logo")

The Financial Conduct Authority will set new rules for regulated financial services including motor finance by mid-2022 as it aims to “fundamentally shift the mindset of firms”.

Currently financial services do not always work well for consumers, the regulator said, and despite the current regime it has seen some practices that cause harm.

Such practices include presenting information in a way that exploits consumers’ behavioural biases, providing poor customer support or selling products the FCA deems not fit for purpose.

Introduction of the new Consumer Duty by the Financial Conduct Authority will be backed by “assertive supervision” and a “data-led approach” for intervention when it spots practices which do not deliver for consumers.

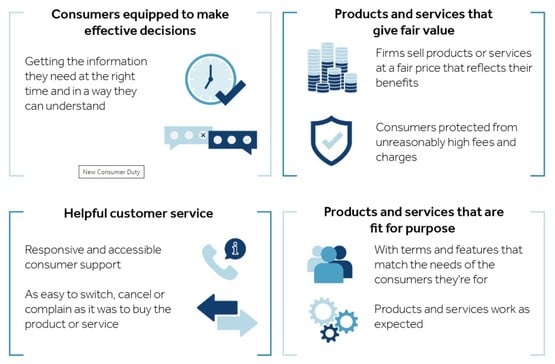

Its new ‘Consumer Principle’ is that “a firm must act to deliver good outcomes for the retail consumers of its products”.

The new rules will require firms to focus on supporting and empowering their customers to make good financial decisions and avoiding foreseeable harm at every stage of the customer relationship.

Firms will have to provide consumers with information they can understand, offer products and service that are fit for purpose and provide helpful customer service.

A second consultation is now under way until February 15, with the final rules being confirmed in July 2022.

Sheldon Mills (pictured), executive director of consumers and competition at the FCA, said: “Making good financial decisions is vital to financial well-being and trust, but too often consumers are not given the information they need to make good decisions and are sold products or services that do not offer the benefits they might expect.

“We want to change that. We’ve been working to set a higher standard for firms, to put more of the onus on them to act in their customers’ interests and get their products and services right.

“We want to change that. We’ve been working to set a higher standard for firms, to put more of the onus on them to act in their customers’ interests and get their products and services right.

“The new duty will drive a change in culture at firms. We expect firms to step up and put consumers at the heart of what they do and we’ll be holding senior managers accountable if they do not.

“The duty will also help create an environment for healthy competition between firms, encouraging them to be innovative in developing products and services that meet consumer's needs.”

In its consultation paper the FCA states that although all firms that have an impact on consumer outcomes will need to consider their obligations under the Consumer Duty regime, there is more onus on dealers and customer-facing businesses.

"We would generally expect firms with a direct relationship with the end user to have greatest responsibility under the Consumer Duty," the FCA said.

However firms will only be liable for their own activities.

Following the implementation period the FCA will expect existing contracts to be included in firms's compliance with the Consumer Duty on a forward-looking basis.

In January the FCA introduced revisions to its consumer credit rules which require dealers to be more open about the fact that they earn commission from selling finance, and which stamped out broker reward models which could be unfair to consumers.

AM Dealer Technology Guide

The AM 2025 Dealer Technology Guide enables UK motor retailers to read about a host of the latest software and hardware available from the industry's dedicated suppliers.

Keeping abreast of technology is a vital part of modern automotive retailing as the demands of customers and staff for rapid and efficient fulfilment only increases.

Industry suppliers have provided their highlights and summaries for the AM Dealer Technology Guide, and we give their web addresses to help you discover more.

Moreover, many of them will be at Automotive Management Live on November 12 at Birmingham NEC. Ensure you register to join us at our flagship exhibition.

Read now

An award-winning journalist and editor, with two decades of experience covering the motor retail industry, and accredited by the Institute of Leadership and Management (ILM) plus the National Council for the Training of Journalist (NCTJ)

As editor of AM since 2016, Tim is responsible for its media content, planning and production across AM's multiple channels, including the website, digital reports, webinars, social media and the editorial content of AM's events, Automotive Management Live and the AM Awards. His focus is on interviewing senior leaders of franchised dealer groups and motor manufacturer national sales companies to examine latest developments in UK motor retail.

production line")

Login to comment

Comments

No comments have been made yet.