The retail consumer is a fickle animal and even more so in a month of outstanding weather and sporting focus.

As such it is perhaps little surprise that the new car market posted a drop of 3.4% in registrations this month.

Sales to the private market were 0.6% lower in June 2018 than they were last year and the private sector now rests at 4.9% lower than the same period last year in registration terms, although market share as a whole has improved by 0.6% to register 44.7% of the total market.

This is of note as the fleet sector is not performing as well at the moment although expectations are that it will improve later in the year.

With diesel new car registrations still on a heavy downward trend the subjective discussion in the wholesale market consistently points at a lack of consumer demand for diesel product in the used car market.

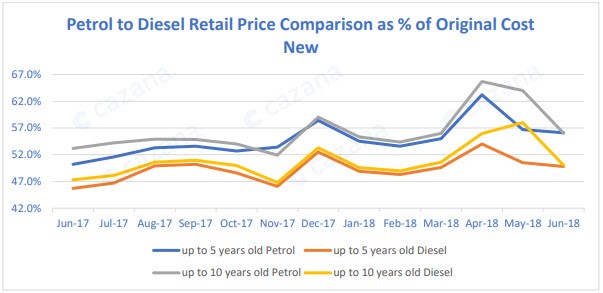

In recent months Cazana have focussed on a generic market measure, but for June 2018 the chart below is a little more specific and shows performance as a percentage of original cost new for all vehicles up to five years measured against vehicles up to 10 years in age:

The chart demonstrates there is little change in the pattern between the two different age sectors and this is important as it suggests that for the moment older vehicles are still not negatively impacting on demand.

The delta between pricing performance for petrol and diesel cars up to five years old has increased by 1.8 percentage points in comparison to June last year and for cars up to 10 years old this delta has actually decreased by 0.9 of a percentage point.

The chart is also interesting because it demonstrates that retail pricing for all diesels up to 10 years old have been more robust than diesels up to five years old although this pattern is similar if less pronounced for petrol cars.

There are two possible reasons for this, firstly that there has been greater consumer demand for older diesel product or secondly that the market may have experienced a short-term imbalance of desirable premium diesel cars that tend to return a higher percentage of original cost new.

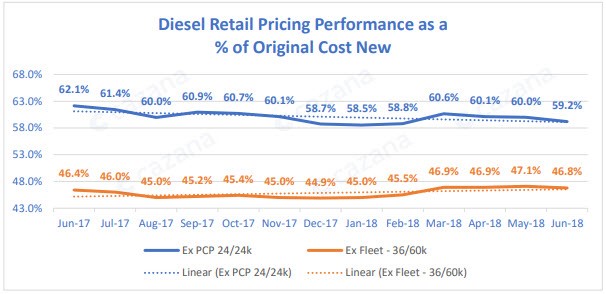

To put a closer focus on this the next chart compares performance of typical ex-PCP and ex-fleet cars in the consumer market by comparing the retail percentage of original cost.

The chart may show the beginning of the long-mooted decline in values for the ex-PCP sector as the trend shows that over the last 12 months values have been on a downward trend.

Whilst this data looks at the sector at a high level and is focussed on diesel product there has been a 2.9 percentage point reduction in retail pricing as a percentage of original cost new.

This is likely to be due to the volume of this product returning to the market and a more detailed view of specific OEM and range data will provide essential detail.

Conversely there appears to be continued strength for ex fleet models at the traditional 60k contract mileage with a stable trend line and an increase of 0.4 of a percentage point in comparison with June 2017.

It is possible that this is a direct result of fewer cars of this mileage profile returning to the market as ex-fleet mileages appear to be declining at this age.

In summary, June 2018 has been another good month for the retail used car market although prevailing trading conditions appear to have been harder for the dealers thanks to the weather and the World Cup to name just two distractions.

Profit opportunities are still there and wholesale stock volumes have increased marginally resulting in lower conversion rates at the auction.

Author: Rupert Pontin (pictured), director of valuations, Cazana. Data from Cazana.com – driven from live retail pricing.

Login to comment

Comments

No comments have been made yet.