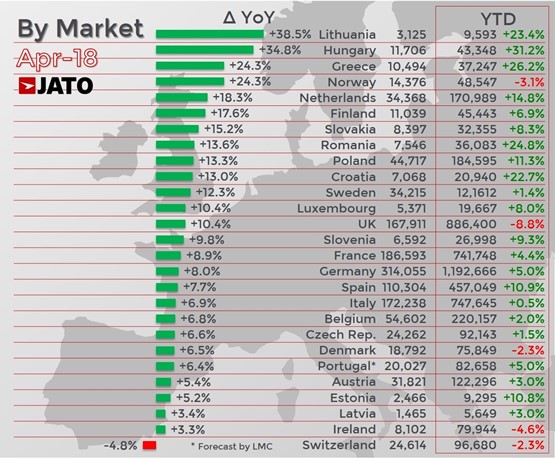

The UK was once again able to contribute to new car registrations growth in the European market as the region saw volumes rise by 9% overall.

As reported by the Society of Motor Manufacturers and Traders earlier this month, the UK market returned to growth with a 10.4% uplift in sales last month as a result of last year’s market slump following a rush to beat changing VED road tax regulations in March.

The result meant that the UK was able to contribute to growth which saw 1.34 million cars registered across Europe in April, taking the year-to-date total reached 5,607,856 registrations, an increase of 2.5% year-on-year with the biggest month-on-month rise in volumes since last March.

The figure represented the best April performance for the region since 2008.

Switzerland was the only market to register a decline.

Switzerland was the only market to register a decline.

Felipe Munoz, JATO’s global analyst, said: “April 2018 was an abnormal month, as many unusual factors helped to accelerate growth.

“However, these results show that there’s a positive mood among both consumers and car makers, as more models hit the market and more alternatives to diesel cars become available.”

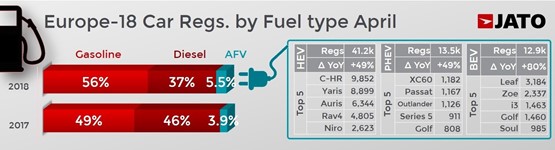

Jato’s car registrations data from 18 markets showed that diesel registrations continued to fall in April, with volume down by 13.2% to 453,500 units – a market share of 36.7%.

Petrol-powered vehicle sales continued to climb, however, rising by 53.5% to 692,300 units – a market share of 56.1% as alternative fuelled vehicles also continued to gain traction, with volumes up by 53.5% as they counted for 5.5% of total registrations.

Petrol-powered vehicle sales continued to climb, however, rising by 53.5% to 692,300 units – a market share of 56.1% as alternative fuelled vehicles also continued to gain traction, with volumes up by 53.5% as they counted for 5.5% of total registrations.

SUVs were, once again, the best-selling segment in 24 of the 27 markets analysed by Jato.

SUV volumes generated double-digit growth in 25 markets and a huge 116% increase in Croatia.

Small SUVs accounted for 166,700 registrations, their volumes boosted by 45% following the arrival of the Volkswagen T-Roc, Dacia Duster, Citroen C3 Aircross, Opel Crossland, Seat Arona, Kia Stonic and Hyundai Kona.

Compact SUV’s volume increased by 27%, which equates to 40,000 more units than in April 2017.

Jato revealed that the segment remains the top-selling type of SUV in Europe, with April volumes delivering double-digit growth driven by strong sales of the Peugeot 3008, Ford Kuga, Toyota C-HR, as well as new arrivals like the Skoda Karoq, Jeep Compass and Opel Grandland.

Jato revealed that the segment remains the top-selling type of SUV in Europe, with April volumes delivering double-digit growth driven by strong sales of the Peugeot 3008, Ford Kuga, Toyota C-HR, as well as new arrivals like the Skoda Karoq, Jeep Compass and Opel Grandland.

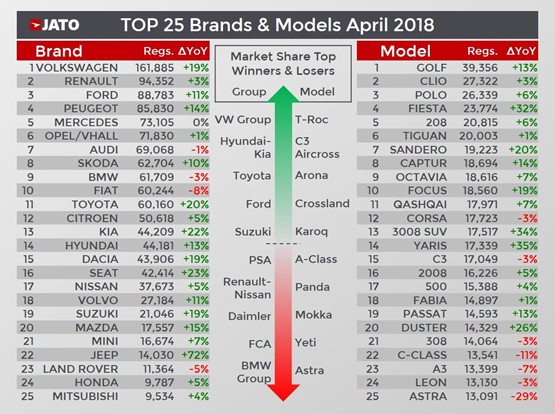

For the second consecutive month, Volkswagen Group gained the most market share across Europe, jumping from 24.9% in April 2017 to 25.7% in April 2018.

Jato attributed the growth to strong performance to the SUVs of the Skoda, Seat and the Volkswagen brands.

Hyundai-Kia posted the second largest market share gain, as its volume grew by 17.4% to 88,400 units. It was the sixth largest car maker in April, however there was only a marginal gap between them and FCA, who recorded 89,100 units and came in fourth place.

Premium car makers like the BMW Group and Daimler lost ground as a result of double-digit falls in their midsize and compact models. Their market share also suffered as a result of minimal growth in the premium car segment, which increased by only 1.7% in April to 297,800 units.

Volkswagen’s Golf was once again the most popular model in Europe, but the new T-Roc continued to climb the rankings and recorded the highest volume from the market’s newest additions.

The small SUV recorded 12,950 registrations and was the 26th best-selling car in Europe during April.

Login to comment

Comments

No comments have been made yet.