The used car market performed surprisingly well during March despite the best efforts of the continued bad weather to disrupt it.

Conversely, the new car market has struggled and contracted as buyers seem to be tempted towards buying used rather than new cars.

It is worth noting that whilst new car registrations have dropped by 15.7% in March 2018 in comparison to the same month last year, and diesel by 37.2%, March 2017 was a forced market falsified by the need to register cars ahead of the Government’s VED changes.

As such the headlines are not really as bad as they seem and overall the market will balance a little during the course of the year to record a reduction in registrations of around 6.5%.

There are more used car PCP options coming to the market too as finance companies seek to improve finance penetration.

There are a number of innovative online finance and car search sites making finding and buying a used car easier for the retail consumer.

However, quality used stock has been difficult to find and auctions have in the main part been busy and values strong as wholesale buyers strive to fill used car forecourt spaces.

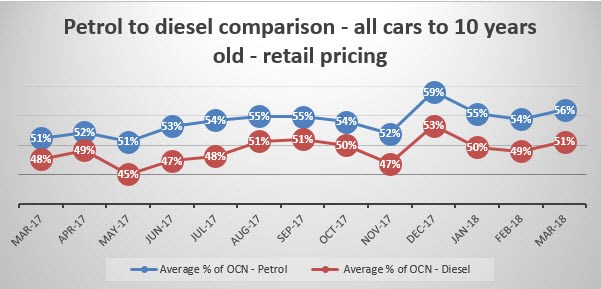

Petrol to diesel market performance

Of continued interest is the diesel discussion fuelled by the national press and driven by the drop in new diesel car sales.

The reduction in new diesel sales seems largely to still be driven by national press speculation and misinformation.

However, the used market is not suffering in the same way and the chart below shows the continued performance of retail driven used car pricing in the UK market over the last 12 months.

This data is a top-level view of Cazana Retail values expressed as a percentage of cost new over the past 12 months.

A year ago, the difference between petrol and diesel retail values expressed as a percentage of original cost new was 3%.

In March 2018 that difference had increased and there is now a 5% difference in values.

Despite the negative feeling towards diesel, this widening of the gap must be considered fair given that the volume of diesel cars coming to the used market has increased off the back of increased registrations in the new market in recent years.

It is also interesting to see that both fuel types have seen in increase in value reflecting the demand from the retail consumer.

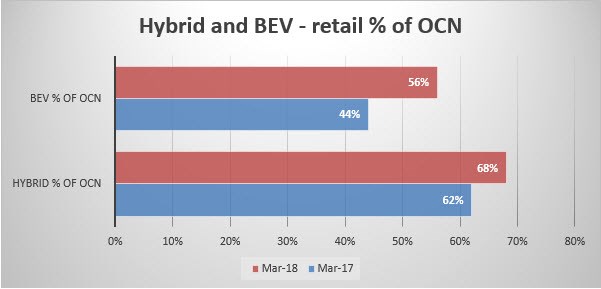

Much has been made of the consequential increase in sales of alternative fuel vehicles as the new diesel market declines, but volumes still remain almost worryingly low.

Whilst this market will continue to improve there is little doubt that at 5.1% new market share, up just 1% on 2017 to year to date, the sector still has a long way to go.

An improved range for BEV’s and the electric side of hybrid vehicles will be the catalyst.

However, the used car market needs to find homes for these cars and at the moment whilst new sales gradually improve, demand for used versions appears to be accelerating a little faster as demonstrated in the chart below.

From March 2017 to the same period this year, retail values as a percentage of cost new for BEV’s have increased by 12%.

Whilst it is possible that some of this can be attributed to the type of car coming to the market it is more conceivable that the increase is down to a better understanding of the cars by both dealers and retail consumers.

In addition, greater driving range in later cars makes them more usable and therefore more desirable to buyers.

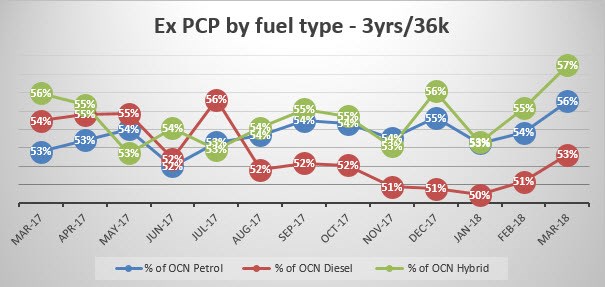

Ex-PCPs in the used market

Last month we looked at the Cazana view of the two-year 24,000 mile ex PCP market and this month the chart below reviews the performance in the retail market of prices for three-year-old 36,000 ex PCP cars.

With volumes continuing to increase there has been much anecdotal evidence suggesting that values have been decreasing rapidly across all fuel types.

However, despite the increase in volume this sector of the market is less clear -cut.

It is interesting to note that over the course of the year retail pricing for petrol and hybrid cars has followed broadly the same pattern. Diesel values have followed a similar pattern to those of the 2-year-old vehicles reviewed last month with a marked dip in values from the early spring 2017 as the discussion about diesel began to gain serious national press traction.

However, year on year diesel values have decreased by just 1 percentage point of original cost new having rallied somewhat since the beginning of 2018. Granted, petrol cars have increased by 3 percentage points and hybrid by one percentage point but it is clear that anecdotal comments suggesting the death of diesel are currently unfounded for used car buyers.

In summary, the last month has seen a positive used car market with consistent retail demand that seems to have driven retail prices and therefore wholesale values upwards. However, the devil is in the detail and greater focus on specific parts of the Cazana database can help drive performance to a greater level and improve sales success.

Author: Rupert Pontin (pictured), director of valuations, Cazana.com

Login to comment

Comments

No comments have been made yet.