By Rupert Pontin

Much has been made in recent months of the very strong levels of new car registrations in the UK market, but views differ on how this exceptional run of success is being sustained.

SMMT data confirmed that March 2015 was the 37th consecutive month of improved registrations and the best in new registration terms since the two-plate system was introduced in 1999. Year-to-date registrations are up 6.9% on 2014.

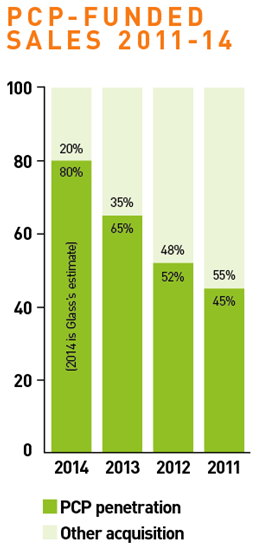

Whether these registrations are all genuine sales is doubtful, but what is clear is that the UK economy and subsequent consumer confidence is encouraging manufacturers to push product into the UK market. PCPs are the key facilitator to move these cars to the private buyer so effectively. The chart below depicts just how great the phenomenon has become, by showing how the percentage of sales funded by PCP has increased in the past four years.

This is good in many ways. It ensures European over-production is dealt with in a constructive way without further damaging the European position, dealers are given the opportunity to make more money and, of course, the general public have the enjoyment of a new car.

This is good in many ways. It ensures European over-production is dealt with in a constructive way without further damaging the European position, dealers are given the opportunity to make more money and, of course, the general public have the enjoyment of a new car.

It is also evident that to cope with the level of production due to come to the UK, manufacturers and finance companies will be pushing dealers to bring PCP change cycles forward from those originally agreed. On the face of it, this is again good news for all.

However, it does begin to bring a different dynamic to the used market, which will need to be prepared to absorb greater volumes of newer cars in a way it had not expected.

There are two ways the new car volume position can be tempered. Firstly, manufacturers could look at reducing the volume of cars produced and where those cars are scheduled to be sold. However appealing and easy this solution appears, the reality is that production cannot just be turned off at short notice.

The second way is for the European markets to improve significantly to take the volume originally planned for them. This is also unlikely. Glass’s economic data partner, Oxford Economics, highlights areas of optimism and growth, but nothing that will result in alleviating the volume heading for the UK domestic market this year.

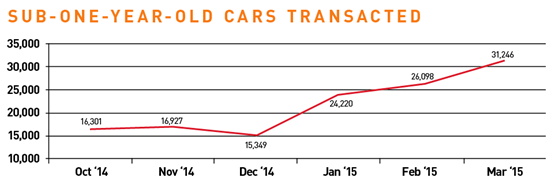

In recent months, we have seen the tactical activity required to deliver the reported registration levels result in a notable increase of sub-one-year-old cars to the market. Using data from Glass’s Radar product, the table, left, clearly shows the increased level of what are likely to be pre-registered cars in the used market.

It is clear from the chart below that between October 2014 and March 2015 the volume of sub-one-year-old vehicles sold increased by more than 91%. While these are not all pre- registered vehicles, this shows a significant change in the shape of the market and what must be considered is the pressure this has put on used values. Equally, the impact of continually using this type of route to market must be assessed over the course of the coming months as there will only be a finite number of customers willing to purchase at this level and therefore other strategies will need to be developed to keep sales moving.

There is little doubt that by the end of 2015 new car sales volumes will have increased on the 2014 figure of 2,476,435. Glass’s believes the market will support 2.6 million new registrations, an increase of 5%. This will consist of an increase in the private sales sector, but it will also be due to expanding contract hire and leasing sales that are now increasing month on month as a direct result of the improved economy and the pent-up demand caused by retaining cars on fleets for extended periods during the recession.

There has long been speculation over when this position would right itself. The market is finally beginning to see the start of continuous volume increases and this naturally translates into greater defleet of used vehicles hitting the market. Until this point, there has been a lack of the varied product now being released by the fleet owners and this provides a greater level of choice for both the trade and retail buyer.

It is not hard to see this will translate into a buyers’ market in time, something that has not been seen for some years. The real concern is that the gentle volume increase experienced in the past six months will ramp up significantly in a very short period of time. The trade appears to be preparing for this onslaught after the September plate change.

Many contract hire and leasing companies have candidly expressed concern at what may happen at this point, with specific disquiet expressed over the state of the late-plate market and the downward pressure these cars will have on their 36- to 48-month-old defleets. Until this point, these three- and four-year deals had looked fairly sound based on the fact that transactions made founded on high residual value expectations would be fine when placed into a market short of ex-contract hire and leasing product.

Login to comment

Comments

No comments have been made yet.