Pawnbrokers are the only lending provider deemed worse than motor finance at assessing customer vulnerability as UK households feel the impact of the cost-of-living crisis, an FCA report suggests.

Findings from the Financial Conduct Authority’s (FCA) ‘Borrowers in Financial Difficulty following the Coronavirus pandemic’ report revealed that motor finance was falling short of the standards achieved by market segments including ‘high-cost short term loans’ and ‘home collected credit’.

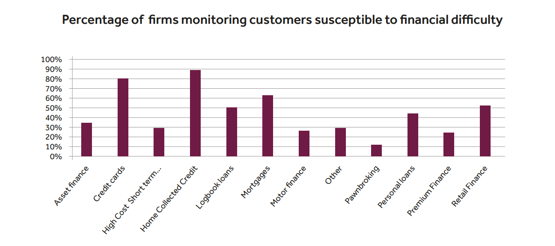

Just over a quarter of motor finance providers were found to be “monitoring customers susceptible to financial difficulty”, the FCA’s report found.

The findings come after the deadline passed for motor finance providers to tell the FCA about the measures they are taking to meet its new Consumer Duty, which is shifting its expectations of from the old "treating customers fairly" principle to now an adage of "put their customers' needs first".

The findings come after the deadline passed for motor finance providers to tell the FCA about the measures they are taking to meet its new Consumer Duty, which is shifting its expectations of from the old "treating customers fairly" principle to now an adage of "put their customers' needs first".

It also comes after AM reported on research which highlighted that finance debt for new and used cars had risen to £40 billion per year in the UK – prompting concerns that consumers may default on agreements amid soaring living costs.

The FCA said: “As pressure on household finances continues, the FCA expects more customers will need support from their lenders.

“The FCA’s recent Financial Lives survey of 19,000 people shows that more expect to struggle in the months ahead.

“Nearly eight million people are finding paying for the basics a heavy burden which is two and a half million more than in 2020.”

In total the FCA’s latest report found that just 30% of firms (15 out of 50) it reviewed sufficiently explored customer’s specific circumstances, which meant repayment agreements were often unaffordable and unsustainable.

The FCA said that it had already told 32 firms to make changes to improve the way they treat customers and so far, seven of these firms have voluntarily agreed to pay £12 million in compensation to nearly 60,000 customers.

Sheldon Mills, executive director of consumers and competition at the FCA, said: “While many firms did well in supporting customers in difficulties during the pandemic, with our support and guidance, others sadly failed their customers.

Sheldon Mills, executive director of consumers and competition at the FCA, said: “While many firms did well in supporting customers in difficulties during the pandemic, with our support and guidance, others sadly failed their customers.

“Given the current cost of living challenges, it’s vital that the sector continues to learn lessons to make sure they support struggling customers.

“We will take action to restrict or stop firms from lending to people if they fail to meet our requirements that consumers in financial difficulties should be treated fairly.”

The FCA said it expects lenders to learn the lessons from good and poor practice during the COVID-19 pandemic to help borrowers during the cost-of-living squeeze.

It asserted that firms should be:

- Encouraging consumers to engage earlier when facing financial difficulties.

- Offering tailored support, particularly for those with vulnerable characteristics.

- Letting those in difficulties know about the availability of free, independent debt advice when appropriate.

- Making sure their fees and charges are fair and only reflect the reasonable costs that firms incur.

- Considering, when engaging with consumers, whether it would be appropriate to reduce, waive or cancel fees and charges.

To read the FCA's full ‘Borrowers in Financial Difficulty following the Coronavirus pandemic’ report, click here.

Login to comment

Comments

No comments have been made yet.