November’s new car registration figures may be an indicator that the market is started to “rebalance itself” but market forces continue to favour used car retail, according to Cazana.

Director of valuations at the vehicle valuations and sales tool specialist, Rupert Pontin, believes that the Society of Motor Manufacturers and Traders’ (SMMT) data from last month – which indicated a 3% decline in registrations over the same period in 2017 – indicates that the impact of WLTP has now settled.

Pontin said: “This does not mean that WLTP and the removal of the Plug-In Car Grant will no longer affect the market, but it does suggest that the biggest changes are now passed.

“Year to date new car registrations are now running at 6.9% behind 2017 and it will be interesting to see whether there will be any sort of push before the end of the year during December to clear remaining stock or meet annual commercial targets.”

Here, Pontin gives his insight on the month’s trends and their impact on the used car sector:

Private registrations are consistent for the year recording a drop of 6.5% whilst fleet figures are down 7.3% and business registrations at 6.3% lower for the year.

Going forward new car supply looks set to be an issue for certain manufacturers as they catch up with the WLTP testing procedures and this may result in less pre-registration activity.

In turn that is likely to mean late plate used car values will continue to improve and used car stock is still short.

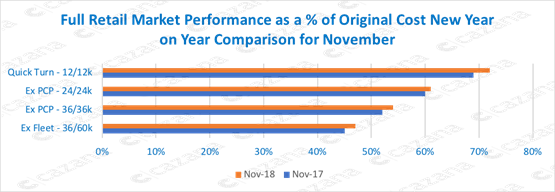

The chart below shows the overall market performance of key vehicle age profiles year on year:

It is clear from this top-level view of all vehicles and all fuel types combined at key age and mileage profiles that the used car market is short of stock as retail pricing across all key age and mileage profiles has increased.

It is clear from this top-level view of all vehicles and all fuel types combined at key age and mileage profiles that the used car market is short of stock as retail pricing across all key age and mileage profiles has increased.

The greatest increase in retail prices at three percentage points, is for the sub twelve-month old profile and this may also support the view that as pre-registration activity declines the lack of pressure from those cars sitting at the top of the market means that the desirability of sub twelve-month old cars is increasing and pulling prices up.

Retail pricing improvement for ex-PCP profile cars that has been a feature of the market in recent months continues and this chart shows a one percentage point increase at two years and twenty-four thousand miles and a two-percentage point increase at three years and thirty six thousand miles.

The rate of increase for these two profiles mirrors the October data and further supports the thinking that the greater volume of two-year cars coming back is mildly suppressing demand but purely due to increased choice.

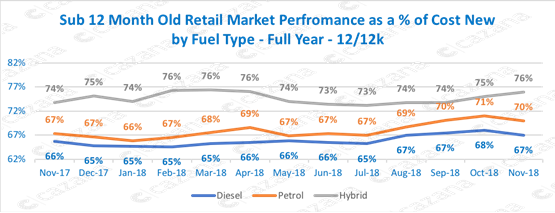

Given the greatest increase highlighted is in the sub twelve-month-old car profile the chart below looks at performance over the course of the year:

This chart is very interesting as it confirms the fact that there has been a marked increase in retail pricing for sub twelve-month old cars not only over the course of the year but specifically in the last five months.

This chart is very interesting as it confirms the fact that there has been a marked increase in retail pricing for sub twelve-month old cars not only over the course of the year but specifically in the last five months.

This is especially noticeable for hybrid cars which unlike petrol and diesel vehicles have continued to increase in price during November where the other fuel types have declined slightly.

Year-on-year hybrid cars have improved by two percentage points and diesel by one percentage point but it has been petrol powered cars that have shown the greatest year on year increase at three percentage points.

This is no doubt in part due to the petrol/diesel discussion but also at this age group there can be greater volumes of smaller cheaper cars I the market from all vendor sources.

It is also worth noting the delta between the different fuel types both now and at the same point last year.

The gap between petrol and diesel has widened by one percentage point whilst the difference between petrol and hybrid has narrowed by one percentage point.

This is probably due to the fact that there are more hybrids coming to the market and realistically speaking hybrids will in all likelihood decline in residual value as supply improves as they sit particularly high in relation to cost new at the moment.

However, there may be a hiatus in the coming weeks as new versions no longer attract support from the recently withdrawn Plug In Car Grant (PICG) as reviewed in last month’s market commentary.

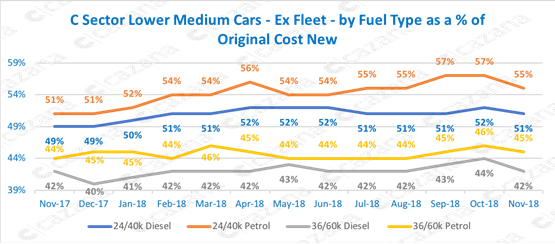

Market sentiment and anecdotal comment is always plentiful and one topic of late has been that there are too many C-sector cars coming to the market at the moment particularly as ex fleet profile vehicles.

There is currently discussion around the fact that wholesale values are being adversely affected and a suggestion that the retail consumer demand is not there for these cars.

Astra, Focus, 308 and Golf type cars are usually a firm favourite with the consumer and despite the influx of crossover SUV’s in recent years as alternatives they have remained popular.

The chart below shows the retail pricing performance for ex Fleet C-Sector cars over the past year:

This chart shows some interesting insight with no indication that retail pricing has decreased year on year for either petrol or diesel variants in the sector. In fact, lower mileage petrol and diesel cars have both increased in price with a four percentage point increase for petrol and two percentage point increase for diesel at forty thousand miles.

This chart shows some interesting insight with no indication that retail pricing has decreased year on year for either petrol or diesel variants in the sector. In fact, lower mileage petrol and diesel cars have both increased in price with a four percentage point increase for petrol and two percentage point increase for diesel at forty thousand miles.

At the higher mileage point, petrol prices reflect a one percentage point increase and diesel remain at the same level as November 2017.

This demonstrates that despite increased volume there is still good consumer demand for C Sector cars in the used market. It is key to remember that retail pricing is driven by what a consumer will pay for a car and therefore drives wholesale pricing more often these days.

Summary

The November market has been more difficult from both a new and used car perspective but this should not come as a surprise. In the run-up to the festive season consumer focus is on other things and the ongoing Brexit complications should not be underestimated as consumer confidence continues to remain low.

The balance of the year will see an improvement in used car interest towards the end of the month and new car registrations may see a boost once more as manufacturers and dealers seek to meet end of year targets to achieve full year bonus.

Login to comment

Comments

No comments have been made yet.