A choking of new vehicle supply to dealers’ showrooms triggered by the September introduction of WLTP will continue to drive a buoyant used car market into 2019, according to Cazana.

Rupert Pontin, Cazana’s director of valuations, stated in his monthly report on the performance of the used car market that, despite a general lack of consumer confidence, the number of used retail buyers have been boosted by new car buyers unable to find the car they want.

“This has helped to dent the large volumes of pre-registered cars that hit the dealer websites in recent months”, he said, adding: “With new car supply set to be an issue for the foreseeable future this bodes well for used car dealers nationwide and where there had been an expectation that retail pricing may have dropped to stimulate demand resulting in narrower margins it would seem that the opposite is actually likely to be the case.

How has the introduction of WLTP affected your franchised car dealership? Click the tab to tell AM about your dealership's experience of managing the shift to WLTP and RDE fuel economy and emissions test regimes by taking this month's 'one minute' multiple-choice survey.

How has the introduction of WLTP affected your franchised car dealership? Click the tab to tell AM about your dealership's experience of managing the shift to WLTP and RDE fuel economy and emissions test regimes by taking this month's 'one minute' multiple-choice survey.

Here Pontin delivers his latest view of the UK used car market:

Here Pontin delivers his latest view of the UK used car market:

Data published by Cazana supports the view that the used car market is short of used stock overall and also enjoying a good level of retail consumer demand.

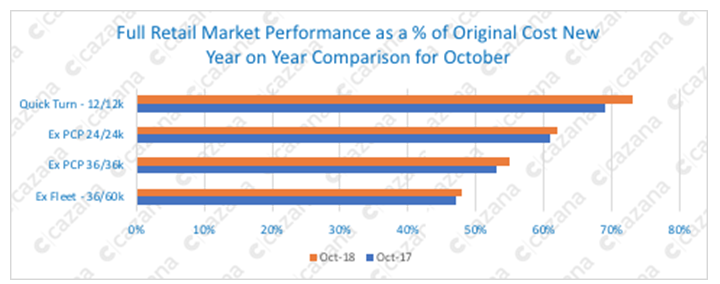

Retail price performance across all key sectors shows an increase in value as a percentage of original cost new with the best performing profile being the twelve-month-old vehicle with a four-percentage point increase when compared with the same month last year.

This is the result of the new car stock shortage with dealers able to achieve higher prices when selling to what were inevitably intended to be new car buyers.

There was also a two-percentage point improvement in retail pricing performance for three-year-old ex PCP cars.

Compared to the 1ppt increase at two years old, the lack of this profile of vehicle is resulting in good demand and stronger prices.

The lower improvement in two-year-old ex PCP product is possibly driven by higher volumes of this age and profile car coming to the market as dealers work to move customers to newer pre-registered cars creating a greater availability of two-year-old product.

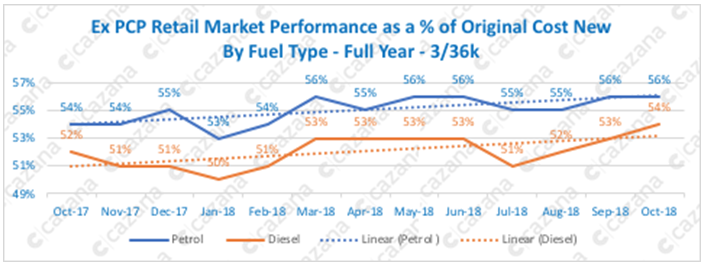

With values of the ex-PCP three-year-old vehicles increasing of late the chart below looks at the data in more detail by fuel type:

The previous chart shows the performance over the last 12 months of ex-PCP cars at three years old and thirty-six thousand miles by fuel type.

The previous chart shows the performance over the last 12 months of ex-PCP cars at three years old and thirty-six thousand miles by fuel type.

Whilst both petrol and diesel cars follow similar patterns for much of the year it is interesting to note that since July, diesel powered cars have been on a marked increase with retail pricing increasing by three percentage points whereas petrol powered cars improved by just one percentage point.

This could indicate that there is greater demand for older cheaper models or indeed that there are less of these cars in the market.

This would support the earlier suggestion that OEM’s are churning PCP contracts early to improve pre-reg sales.

The other important data in this chart is the relative positions of petrol and diesel models to each other during the course of the year.

In October 2018 as a comparison against October 2017 the delta between the two fuel types is exactly the same at two percentage points.

This shows consistency and strength. In fact, the trend line indicates that retail pricing has increased at the same rate although the performance line appears to show greater stability for diesel cars.

Given the significant increase of over 30% in Alternative Fuel Vehicle (AFV) registrations in October it would be remiss not to take a snap shot of this market.

As identified, this increase is due to the withdrawal of the government subsidy but it will be fascinating to see what impact this will have on the used car retail pricing of these cars going forward.

Taking into consideration the fact that new prices have now increased, the question is whether used prices will follow suit as the gap between new and used pricing will expand.

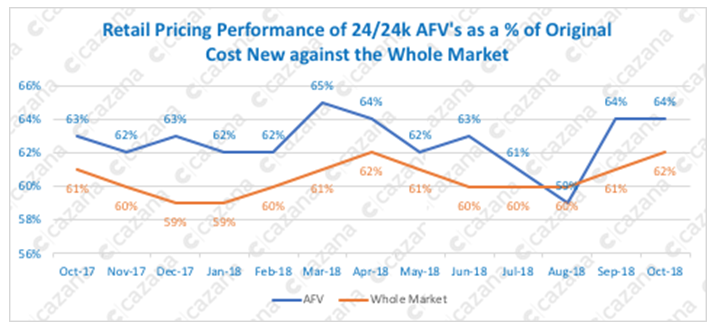

The chart below shows the retail pricing performance for ex PCP AFV’s over the past year:

This chart compares retail pricing performance as a percentage of original cost new for AFV’s against the performance of the rest of the market at the same age and mileage profile.

The interesting point here is the fact that AFV retail pricing as a percentage of cost new sits higher than the other fuel types combined.

Naturally it is encouraging to see that generally speaking, pricing trends mirror those of the rest of the market which indicates that up until this point AFV’s have been striking a chord with the retail consumer.

It is also worth highlighting that despite a less stable journey, AFV’s have retained the two-percentage point uplift in retail pricing over the rest of the market.

To summarise the October market is in some ways straightforward.

With a further decline in the new market the used car market has continued to perform well. At this stage Cazana’s data science-driven insight gives no reason to suggest this will change, although there is a caveat.

If the government are unable to secure a Brexit deal and the chancellor is forced to return to parliament with another budget proposition then the state of the economy will in all likelihood be compromised.

At this point the political and economic landscape is likely to see a significant change, the likes of which are not really forecastable.

Login to comment

Comments

No comments have been made yet.