their used car operations amid falling new car registrations volumes was evidenced by higher used car stock levels during February, according to Jones, but average days to turn stock rose from 55.2 to 58.2 during the period.

Dealers’ return on used car investment reflected this, falling from 85.8% to 82.1%.

Jones noted, however, a reduction in stock investment of 13% by the end of February.

He said: “This is an area which still needs to be monitored, with stock investment currently 17% up year-on-year. Given the significant used profit opportunity this is not necessarily an issue but the cars must be kept moving.”

Jones was also hopeful of seeing retailers achieve improvements in their overhead absorption rates during 2019.

He said that years of rising overhead costs may be coming to an end after identifying a stability in the overall back page cost during the past two months.

“For the majority of brands we have seen the end of the significant facility cost increases and, whilst there may be a rise as a result of increasing utilities cost, we should see growth in overhead absorption as a result,” Jones said.

Summarising his outlook for the months ahead, Jones added: “The result for March remains uncertain. The overall registration level looks like being 3% behind the prior year, with similar levels of self-registrations as we saw in 2018. There is, however, significant variance between brands, with double digit gains and falls amongst different franchises.

“Used car and aftersales profitability should provide a solid platform for profit improvement, particularly when allied to the stable cost base noted above. The key will, however, be new car profitability and the all-important bonus earnings.”

Login to comment

Comments

No comments have been made yet.