By Jay Nagley

It probably won’t come as a surprise to most people that mainstream manufacturers are more dependent on small cars than they were 10 years ago. With the rise of premium brands, the scope for selling large cars without a premium badge has shrivelled to nothing so, logically, small cars must take a bigger share of “volume” manufacturers’ output.

|

||

Jay Nagley was a market analyst at Porsche Cars GB before spending the past 13 years as the head of Redspy Automotive, his own analysis and forecasting consultancy. |

||

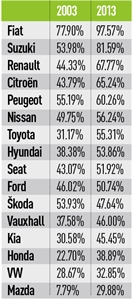

Nevertheless, the speed of the shift has been startling (see table, right). Some manufacturers have seen their dependence on small cars (defined as city cars and superminis) rise by more than 20 percentage points.

At the furthest extreme, Fiat effectively sells nothing but small cars, but there are other manufacturers that appear to be on the same trajectory.

Suzuki, having lost most of its presence in 4x4s, is now basically a small hatchback specialist (although it is going to try to reconquer the 4x4 market), while Renault is not far behind.

Ten years ago, Renault sold a lot of Lagunas and still had aspirations to compete in the executive segment with the Vel Satis – a name that perfectly captured the product’s empty pretensions. By 2013, two-thirds of sales came from small cars, and initial figures for 2014 suggest Renault is heading for a Suzuki-like figure this year.

Selling small cars only is a precarious position to be in

It should be said that making more small cars is not automatically a bad thing. Fiat’s alternative to selling lots of 500s is not selling lots of Bravos – it is extinction.

Similarly, Citroën is a lot healthier selling lots of DS3s at a good margin than giving away thousands of Xsara Picassos at VAT-free prices.

However, only a finite number of people want a designer small car. Thankfully, that number is big enough to keep a few car companies going, but it is a precarious position to be in. These are giant industrial enterprises basically dependent on one or two models staying in fashion. Ever since GM invented market segmentation in the 1920s, the goal has been to have a range of models appealing to different types of buyers.

It is no coincidence that Europe’s most successful car company, VW, not only has one of the lowest proportions of small cars, it also has one of the most stable figures. It sells more Ups than it used to sell Lupos, but it also sells more of everything else. VW also controls the only major brand that has reduced its proportion of small cars over the past 10 years: Škoda’s share is down to under 50%, mostly thanks to the success of the Yeti.

Some companies may find it impossible to get back into medium-sized cars

|

|

| Small car proportions by manufacturer |

The big danger for non-premium car companies is that they retreat to the small car market, but find it impossible to get back into medium-sized cars. Fiat has publicly admitted it has given up on C-segment hatchbacks and it may not be the last.

In the short-term, lifestyle small cars, such as the Nissan Juke, can do excellent business with good margins, but everyone is piling into that particular market. In five years, margins on small crossovers may be little better than B-segment hatchbacks, in which case crossovers no longer look like much of an escape route. Of course, that is less of a problem for Nissan, which also has the bigger Qashqai, but a manufacturer dependent only on the B-segment would then be in trouble. Premium small cars, such as the DS3, also have finite possibilities, because they have to be premium in comparison to something else: by definition, not every small hatch can be premium.

The car industry is far too complex to summarised in a single number, but dependence on small cars is definitely a warning signal. There are exceptions: Suzuki is a global small car specialist that seems able to make better money out of basic cars than almost anyone else: until the start of 2014, it was selling its entry-level Maruti 800 hatchback in India for just £2,500 (the reason why a Tata Nano does not look like such a bargain to Indian buyers).

However, for manufacturers who have no fundamental advantage in small car design, it has to be a

Login to comment

Comments

No comments have been made yet.