The Financial Conduct Authority (FCA) is proposing a number of changes to the way general insurance products are sold in the dealership, which could massively affect the sale of GAP at the point of sale.

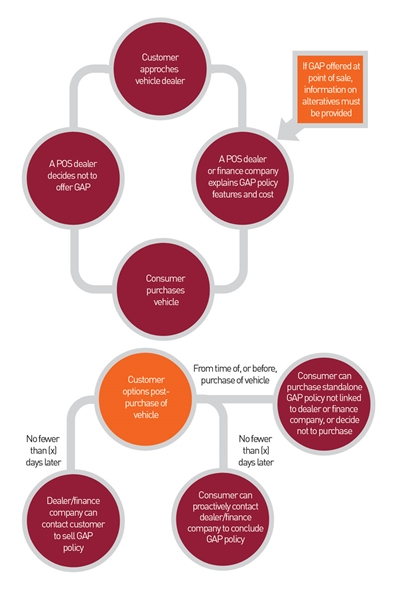

It could mean that while dealers can explain and offer GAP when selling a car, it cannot be sold when the car is purchased. Customers can walk away with details of a dealership’s offer, but must be told alternatives are available. The customer can then get in touch with the dealer to buy GAP at a later date or the dealership can contact the customer about the GAP policy after a number of days have passed (the amount is still to be determined by the FCA).

NEED TO KNOW |

|

| ♦ Proposals could restrict dealers to offering information | |

| ♦ The FCA estimates overpaying for add-on products costs consumers £200 million a year across all industries | |

The FCA has put together a 69-page document of proposals following its investigation into the general insurance add-ons market. Since the inquiry began in July 2013, the FCA has analysed evidence about companies and consumers in the travel, gadget, GAP, home emergency and personal accident add-on insurance markets.

The FCA reviewed the experiences of more than 1,000 consumers and carried out behavioural research to understand if buying decisions were affected by different sales tactics. The FCA also reviewed product literature, sales, pricing, profitability, and claims.

The FCA believes it is currently too complicated to compare packages of products with separate prices in the showroom and believes there is a lack of transparency about add-on cover and price.

The FCA has estimated that consumers are overpaying for add-on products up to the value of £200 million a year across all industries.

A spokeswoman for the FCA said the changes were proposals at this stage and a decision will be made on how the industry will proceed after it gathers feedback.

'Firms must stop seeing consumers as pound signs'

How the FCA wants GAP sales to work |

|

|

|

|

Other products that may be affected♦ RTI (return to invoice) insurance ♦ MoT insurance ♦ Alloy/tyre insurance ♦ SMART insurance |

The FCA’s investigation was initiated against a backdrop of a series of actions tackling the mis-selling of products sold as add-ons, including payment protection insurance (PPI), card protection, identity theft protection, personal accident, home emergency and breakdown cover products.

While the proposed changes affect the sale of all general insurance add-ons, FCA communications highlighted GAP insurance in particular as a target.

Christopher Woolard, director of policy, risk and research at the FCA, said: “There’s a clear case for us to intervene.

Competition in this market is not working well and many consumers are simply not getting value for money. Firms must start putting consumers first and stop seeing them as pound signs.

“We believe our proposals will address these issues and prevent consumers paying for poor-value insurance products that they may not need or use.”

Dealers have until April 8 to send feedback to the FCA.

Why focus on GAP?

The FCA said the particular circumstances of the GAP sale may exacerbate some of the things it believes can affect consumer behaviour.

Author:

Tom Seymour

Freelance writer

Freelance writer for AM, Tom Seymour has been a specialist B2B journalist covering the automotive sector for over 14 years. He started his freelance career in 2015 and currently writes for a variety of automotive, business and technology publications.

Login to comment

Comments

No comments have been made yet.