A lack of “good quality and desirable stock” has not been enough to stall rising used car prices as demand from consumers defies the uncertainty caused by Brexit, according to Cazana.

In his monthly report of the used car sector, Cazana valuations director, Rupert Pontin, explains that car retailers look set to continue to perform well in what currently remains “a profitable place to be”.

The used car market and activity in the last few weeks has been less positive than normal for many at this time of year.

There has been a lack of good quality and desirable stock in the wholesale market and demand in the retail market has been consistent meaning for some cars there has been an increase in retail pricing driven by an uplift in consumer demand.

However, there is little doubt that the retail consumer is more difficult to close at the point of sale at the moment.

Getting the customer through the door is just part of the process and it is in the latter stages where commitment seems to be less strong than in recent months.

Anecdotal feedback is that Brexit is cause for concern and this is probably a valid reason for some buyers but the wiser buyers seem to also be capitalising on this as a starting point for a better deal.

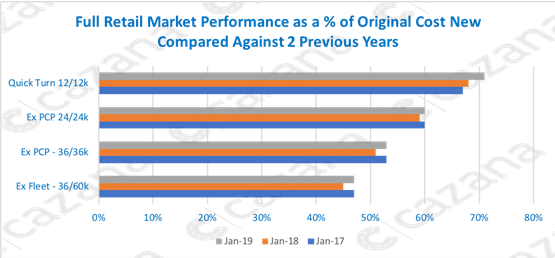

This chart, compiled from data gathered by Cazana, is interesting as it shows a unique trend across three of the key market profiles.

This chart, compiled from data gathered by Cazana, is interesting as it shows a unique trend across three of the key market profiles.

Whilst it is clear that retail pricing levels in January 2019 have improved over the same period last year, it is of note that in all but the ‘quick turn sector’ retail pricing as a percentage of original cost new is now at the same level as it was in January 2017.

It is likely that the ‘quick turn sector’ is still enjoying the retail pricing advantages of having less pre-registered stock in the market allowing for higher pricing.

Customers in this sector are in part those who can’t get a new car because of WLTP supply driven constraints.

Strength in the very young car market can often lead to a general rise in retail pricing so the next few months will be interesting to watch.

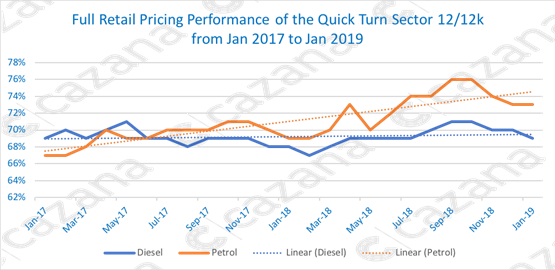

The next chart looks at performance in the Quick Turn sector by fuel type:

Given the strength in the ‘quick turn sector’, the previous chart is worth appraising to see what has happened to retail pricing over the previous two years when split by fuel type.

Given the strength in the ‘quick turn sector’, the previous chart is worth appraising to see what has happened to retail pricing over the previous two years when split by fuel type.

The first point of interest is that until mid-2018 the residual value performance of the diesel and petrol variants was very similar.

The trend is for petrol prices to continue to increase in this sector and bearing in mind much of the activity at this age and mileage is rental, body shop and courtesy car fleets this is not a real surprise.

The second point of interest is that diesel residual value performance has been consistent and this may come as a surprise to many.

At 69% of original cost new in January 2017, the figure remains the same in January 2019 although it is important to highlight that over the same period petrol performance has improved from 67% to 73% of original cost new which is an increase of 6 percentage points which is remarkable.

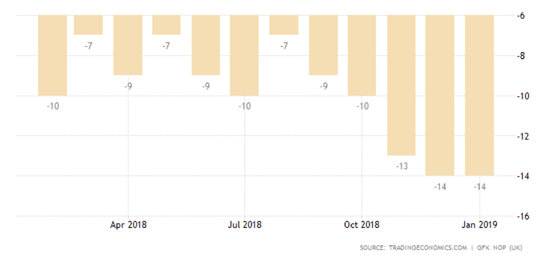

With such continued retail pricing strength in the market it is often difficult to understand how this is being achieved under the current economic conditions.

Brexit is ever closer and an agreement ever further away. Consumers are worried as the Consumer Confidence chart below shows:-

But it would seem that despite confidence being at a 12 month low, cars are still selling and for high retail prices.

But it would seem that despite confidence being at a 12 month low, cars are still selling and for high retail prices.

Therefore, there must be a catalyst that is keeping the market moving and it would seem that this might well be the change in ownership patterns.

Working on a deal with straight HP can provide a scary looking monthly figure these days but using the ever-increasing number of used car PCP products might just be the way that retail pricing and sales success is being perpetuated.

The FLA confirm that used car finance penetration is at one of the highest ever levels.

Finance companies are working hard to make sure that they are as accurate as possible on the Guaranteed Future Values and put all these factors together and taking a PCP on a used car looks more appealing than it has done in many years.

In summary, January has posed its own challenges in both the new and used car markets. New car sales should be better balanced this year and the coming months will see whether that will be the case, although supply and demand factors should resolve themselves in the coming weeks and a more balanced year in volume terms is very likely.

The used car market whilst harder in recent weeks will continue to be a profitable place to be, especially as finance companies use more live and intuitive unedited market data on which to base future values thus driving ownership costs down.

Login to comment

Comments

No comments have been made yet.