Cazana’s director of insights, Rupert Pontin, has conceded that February new and used car sales were ‘less promising than expected’ – despite attempts to set the data in a positive context.

In his weekly market analysis, Pontin suggested that general consumer confidence seemed to be under pressure, adding that “the plethora of negative stories in the national press can’t be helping the situation”.

Here he draws on Cazana data to share his observations of the car retail environment in mid-February:

There should be no surprise to anybody in the nation that the economy shrank in 2020, or that retail sales nationwide were lower.

The positivity of the current position seems to be overlooked and given the current lockdown and what happened in the last 12 months the country has shown remarkable resilience, as has the automotive sector and consumers should remember this.

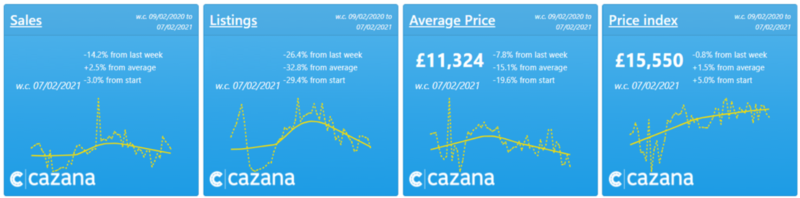

The charts below qualify the market performance over the last week in comparison to the previous week with a full year trendline shown in yellow: Sales levels declined by 14.2% on the previous week and this is symptomatic of the general apathy of the retail consumer.

Sales levels declined by 14.2% on the previous week and this is symptomatic of the general apathy of the retail consumer.

Unfortunately, the resulting dip in sales leads available to convert towards commercial sales targets has been uncomfortable in the last seven days for most retailers.

There has also been a drop in the volume of new retail adverts suggesting that wholesale stock is still proving difficult to find.

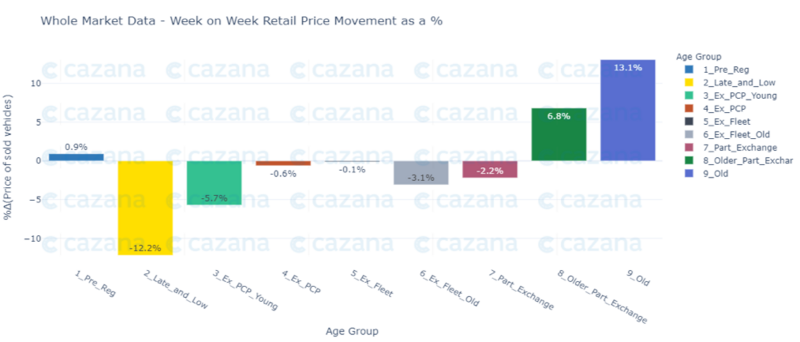

The chart below looks at retail price movements week on week by age profile:

This chart is very interesting as it highlights some significant market pricing shifts and at the same time raises some questions on what is happening in the used car market on a more granular level.

This chart is very interesting as it highlights some significant market pricing shifts and at the same time raises some questions on what is happening in the used car market on a more granular level.

In comparison to the previous week, there are two clear areas of change.

Firstly, the significant drop of 12.2% in the average ‘late and low’ profile retail price, and the jump of 13.1% for the ‘old car’ profile.

Whilst the normalised Cazana Retail Price Index shows a minimal drop of 0.8% the detail is always of critical importance.

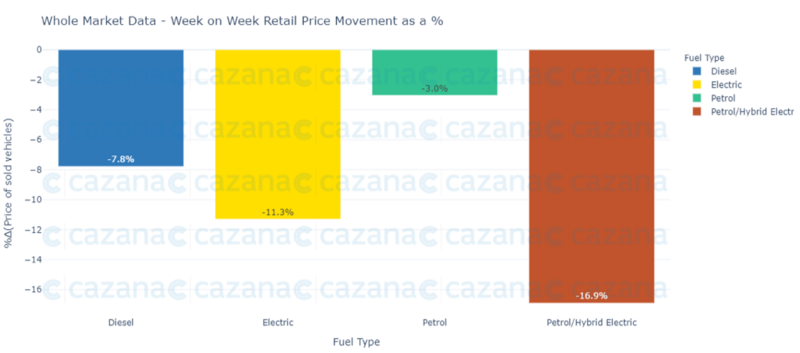

The chart below is a different lens on the market and looks at the weekly retail price movement as a % by fuel type:

A fascinating view that shows that despite the intricacies of the market sector and individual models, all fuel types have shown a dip in average Retail Price on the previous week.

A fascinating view that shows that despite the intricacies of the market sector and individual models, all fuel types have shown a dip in average Retail Price on the previous week.

There has been a marked concern of late as to the hybrid pricing position and this shows that in the last week there has been a large drop of 16.9%.

This is not to say that the position may not significantly improve next week but it is clear that the balance of retail consumer demand on supply is having quite an effect.

Talk of the Road to 2030 and the shift to elelctric vehicles (EV) and hybrids is prevalent at the moment, and a variety of human decision-based forecasts are being punted around the market.

Retail fact-based insight is the only way to have a clear view and eliminate the subjectivity.

To conclude, the second week of February has not been the most encouraging of weeks either for the economy or the automotive sector.

However, the improvement in the weather, the number of people vaccinated in the country and the governments’ plan to bring the country out of lockdown will most likely improve matters.

AM Dealer Technology Guide

The AM 2025 Dealer Technology Guide enables UK motor retailers to read about a host of the latest software and hardware available from the industry's dedicated suppliers.

Keeping abreast of technology is a vital part of modern automotive retailing as the demands of customers and staff for rapid and efficient fulfilment only increases.

Industry suppliers have provided their highlights and summaries for the AM Dealer Technology Guide, and we give their web addresses to help you discover more.

Moreover, many of them will be at Automotive Management Live on November 12 at Birmingham NEC. Ensure you register to join us at our flagship exhibition.

Read now

Login to comment

Comments

No comments have been made yet.