- Used car market remains in good health

- Ex-fleet values retain stability despite volume increase

- Ex-fleet petrol values increase year on year

The May new car registration data released on June 5 paints a marginally better picture of the new car market with overall volumes showing an increase of 3.4% over May 2017.

This positive news brings the total year to date volume of cars registered to just over a million vehicles - 6.8% down on 2017.

This is in line with Cazana’s predictions earlier in the year and is the second consecutive month of increase, but must be taken in context with the fact that the May 2017 registrations may have been adversely affected by the general election.

The diesel figures paint another month of poor performance with a drop in volume of 23.6% reflecting the continued concerns over pollution and uncertainty over taxation and government policy.

Year to date diesel registrations are now down by 30.6% and the market share has fallen to 32.8% year to date that is 11.3% lower than at this point in 2017.

Conversely, petrol registrations have improved by 23.5% for the month taking the year to date figure to 11.3% higher than in 2017 and reflecting a 61.9% share of the market.

The improvement in AFV registrations of 36.1% on the same month last year is impressive and the year to date market share sits at 5.3% which is 1.2% higher than at the same point in 2017.

Generally speaking the new car market in May has been boosted by the private buyer with sales to this sector up 10.1% on 2017.

It was sales to the private consumer that were missing in May last year as the country prepared for the general election and this year consumer confidence for the month was stronger and thus reflected in the registration figures.

However, it is worth considering the fact that pre-registration activity has also remained quite high.

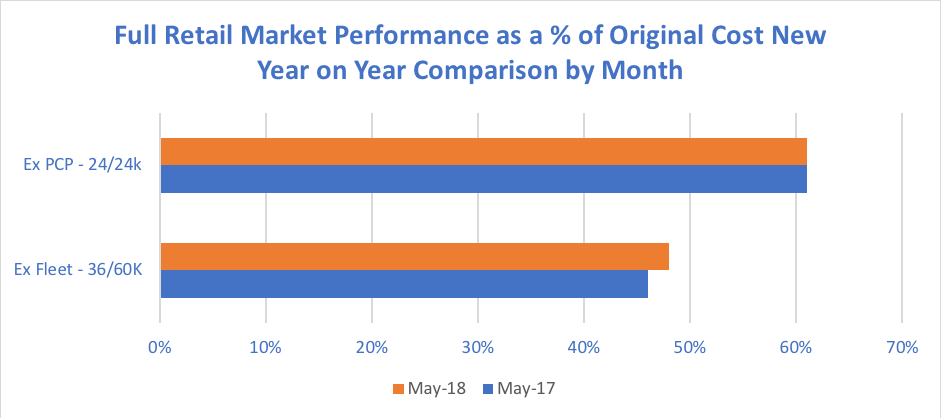

Looking at the used car market the Cazana data shows some interesting nuances, and the chart below shows the performance of two of the key used car market sectors at present.

This chart is based on data taken from the retail market which is the largest volume of relevant pricing and valuation data available to the industry.

This chart demonstrates that the ex-PCP sector has remained consistent in value terms year on year with vehicles retaining 61% of original cost new overall during May 2018.

This is a drop of one percentage point when compared with April 2018 which is very reasonable considering the increased numbers of this age and profile of car returning to the used car market.

The performance of the fleet sector is also good despite also experiencing a similar increase in volume.

May data highlights an uplift in retail values of 2% over the same month last year, and unlike the PCP sector, the May data shows consistency with performance in April 2018 with no decline in values as a percentage of original cost new.

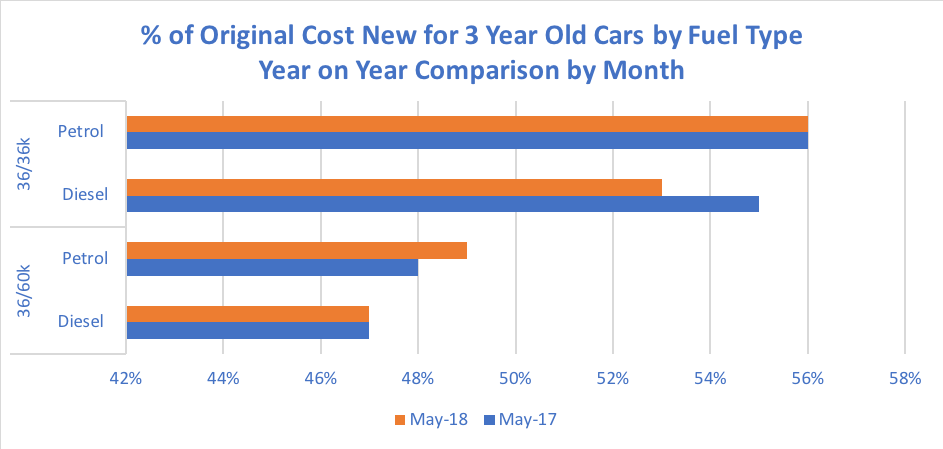

Looking at the petrol to diesel market and despite another monthly decline in new diesel car sales and continued negative press coverage nationwide the used car market continues to show remarkable resilience.

The data collated during May is shown in the chart below.

In comparison to May 2018 there has been stability for ex-PCP and privately-owned cars that have covered 36k mileage.

Pricing has remained at 56% of original cost new mirroring the price point in May 2017 and a 1% uplift on the April 2018 data.

It is interesting to note that diesel pricing has fallen again in May in comparison to last year.

However, at 53% of original cost this shows stability when compared to the April 2018 figure which is positive news.

Looking at higher mileage ex-fleet vehicles there is an uplift in pricing performance of one percentage point for petrol powered cars in comparison to last year although at 49% of original cost new this is some 4% behind the April data.

Conversely, for diesel-powered cars there has been stability from May last year and of note is the fact that prices between April 2018 and May 2018 have increased by one percentage point.

This stability in pricing reinforces the fact that the used car market is still robust with good retail demand.

The increase in volume, however, has seen some vendors in the wholesale environment needing to readjust expectations and auction conversion levels were more variable during the course of the month.

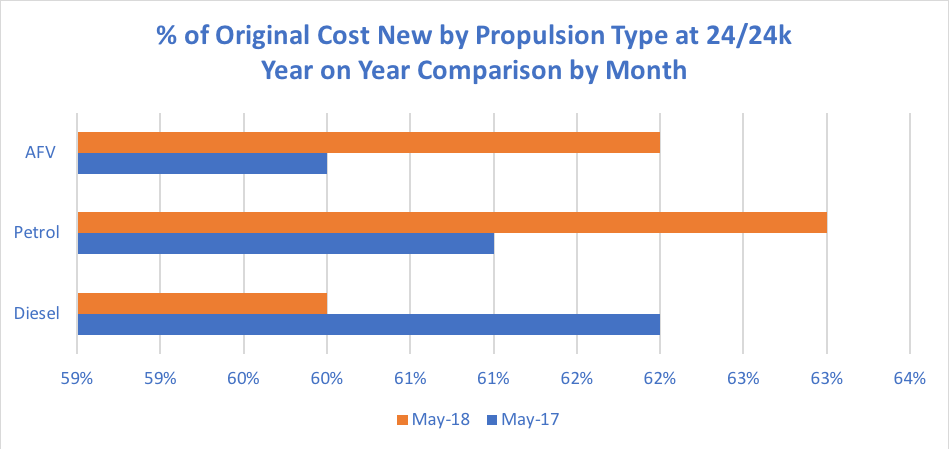

Finally, a view of pricing activity in the PCP sector by fuel type reviewing the performance of alternative fuel vehicles in comparison to traditionally powered cars.

The chart shows that in comparison to May 2017 petrol and AFV retail asking prices have increased as a percentage of original cost new by 2% where diesel has dropped by two percentage points.

This suggests a further erosion of diesel car popularity at this age.

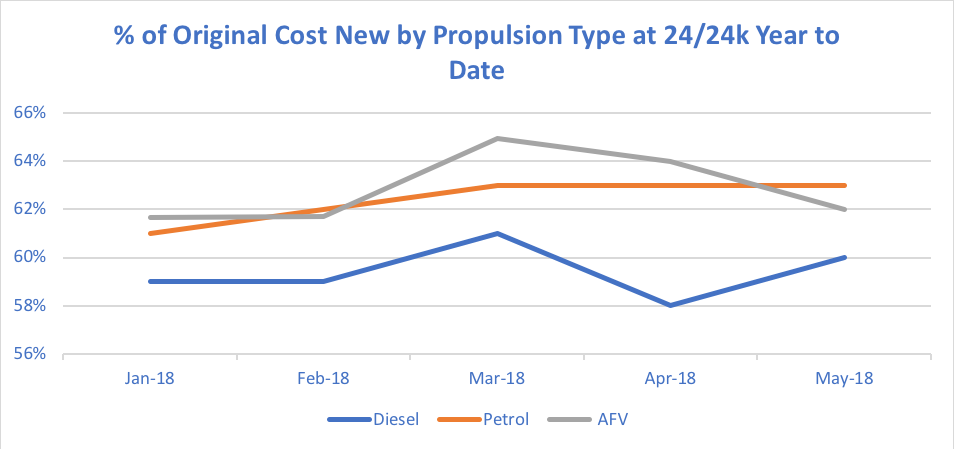

However, it is important to take these year on year changes in context and the final chart depicts retail pricing movements by fuel type since the beginning of 2018.

This chart shows that retail pricing for petrol cars has been the most stable and retail prices have improved by two percentage points year to date.

Diesel pricing has been more volatile although it has increased by one percentage point year to date whilst AFV pricing has also been varied although pricing has remained at the same level thus far.

In previous years retail pricing tends to drop for all propulsion types as the year has progresses, reflecting the natural depreciation of an asset.

As such there is clarity here on the strength of the used car market.

Author: Rupert Pontin (pictured), director of valuations at Cazana. Data powered by Cazana.com

production line")

Login to comment

Comments

No comments have been made yet.