New car registration data released by the Society of Motor Manufacturers and Traders (SMMT) for September saw a quantum shift from the August return that saw such an uplift in registrations.

This was, in the majority of cases, due to the introduction of the WLTP and the need to clear the stocks of old less environmentally friendly cars.

With registrations this month down by 20.5% this reflects the impact of selling cars that were not going to be able to be sold under the new regulations.

This has taken the year to date registration volume to 7.5% below the figure achieved by the end of September last year, which is on track with the Cazana full-year expectation of a market decline of 6.5% over 2017.

Looking at propulsion type, registrations for diesel cars reduced by a stunning 42.5% lowering market share for September 2018 to just 29% which is 10% less than the same period last year.

Conversely and unsurprisingly petrol cars took 64.1% of the market share with registration volumes down just 6.7%.

This left AFVs with 6.9% market share which is an increase of 3.9% representing the continued shift in customer demand to what is perceived to a better fuel type.

The September registration volume has been decimated by the lack of supply of new cars rather than a significant drop in consumer demand.

However, there are some who are citing that market demand has also been significantly affected by consumer confidence over Brexit and although this has a part to play, an element of poor planning on testing and production must also be partly to blame.

With so many changes to product supply and to the stated emissions, there is a high level of confusion in the market particularly for the business user whether they be fleet owners or company car drivers. Whilst the SMMT shows that market share between private sales and fleet sales has varied by just 1% in comparison to last year there is quite a story behind how these figures have been achieved.

The used market has been a different proposition and where consumer confidence has been lower, this has resulted in buyers seeking slightly cheaper cars on the basis they would like to save money.

There is little doubt that this has been good news for the OEM’s that have pre-registered so many cars as the problem has been shifted to a lower price point and thus far it would seem that consumer demand has just about kept up with supply.

With quieter months ahead though it may become a challenge for used car sites to ensure that sales meet budget aspirations.

It is possible that to keep stock moving there may be a reduction in retail pricing at the expense of margin as consumers begin to focus on autumn holiday time and the festive season beyond rather than buying cars.

Although these are usual seasonal factors considered and budgeted for by most businesses, with such change in the market this year it may prove to be a period of discomfort for some as competition increases.

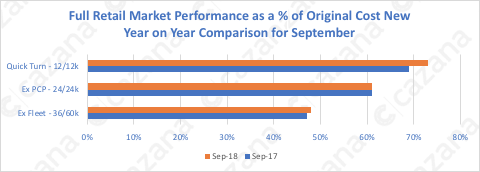

The chart below shows overall market performance of key vehicle age profiles year on year:-

Given the increase in pre-registrations of late, the trend of improving prices of Quick Turn cars in recent months was surprising as volumes had increased.

Given the increase in pre-registrations of late, the trend of improving prices of Quick Turn cars in recent months was surprising as volumes had increased.

However, following a month of drastically reduced new car sales, there is now an irrefutable reason for retail prices in this sector to have risen.

This trend may continue during the last quarter.

Stability appears to remain in the ex-PCP sector despite volumes increasing further but there is more to be revealed in the data on closer investigation.

The ex-Fleet sector has recorded an increase in retail pricing over the same period last year which is positive news and it is likely to be down to the fact that WLTP has caused distress in the new Fleet market hence affecting the supply of de-fleeted product to the used market.

Alternatively, this could reflect better consumer retail demand as buyers seek to save money as a result of Brexit concerns.

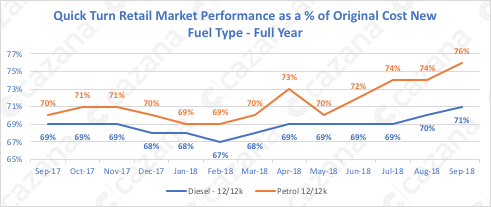

With values of the sub 12-month-old vehicles increasing of late the chart below looks at the data in more detail by fuel type:

The year on year increase in pricing for petrol cars is a significant 6ppts whereas for diesel the increase is 2ppts. The good news is the general shape of the chart for both propulsion types is similar and this quantifies the fact that there is not a problem with used diesel cars, in the same way, there is with new models.

The year on year increase in pricing for petrol cars is a significant 6ppts whereas for diesel the increase is 2ppts. The good news is the general shape of the chart for both propulsion types is similar and this quantifies the fact that there is not a problem with used diesel cars, in the same way, there is with new models.

The growth in the delta between the two fuel types is important as although diesel propulsion is not in trouble, retail pricing has not improved as much.

This is possibly due to the volume of cars in the market and without a doubt the type of car.

With so many changes to the new car market over the last few months, there is now a level of concern around what the impact of this changeable supply will have on the used car market in the years and months to come.

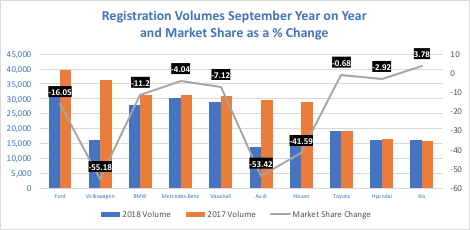

The chart below shows just how much of a shift there has been in new car registrations and market share for the top 10 manufacturers in September:-

With this level of change in the new car registrations and market share, it seems highly likely that used car buyers will find themselves being offered very different cars on the forecourt in the future.

Change is often seen as good and this period of adjustment may prompt customers to review the type of vehicle they really want or actually need to meet personal requirements when they find a limited supply of what they perceive to be the right car for them.

Author: Rupert Pontin, director of valuations, Cazana

Login to comment

Comments

No comments have been made yet.