Ahead of the Society of Motor Manufacturers and Traders (SMMT) publication of Q1 new car registrations figures, AM takes a look at February's trends and how Russia “threw a hammer and sickle into the works” of automotive's 2022 recovery.

In a month where the world seems to have gone mad, perhaps it is only to be expected that the car market seems to be operating at an entirely random level.

Not only is Kia now the UK’s best-selling marque and MG is now outselling the likes of Land Rover, but the pattern of manufacturer sales increases and falls is unprecedented.

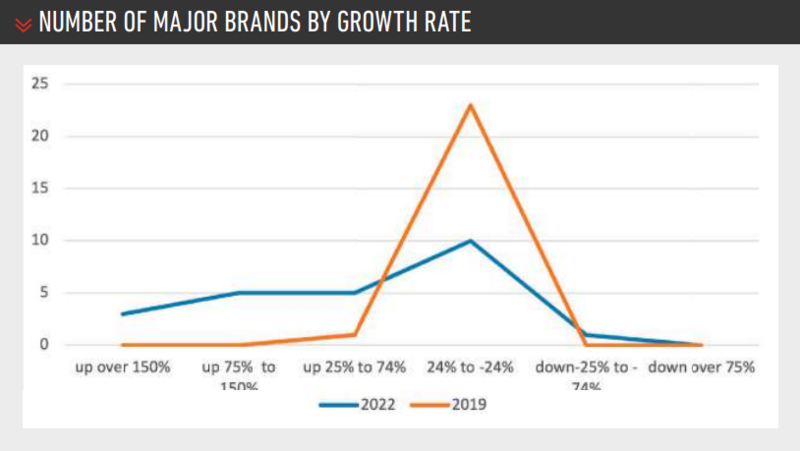

Traditionally, the car market (and pretty well all others) follows what is called a “normal distribution” – most manufacturers’ sales increases/decreases are close to the market average, and the further away from the average you get, the smaller the number of manufacturers.

Of course, what counts as “normal” has been increasingly hard to define since Brexit, but if we take year-to-date (YTD) 2019 as the last pre-COVID year, we can see that the car market followed the expected pattern (see graph).

Of course, what counts as “normal” has been increasingly hard to define since Brexit, but if we take year-to-date (YTD) 2019 as the last pre-COVID year, we can see that the car market followed the expected pattern (see graph).

However, YTD 2022 shows no pattern at all. Of the 24 major marques (brands with more than 1.0% market share), eight have grown by more than 75%, compared with none at all in 2019.

In a market that was only up by 23.0%, that is remarkable. 2022 also saw a larger number of manufacturers with big falls compared with 2019.

The reason may be partly linked to lumpy supply, as manufacturers try to catch up with demand with cars going straight from ports to dealers.

Now Russia has thrown a hammer and sickle into the works, making the situation even worse.

MG said on March 1 that it was “temporarily” telling its dealers to stop taking orders for petrol cars.

At least that move seems to be in line with overall market trends: Auto Trader is reporting a spike in electric vehicle (EV) searches as a response to rising oil prices.

Certainly, there is no sign of the traditional response to rising fuel prices – i.e. buy a more economical diesel. Diesel sales have fallen by 34.6%, with market share slumping from 18.9% YTD 2021 to 10.1% YTD 2022.

Premium brands still sell a reasonably large number of diesels – approximately 20% of total sales for BMW and Audi, but most manufacturers are far lower. The only outlier is Land Rover, 41% of which are still diesel.

One would expect a brand that concentrates on large SUVs to have a relatively high diesel percentage, but it leaves something of a chasm between where Land Rover is now and where it needs to be by 2030.

Quite a number of brands have a diesel proportion of either zero (Nissan, Mini, MG, Honda, Fiat) or close to zero (Toyota, Hyundai).

Quite a number of brands have a diesel proportion of either zero (Nissan, Mini, MG, Honda, Fiat) or close to zero (Toyota, Hyundai).

In terms of the overall market, it is as much a question of supply as demand. The war in Ukraine is affecting crucial raw materials (e.g. nickel for batteries, palladium for catalysts and neon for microchip production), but Ukraine had also become a significant assembly location for Tier 1 suppliers.

It manufactured a large number of wiring harnesses, and also had some factories making key electronic components.

One supplier told us it had two weeks’ supply in the system at the start of the war. If it was to try to start production in a western European factory, it would need eight weeks for “soft tooling” (tools that can last a year or two before wearing out) or 16 weeks for “hard tooling” that will last the lifetime of the product.

Of course, the value of the tools already in Ukraine would have to be written off. The only alternative would be to try to source from parallel factories in China, but existing factories cannot suddenly double output.

Returning from geopolitics to the here-and-now of the UK car market, the fastest growth has been seen in superminis, which have developed at double the rate of the overall market (46.5%).

This may not reflect any change in demand, but rather a reflection that a lot of manufacturers switched production in 2021 to more profitable larger cars, reducing supermini sales.

Until Putin destroyed their plans, car manufacturers had been expecting the chip shortage to ease this year, so production of small cars had been on the rise.

At a manufacturer level, the big news is obviously the market leadership position of Kia.

At a manufacturer level, the big news is obviously the market leadership position of Kia.

Kia is not going to hold that spot for long, but it would be a mistake to dismiss its 8.2% market share as just a statistical quirk.

Kia might be doing well partly because it has greater availability, but every new customer it sells to now is one more customer brought into the Kia fold.

If it can keep them in the fold in three years’ time, then it has a great platform to build on.

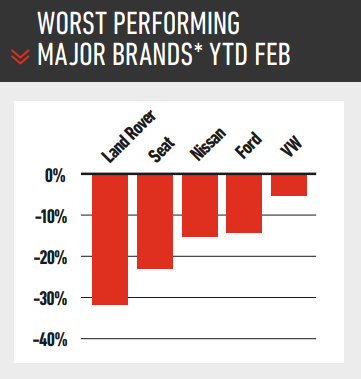

In second place is BMW – another unprecedented result. Of the other top 10 manufacturers, the biggest growth has come from Hyundai (100.6%), although that is more a case of recovery after some poor years, than underlying growth. Notable is the name not in the top 10 – Nissan, whose Sunderland factory is the jewel in the crown of British manufacturing, is in 12th position (down 15.4%).

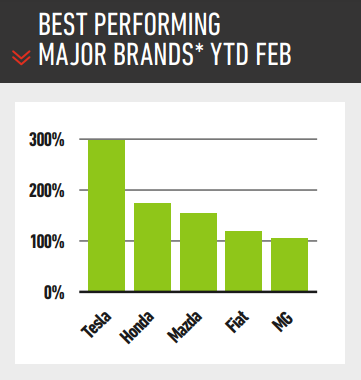

Outside the traditional brands, Tesla continues to make huge progress.

Outside the traditional brands, Tesla continues to make huge progress.

Tesla does not officially report its sales, hiding coyly in the “Others” category of the SMMT (appreciating that the word “coy” is not normally attached to Elon Musk). However, it is not hard to deduce its market share, which is 1.5% YTD, with the Model Y and the Model 3 both in the top 10 for the month of February.

As for next month, the bigger volumes of the March registration plate change might flatten out some of recent fluctuations. On the other hand, supply problems could mean a very weak March. As a film producer once said about Hollywood: “No one knows anything”.

Author: David Francis

AM Dealer Technology Guide

The AM 2025 Dealer Technology Guide enables UK motor retailers to read about a host of the latest software and hardware available from the industry's dedicated suppliers.

Keeping abreast of technology is a vital part of modern automotive retailing as the demands of customers and staff for rapid and efficient fulfilment only increases.

Industry suppliers have provided their highlights and summaries for the AM Dealer Technology Guide, and we give their web addresses to help you discover more.

Moreover, many of them will be at Automotive Management Live on November 12 at Birmingham NEC. Ensure you register to join us at our flagship exhibition.

Read now

Login to comment

Comments

No comments have been made yet.