In the wake of the Society of Motor Manufacturers and Trader’s fully-year 2018 new car registration figures, Cazana valuations director, Rupert Pontin, delivers his market analysis for December, 2018.

With the new year now upon us, it is interesting to note that the level of optimism being expressed industry wide has not improved greatly as it usually does at the beginning of a new year.

There are still significant concerns over the economic position and the debacle that is Brexit.

Without some clarity and certainty, the country and indeed Europe cannot plan certain aspects of the future with any degree of certainty or accuracy.

As we draw ever closer to withdrawal from Europe with no deal in place, and only a weak deal being perceived as the only alternative, confidence continues to waver.

This means that opportunities in the used car market may well prove to be the best options for those buyers not prepared to gamble on a new car until Brexit provides more clarity and subsequent stability.

Whatever the final decision the economy needs to know to be able to prepare for what could be significant difficulty.

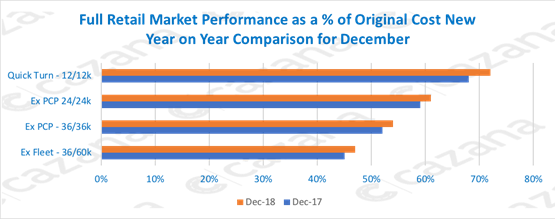

The chart below shows overall market performance of key vehicle age profiles year on year:

This chart compares retail pricing performance across key market profiles from December 2017 to December 2018 and the data incudes all cars and fuel types so is a generic view of the market.

This chart compares retail pricing performance across key market profiles from December 2017 to December 2018 and the data incudes all cars and fuel types so is a generic view of the market.

However, it is clear that in retail pricing terms the market is stronger than it was last year at all levels with a two-percentage point uplift across the board.

This reinforces the view that the market is suffering from a shortage of used car stock.

It is also interesting to note that the average cost new price across all profiles, except the three-year 60,000-mile ex-fleet sector, has dropped by up to 10%, the latter showing a minimal increase.

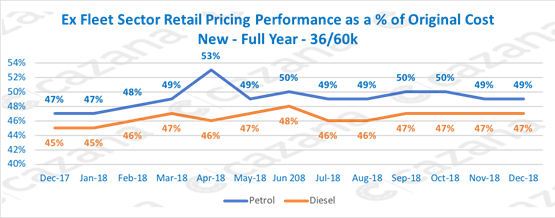

The chart below looks at the ex-fleet sector in more detail given that this area has been specifically affected by new car difficulties during the year:

The chart gives a very clear and consistent message. Despite anecdotal concerns that this area of the market has been difficult, it is obvious that retail pricing performance has followed a similar pattern for both petrol and diesel cars through the course of the year.

The chart gives a very clear and consistent message. Despite anecdotal concerns that this area of the market has been difficult, it is obvious that retail pricing performance has followed a similar pattern for both petrol and diesel cars through the course of the year.

The increase in retail pricing is consistent for both fuel types and the delta between the two in December 2018 at two percentage points, is the same as it was in 2017 confirming that there has been no punishment of used diesel values by the used car buyer.

There is an interesting blip in the data in April 2017 showing quite an uplift in pricing for petrol cars and a drop for diesel.

Given that this is for just one month it is likely to have been the result of a change in volumes being de-fleeted.

Overall the two-percentage point difference between the two fuel types has remained consistent for most of the year.

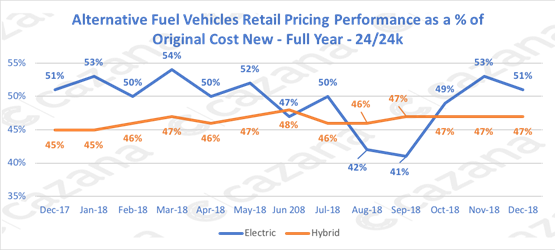

Finally, it would be remiss not to look at the performance of the only sector of the market that has posted a new car increase in registration volumes for the year.

Alternative Fuel Vehicles (AFVs) remain a hot topic of conversation in the trade and retail press, and discussions over the relevance of the power train continue.

The chart below shows the retail pricing performance for AFV’s over the past year:

The important point to acknowledge with this chart is that data volumes for AFV’s are much lower than for other propulsion types due to the reduced volume of cars registered in recent years.

The important point to acknowledge with this chart is that data volumes for AFV’s are much lower than for other propulsion types due to the reduced volume of cars registered in recent years.

The somewhat volatile movements for Electric vehicles are a direct reflection of the low data points and many of the changes in retail pricing reflect the type of product coming to the used market and this is dependent on de-fleet activity.

There is greater stability for the Hybrid models and this is due to greater acceptance by the used car consumer as much as it is based on the volume of data and type of car in the market.

It will be interesting to see how both fuel types perform during the course of 2019 and whether the used car consumer is as enthusiastic about these cars as many would have you believe the new car buyers are.

To summarise, the December market has been as expected for both new and used cars with lower footfall at the dealers and more challenging customers necessitating a tougher approach by the sales team.

Whilst days to sale increased slightly pricing was not the issue that many expected. The fact that stock was short for most of the month supported the firm stance that many dealers took when negotiating with retail consumers which is both encouraging and good news for the industry as a whole. This position is likely to continue for the best part of 2019.

Cazana’s truly live retail-driven data is unique in providing up to the moment market insight and intelligence being driven from over 25,000 websites each day.

Seeking more focussed information relating to specific market sectors or time periods ensures maximum vision and the most comprehensive insight required to maximise profit, ROI and asset management.

With the continuing Brexit confusion at an all-time high, top quality up to the minute commercial data will identify market variations quicker than any other data provider and will be vital to ensure modern automotive organisations are in a position to make the most effective strategic decisions.

Login to comment

Comments

No comments have been made yet.