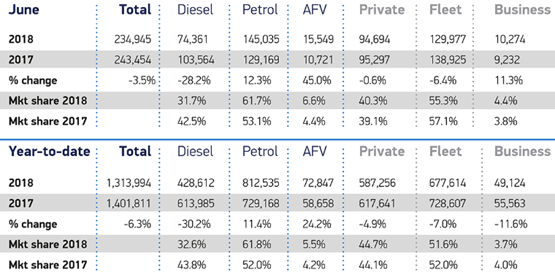

New car registrations fell by 3.5% in June to 234,945 units and the market is down by 6.3% for the first half of this year, according to the latest figures from the Society of Motor Manufacturers and Traders (SMMT).

Private registrations were flat in June, down 0.6%, while large fleets led the biggest decline with a 6.4% drop. SME business helped to offset the declines with an 11.3% uplift.

The SMMT said the market is continuing to stabilise following a turbulent first half of the year distorted by the previous year’s VED hikes, with the market experiencing a severe double-digit decline in March followed by a stronger April and May, when year on year demand grew.

Smaller cars remained most popular, with supermini and lower medium vehicles taking a combined 57.4% market share.

However, dual purpose (crossovers/SUVs) was the fastest growing segment, with demand up by some 16.4% - 6,710 more than in the same month last year. Premium crossover and SUVs (+4.3%) and luxury saloon (+1.3%) were the only segments to register growth in June.

The alternatively fuelled vehicle sector saw a 45% increase in plug-in and hybrid registrations as consumers responded to a growing range of models.

The alternatively fuelled vehicle sector saw a 45% increase in plug-in and hybrid registrations as consumers responded to a growing range of models.

Petrol cars also attracted more buyers, with demand up 12.3%. However, this growth was not enough to offset continuing decline in diesel registrations, with a -28.2% fall a result of continuing consumer uncertainty over future policy towards this technology.

Mike Hawes, SMMT chief executive, said: “Despite a rocky first six months for the new car market, it’s great to see demand for alternatively fuelled vehicles continue to rise.

“Given these cars still represent only one in 20 registrations, however, they cannot yet have the impact in driving down overall emissions that conventional vehicles, including diesels, continue to deliver.

“Recent government statements acknowledging the importance of petrol and diesel are encouraging. However, we now need a strategy that supports industry investment into next generation technologies and puts motorists back in the driving seat, encouraged to buy the car that best suits their needs – whatever its fuel type.”

Best sellers year-to-date

- Ford Fiesta 56,415

- Volkswagen Golf 39,930

- Ford Focus 30,757

- Nissan Qashqai 30,066

- Vauxhall Corsa 28,003

- Mini Hatch 23,641

- Volkswagen Polo 22,027

- Ford Kuga 21,784

- Mercedes-Benz A Class 20,002

- Mercedes-Benz C-Class 19,684

SMMT new car registrations data June 2018

| JUNE 2018 | % Market share | % Change | |||

|---|---|---|---|---|---|

| MARQUE | 2018 | % Market share | 2017 | ||

| Abarth | 542 | 0.23 | 438 | 0.18 | 23.74 |

| Alfa Romeo | 420 | 0.18 | 448 | 0.18 | -6.25 |

| Aston Martin | 118 | 0.05 | 112 | 0.05 | 5.36 |

| Audi | 14,526 | 6.18 | 15,081 | 6.19 | -3.68 |

| Bentley | 229 | 0.1 | 168 | 0.07 | 36.31 |

| BMW | 22,985 | 9.78 | 19,149 | 7.87 | 20.03 |

| Chevrolet | 2 | 0 | 7 | 0 | -71.43 |

| Citroen | 5,144 | 2.19 | 4,685 | 1.92 | 9.8 |

| Dacia | 2,000 | 0.85 | 2,845 | 1.17 | -29.7 |

| DS | 712 | 0.3 | 872 | 0.36 | -18.35 |

| Fiat | 3,613 | 1.54 | 5,062 | 2.08 | -28.63 |

| Ford | 22,334 | 9.51 | 27,095 | 11.13 | -17.57 |

| Honda | 4,606 | 1.96 | 5,043 | 2.07 | -8.67 |

| Hyundai | 8,663 | 3.69 | 7,965 | 3.27 | 8.76 |

| Infiniti | 97 | 0.04 | 383 | 0.16 | -74.67 |

| Jaguar | 2,960 | 1.26 | 2,960 | 1.22 | 0 |

| Jeep | 644 | 0.27 | 363 | 0.15 | 77.41 |

| Kia | 9,162 | 3.9 | 7,972 | 3.27 | 14.93 |

| Land Rover | 6,024 | 2.56 | 6,201 | 2.55 | -2.85 |

| Lexus | 1,306 | 0.56 | 1,161 | 0.48 | 12.49 |

| Lotus | 20 | 0.01 | 46 | 0.02 | -56.52 |

| Maserati | 108 | 0.05 | 107 | 0.04 | 0.93 |

| Mazda | 3,628 | 1.54 | 3,255 | 1.34 | 11.46 |

| McLaren | 37 | 0.02 | 56 | 0.02 | -33.93 |

| Mercedes-Benz | 14,928 | 6.35 | 15,715 | 6.46 | -5.01 |

| MG | 871 | 0.37 | 314 | 0.13 | 177.39 |

| MINI | 8,176 | 3.48 | 9,015 | 3.7 | -9.31 |

| Mitsubishi | 1,545 | 0.66 | 1,361 | 0.56 | 13.52 |

| Nissan | 8,640 | 3.68 | 13,067 | 5.37 | -33.88 |

| Peugeot | 7,786 | 3.31 | 7,688 | 3.16 | 1.27 |

| Porsche | 1,163 | 0.5 | 1,302 | 0.53 | -10.68 |

| Renault | 5,606 | 2.39 | 7,316 | 3.01 | -23.37 |

| SEAT | 6,517 | 2.77 | 4,901 | 2.01 | 32.97 |

| Skoda | 8,233 | 3.5 | 7,512 | 3.09 | 9.6 |

| smart | 633 | 0.27 | 881 | 0.36 | -28.15 |

| Ssangyong | 359 | 0.15 | 362 | 0.15 | -0.83 |

| Subaru | 265 | 0.11 | 202 | 0.08 | 31.19 |

| Suzuki | 3,903 | 1.66 | 3,486 | 1.43 | 11.96 |

| Toyota | 9,697 | 4.13 | 9,556 | 3.93 | 1.48 |

| Vauxhall | 18,218 | 7.75 | 20,981 | 8.62 | -13.17 |

| Volkswagen | 23,224 | 9.88 | 22,639 | 9.3 | 2.58 |

| Volvo | 4,545 | 1.93 | 5,018 | 2.06 | -9.43 |

| Other British | 58 | 0.02 | 65 | 0.03 | -10.77 |

| Other Imports | 698 | 0.3 | 599 | 0.25 | 16.53 |

| Total | 234,945 | 100 | 243,454 | 100 | -3.5 |

MORE: New car sales data

MORE: New car sales per franchised dealership

Industry views

Sue Robinson, NFDA director, said: "The new car market remains relatively buoyant and, to ensure continued stability, it is important that consumers are provided with clear facts and information to enable them to select the car that best suits their needs.

“Summer is usually a quiet period for new car registrations and, this year, thanks to a number of different factors, consumers have a clear opportunity to find very attractive deals on the market."

Richard Jones, Black Horse managing director, said the drop in the market marked further progress towards a sensible, sustainable volume of registrations.

He said: "The ongoing fall in sales of new diesel cars is driven by consumers switching to petrol, which is increasing C02 emissions.

"While we support the shift to electric, this is a very long term transition given the massive shifts needed in infrastructure, vehicle production and consumer adoption attitudes. If we want to impact air quality in a meaningful way in the next five years, we need to get people out of using older cars and into newer ‘Euro 6’ standard vehicles, regardless of fuel type. Consumers need help to understand their choices and remove the mass confusion that exists and we look forward to an effective fuel strategy from UK Government to help with this.”

Sean Kemple, director of sales at Close Brothers Motor Finance, said the market is seeing some hesitance from consumers when it comes to big ticket purchases.

He said: "June saw the SMMT release a harsh warning about the impact of Brexit on both production output and demand to the UK motor industry. Hesitance from consumers if further exacerbated by the uncertainty around diesel, which is having a fierce impact on diesel sale figures.

“The industry is going through a period of change, and dealers need to stay focused in order to protect their bottom lines. It’s crucial to keep a close eye on fluctuating demand, and adjust the stock sitting on the forecourt accordingly."

Ian Plummer, Auto Trader director, said comparisons to 2017 had been difficult due to VED changes last year, so the figures from June are showing more of the underlying market trend.

He said: "It’s still a tough environment with ongoing uncertainty around Brexit and fuel regulation, but with the retail channel roughly flat in the month, it’s clear that strong promotional activity is working to offset this and draw consumers onto forecourts.

“The overall market performance is relatively good, particularly given that the majority of the decline came in the rental channel. This is a high cost, low margin channel which has been made less profitable and less attractive for manufacturers by the unfavourable exchange rate."

Plummer said the forecast for the full year suggests a reasonably strong H2 despite continued uncertainty, but the new emissions testing regime – WLTP or Worldwide Harmonised Light Vehicle Test Procedure – will disrupt typical seasonal sales patterns and could make for a quite unpredictable six months for retailers.

He said: “September is always a strong sales month following the plate change, but this year we are likely to see heavy promotional activity in August to clear non-WLTP tested stock, followed by lower than usual sales in September, and then a bit of catch up played in the Autumn as the new WLTP-ready stock becomes more fully available.”

Author:

Tom Seymour

Freelance writer

Freelance writer for AM, Tom Seymour has been a specialist B2B journalist covering the automotive sector for over 14 years. He started his freelance career in 2015 and currently writes for a variety of automotive, business and technology publications.

Login to comment

Comments

No comments have been made yet.