The next couple of years is a crucial period for Lookers as it considers further acquisitions, prepares for a roll-out of a new website and looks to achieve an individual sale and service for each of its customers, while at the same time contemplating a much-changed retail landscape in the UK, acknowledging the radical changes in customer expectations. AM editor Jeremy Bennett speaks to chief executive Andy Bruce and managing director Nigel McMinn.

Jeremy Bennett: At what figure will the new car market end 2014?

Andy Bruce: The forecast is 2.45 million units, but it feels like it’ll be a little more than that. It would be good if it reached 2.5m, in a symbolic sign of success. There are a lot of harbingers of doom, saying it’s topped out, or that pre-registration activity is forcing the market or in some way the positivity isn’t real. But we think the market has got more growth in it.

The next couple of years is a crucial period for Lookers as it considers further acquisitions, prepares for a roll-out of a new website and looks to achieve an individual sale and service for each of its customers, while at the same time contemplating a much-changed retail landscape in the UK, acknowledging the radical changes in customer expectations. AM editor Jeremy Bennett speaks to chief executive Andy Bruce and managing director Nigel McMinn.

Jeremy Bennett: At what figure will the new car market end 2014?

Andy Bruce: The forecast is 2.45 million units, but it feels like it’ll be a little more than that. It would be good if it reached 2.5m, in a symbolic sign of success. There are a lot of harbingers of doom, saying it’s topped out, or that pre-registration activity is forcing the market or in some way the positivity isn’t real. But we think the market has got more growth in it.

FACTFILE |

|||

|

Organic growth and acquisitions have seen Lookers grow from selling bicycles at the start of the 20th century to one of the most successful plcs and largest dealer groups in the AM100. It has about 5,500 staff across more than 30 manufacturer franchises at more than 120 sites, as well as a leasing and parts wholesaling and distribution businesses. Financial performance is a strong point: as well as being in the AM100 top five by turnover, Lookers is third in profit before tax (£46 million in 2013), 14th in PBT per franchise (£419,000) and 13th for return on capital employed (18.7%). Return on sale is also at a high of 1.9% in 2013. Analysts conservatively estimate 2014 profits will be £61.5m following a statement from the group in October that it achieved record results in Q3 2014. Lookers’ £33.6m purchase of Colborne Garages in March 2014 was one of the year’s largest acquisitions. |

|||

If you accept that the average annual market in a normal environment is about 2.4m, there were about 2.5m cars not sold between 2008 and 2013. Provided the economic conditions are right, this pent-up demand should be released over time. So our working assumption is that provided there aren’t any economic shocks or anything unforeseen, the market will go beyond 2.4m, to 2.5m and even to 2.6m next year. It could go slightly beyond that, as the pent-up demand gets released.

JB: Andy, you’ve said previously your strategy is to operate a diverse business, a wide range of manufacturer partners across a wide geographical area, both of which help to reduce exposure anomalies or fluctuations in demand. But a diverse franchise portfolio means you’re quite exposed during the weak points in the product cycle for any manufacturer.

AB: It’s largely true. The broad geographical coverage is helpful. There are peaks and troughs in regional economies that are evened out by wide geographical presence.

In terms of brands, you will have seen an absolutely deliberate attempt to enrich the mix of premium brands and we have reduced our exposure to the French brands. We had 13 standalone Renault businesses and now we have six.

We don’t want to represent every single brand to the absolute maximum. We’re moving towards reducing low-volume, small-market-share brands.

JB: Looking at your acquisition strategy, you don’t appear to be buying underperforming businesses to turn them around.

AB: It depends what you’re trying to turn around. Our acquisition of Lomond was a good example of a business that by any financial measure was underperforming, but it had the potential to be really profitable.

However, we get offered a lot of businesses that are in secondary markets with relatively low market share franchises. So, if somebody came along and offered us Citroën in a smallish town like Morecambe or Lancaster, the turnover of that business is always going to be low and it wouldn’t appeal to us, unless it was allied to a larger market area.

JB: How centralised is the business operationally? You have a national business with scale, but do you endeavour to have regional focus to ensure you understand and exploit local markets effectively?

AB: We try to create the best of both worlds. Our aggregated turnover this year is going to be about £3 billion, so we’re in a strong position in terms of our buying power for energy, for finance, etc. and we take our scale and use it to buy well. But we run the business on a highly devolved basis in divisions.

We don’t have a homogenised, one-size-fits-all approach. We can’t forget the fact that we work in a franchised model. So, Mercedes-Benz has a way of doing things, which may be different to how Vauxhall does it. For us to try and overlay a Lookers’ approach would conflict with manufacturer culture, which is always going to dominate. We reflect what the manufacturer does. Head office is the bank.

JB: You’ve improved profits, paid off debt (Read 'Why is Lookers reducing its debt?'), made some strategic moves, got some good people on board, but what is the purpose of Lookers?

AB: The purpose of business is to make money and, in our case, deliver shareholder value. The more philosophical line is that we’re here to create employment and purpose and structure in people’s lives, to give them something to strive for.

[page-break]

JB: Are you confident all your staff understand the purpose and can deliver the results required by it?

NM: We’re not the sort of company that tries to write very tight, detailed job descriptions for every role. We keep it more generic than that and flexibility is a key characteristic of what we’re looking for. We have defined values, we have a programme internally to address customers for life and we package our purpose a little more around the customers, not just the shareholders, to ensure we provide a fantastic experience for the customers. The result of this should be driving shareholder value.

JB: Have you got acquisitions in the pipeline?

AB: Nothing is at a stage I can talk about. But if you look at the acquisitions we’ve made in the past two or three years, they should inform people’s expectation of what we’ll do in the future. So, premium brands in affluent, large conurbations. But we will hit some natural buffers in perhaps five years or more in how we can grow.

JB: You said recently that leads generated by your website have gone up 12% this year. Some of these are down to a strong new car market, but how are you ensuring your online business is as strong as it can be?

NM: The first thing we’ve got is a very strong web platform provider in GForces. Our site is on a very robust platform that can handle masses of traffic. Part of the reason that we’ve outperformed the market this year is that we’ve released, as the year’s gone on, more functionality.

There’s a more common standard in the group now. We didn’t dictate what was needed. We’ve talked about it as a team and decided there should be a best practice, so we removed certain barriers, such as development budgets, that have prevented that from happening and pushed through with functionality improvements so things like independent reviews, finance calculators and part-exchange evaluations were introduced as standard across the divisions.

Lookers is also moving this month to an upgraded platform, which is responsive, plus it has features such as Reevoo customer reviews, What Car? car reviews, 360-degree, gyroscopic views of car interiors and new and used car videos.

Most importantly for brand-hopping consumers, you’re not made to search by brand, but can define a search by a number of different criteria, for example, ‘all diesel SUVs that can do 50mpg and will cost me less than £500 per month’.

JB: What will this change deliver performance-wise?

NM: It will improve conversion rates. Our site has about half-a-million unique visitors a month. Users are likely to stay on it for longer and enquire in some way.

JB: Do you know what the visit-to-enquiry ratio is?

NM: No, but it’s strong. What’s crucial is what we do with an enquiry. This year, every division has got a business development centre, a team who do nothing but answer inbound enquiries, whether they come through live chat or email or by phone.

[page-break]

JB: Sooner or later, an individual will come into a showroom and meet a salesperson. How do you ensure the customer does not have to repeat what they told the business development centre, but the conversation continues?

NM: The conversion rate is measured from enquiry toappointment in the branch and then sale. So we’re able to compare the conversion rates by dealership and see whether the centre is allocating the appointments to people who ensure it’s a joined-up process.

All of the customers are receiving surveys from us whether they buy or not, so if they say “it was great until you handed me through to the sales exec in the branch, because they didn’t seem to know anything about me”, we get the feedback.

Between the surveys and the conversion rates, we have a good idea whether enquiries are being handled correctly in the branches.

The website will also help boost our organic search ratings because Google’s algorithms are much more based now around the organic functionality on the website. If that is good and if there’s good strong links to social media then you’re likely to get good organic search results.

JB: How do you ensure your IT function, not just your website, is working right, that you don’t have different databases across businesses, particularly acquired businesses, that lead to inefficiency, repetition or communication drop-outs?

AB: Our goal is to allow the customer to type their data in once and then, wherever or however they engage with us, we know who they are, what they’ve looked at and what they’ve spent so far with Lookers.

Achieving this is one of the biggest strategic challenges that the industry faces.

IT is now at the centre of every retail business, and not just car retailing. We’ve appointed somebody who designed Carphone Warehouse’s retail systems as business transformation director and it’s his job to make sure this goal is achieved.

We’re looking at this as a three-year project, but his intention is that we will see elements of this development – the quick wins – being delivered in the next 12 months.

JB: Is it possible for you to tailor your offering to every customer individually, from establishing the car they need from their driving style (e.g. being heavy on the brakes), annual mileage and lifestyle and then an aftersales package based on a bespoke contact plan rather than a rigid service plan?

NM: It’s not possible now, but it’s where it’s heading. The database we want to create will be built around one very comprehensive, very sophisticated, unique record for each customer. It will record a history of contacts, transactions and vehicle history that includes everything. The solutions we’re looking at also gather information from social media about each customer.

[page-break]

JB: How long will it be before you can say you have a contact plan for each individual customer?

NM: I don’t know the answer to that. We haven’t actually got the data and it’s not collected in a useable format, but we’ll be able to do that within three years.

Then we’ll ask how we can use the data much more intelligently to make the communication and the products and services that we offer bespoke.

Customers expect it; they are frustrated they have bought four cars from us, that they’ve been on the website and filled in some finance quotations, they might have even made an enquiry, spoken to us two or three times and then they walk into the showroom and somebody still says “how can I help you today?”.

The by-product of a joined-up database will be we’re able to talk to customers in a much more intelligent way about stuff they’ll be interested in and that will be conducive towards them continuing to buy from us.

JB: Accepting that consumers are visiting fewer showrooms to shop for their next car, have you changed the way your sales staff approach customers?

NM: It’s changing and we’re in the middle of the transition. The typical sales exec is changing from the old school, big hitter that used a lot of sharp phrases and words and is clever and flamboyant to somebody who’s new to the industry that is enthusiastic, responsive, happy to build technical expertise in the products and just wants to help the customer.

JB: What is it about John Lewis that fascinates the retail motor trade as a role model?

AB: It has convinced everybody that they are the role models for customer service. Whether that’s just through sheer weight of its repeating it or it’s actually founded in fact, it’s hard to know. It’s probably a bit of both.

We got Andrew McMillan (John Lewis’s former head of customer service and a former AM columnist) to facilitate the design of our customer engagement programme and it’s largely reinventing some of what is common sense.

A team of about eight people came together, including myself, and others of the right mindset.

We started out believing that the key to improving customer satisfaction would be to dream up cleverer ways of processing people in the business, so we need to be smarter and think up a new way of getting somebody to book a service. But it became clear that it’s actually a lot less about process and a lot more about the human touch.

Our behaviour is, in turn, influenced by how happy the staff are to work here.

A great deal of our ‘customers for life’ strategy is based on how do we have the happiest, most engaged, committed work force, in the knowledge that it will reflect itself in the customer experience.

[page-break]

JB: How does this goal manifest itself in the business?

NM: It manifests itself in the business in two key ways. We have a ‘NICER’ league which is a balanced score card of customer metrics. They’re the five broad behaviours that we’re looking for: be nice, interested, caring, enthusiastic and responsive.

Secondly, if you’ve got managers who look after their people and genuinely listen to them, encourage them, are genuinely pleased when they do something right and it’s a positive culture that overrides everything, the staff are happy coming to work. They know where they fit in, feel valued and appreciated and that they contribute in some way.

JB: Can the pay model of low basic, high commission be broken? And could you do it unilaterally at Lookers?

AB: It’s going to happen. The whole purpose of the NICER programme and what we’re doing with IT and the web and our branches – the blended retailing – reflects there’s been a transfer of power from us to the customers. The whole sales process in the past was predicated upon the fact that I know lots of things, you don’t know anything and based on psychologically controlling customers and you therefore needed staff that were good at that.

Now people say: “I don’t want any of your psychological rubbish. I know this car needs to be £500 cheaper if I’m going to buy it. So, I just need you to help me to buy this car and I don’t want you to sell me anything, just explain the price differences between makes or models.”

This will lead to a different pay model because all it requires of sales staff is to be a decent, helpful person. You don’t need to have all these psychological control skills, the doggedness. As long as you answer their questions and you’re polite, a customer will buy from you.

JB: What will be a fair basic salary in the new model?

AB: I don’t know. I’d need to scientifically study the market, to find out what good quality, retail sales people outside this sector earn? It could be £20,000. But we would look outside our industry for inspiration.

NM: The days of having two or three big hitters that earn £70,000 are passing. The vast majority of recruits we bring in to the business now are new to the industry and don’t have that expectation that they’re going to earn £70,000 and in truth don’t have the same skills as the guy that earned £70,000, but the skills required today are different. There would be a transition phase in the pay model.

But some of the people that earn £70,000 are very hard working and customer focused, so we’d have to make the pay scheme flexible enough that they can still earn a lot by working hard. Those that want to work six and seven days a week can really do a job that impacts the performance of the business, and you need to reward that. Whatever the number is we’ll pay, but it’ll be more like three quarters of it as basic and a quarter of it based on performance.

[page-break]

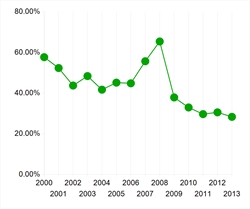

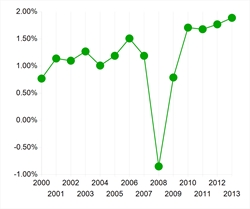

WHY IS LOOKERS REDUCING ITS DEBT?

| LOOKERS' GEARING (%) | LOOOKERS' RoS (%) |

|

|

| Source: www.am-online.com/ami |

Car retailing is intrinsically cash-positive, even done relatively poorly. For example, if Lookers had made a loss (of say £1) last year, they would still have made £30 million when items that do not consume cash, such as depreciation and amortisation, are added back.

Lookers’ profit before tax for 2013 was £44m. Add back depreciation and amortisation and the cash profit (EBITDA – earnings before interest, tax, depreciation and amortisation) is £75m. This offers the group choices:

♦ return money to shareholders

♦ buy more businesses

♦ invest in new profit streams

♦ repay debt.

Dividend yield is 2.17, which is better than Pendragon, but the FTSE100 best 50 show a yield ranging from 3% to 14%.

Colborne Garages was purchased in 2014, but that transaction still leaves substantial cash resources.

Lookers has successfully diversified into parts wholesaling. However, there do not appear to be any further plans to invest in new areas.

So this appears to have left debt reduction as the remaining opportunity. Gearing, from a comparatively modest high of 65% at the height of the recession, has reduced to 28%.

Since 2008, Lookers has been steadily improving the business, so if this trend can be maintained, the problem of what to do with the cash will become more acute.

Lookers’ chief executive Andy Bruce acknowledged that a balancing act was required: “We have increased the dividend by more than 40% in the last three/four years and we’ve signalled generally to the market to expect a 10% progressive increase.

“We’re growing the profits a lot faster than 10% and therefore the yield is weakening all the time. But, of course, these dividends cost money.

“And in the last three years we’ve invested £55m in acquiring businesses. This year they will make £17m – a 31% return – and if our share price in the fullness of time tracks that type of return then it will dwarf any improvement in dividend, even if it went to 4%.”

He said the group considers total shareholder return, an element of which is dividend yield, but demanding greater attention is the question of what to do with cash.

“We don’t want to gear the balance sheet to the level it used to be,” Bruce said. “ We all learned that painful lesson when the banks were throwing money at us. So, we’ve got relatively conservative gearing. We measure it on a debt-to-EBITDA ratio, so it’s about 0.5:1.0 at the moment.

“We would let that float up a bit beyond 1.0 before an acquisition. But of course the bigger the company is getting, the EBITDA gets bigger. We bought Colborne for about £30m in cash in March and we ended up at the half-year with the same debt as we did at the start of the year, such is the amount of cash we’re generating.” The group will be acquiring again, he said.

Login to continue reading

Or register with AM-online to keep up to date with the latest UK automotive retail industry news and insight.

Jeremy has been a journalist for 30 years, 20 of which have been in business-to-business automotive.

He was a writer and news editor on AM-sister brand Fleet News for three years before setting up the AM website.

For the last seven years he has been Bauer B2B’s head of digital helping to manage the digital assets of Fleet News, together with AM and RAIL.

In 2025 he was an Association of Online Publishers awards judge.

Login to comment

Comments

No comments have been made yet.