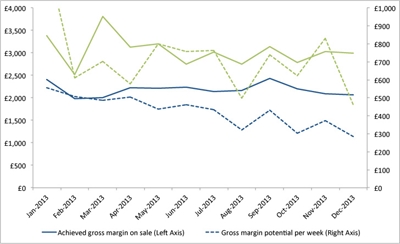

The chart, below, shows the trend in both the actual achieved gross margin and the profit per forecourt space per week for typical B and D segment cars.

|

|

Notably, despite a broadly flat gross margin, the financial return on the B segment car to the dealer appears to have declined by about 40% over the course of 2013, from a rate of over £500 to just under £300 per forecourt space per week for a Ford Fiesta Zetec petrol as a consequence of a steady lengthening in the time needed to secure a buyer for such a car, most likely caused by the plethora of great new car deals for private buyers in that segment.

By contrast and despite greater volatility, a typical D segment vehicle did not show the same level of decline, with a gross margin potential for a Vauxhall Insignia Exclusiv remaining around £600-£700 per week throughout 2013. However, “hidden discounting” through retail PCP deals has been less aggressive in this segment.

It appears that dealers are unaware that the level of profits from certain vehicle segments has been in decline, and many have not adapted.

This really brings into question what a dealer should be stocking; however, it will be necessary to stay ahead of the game as once enough dealers make the connection, prices and selling days will become less attractive as retail supply increases and consumer demand shifts elsewhere.

Without the right data and systems, there is a real chance that the less informed dealer will be left with only the weaker opportunities.

sgcb - 29/05/2014 14:51

THOSE WHO CAN,CAN! THOSE WHO CAN'T TEACH