February has not served to install car retailers’ used vehicle operations as “the shining star” in their business in recent months and news of HMRC VAT reforms will only make life tougher, according to Cazana.

In his monthly used car market update, the vehicle marketing and data specialist’s director of valuations, Rupert Pontin, shares his observation of a month where stock is traditionally in short supply as the new ‘plate change approaches.

To be clear, used car demand was still there but closing the customer has been more difficult and, interestingly, it was not solved by offering a discount on price.

It would appear that the commitment to buy is around confidence in personal circumstances and what effects there may be from the upcoming Brexit conundrum.

Common sense tends to prevail and the deal is done but it is interesting to observe this behavioural pattern and work with a subjective and emotional viewpoint.

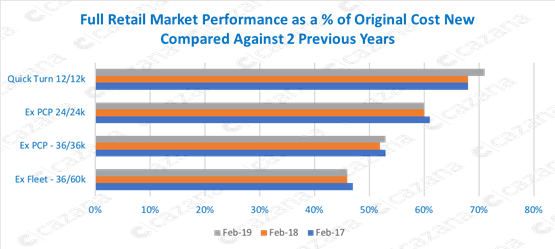

Used car prices remain buoyant

This chart highlights the fact that used car retail pricing has not fallen at sector level when comparing with the same period in 2018.

This chart highlights the fact that used car retail pricing has not fallen at sector level when comparing with the same period in 2018.

Whilst prices for ex PCP cars at 24k and ex Fleet cars at 60k have mutually dropped by one percentage point since 2017, the year on year comparison shows either parity in pricing or an increase of between one and two percentage points market wide.

However, detailed analysis always gives a clearer picture.

It is also interesting to note the positive impact on pricing in the quick turn sector as a result of the drop in pre-registration activity.

Likewise, the strength of pricing for three-year-old ex PCP cars is also of interest and perhaps reflects a shortage of used car stock.

This is probably due to the propensity for OEM’s to take customers out of PCP deals as soon as the value of the customer’s car matches or marginally exceeds the current value, giving the opportunity to generate a new car sale.

This therefore goes part way to explaining why ex PCP cars at 24 months old have stayed at the same pricing point as a percentage of original cost new as there are clearly more examples in the used car market.

On the topic of PCP’s the recent announcement by HMRC to change the VAT treatment of PCP deals was something of a surprise.

It will be interesting to see how this affects the new car market in the first instance and in time how this will affect the used car customer.

For the time being the PCP market looks vibrant although the previous chart did highlight parity of retail pricing at 24 months old.

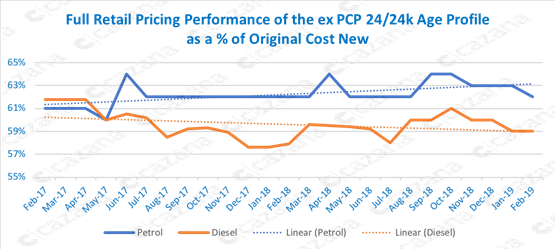

Petrol vehicle show RV strength

This chart gives better clarity to the performance of ex PCP cars over the past 2 years and it is obvious that there is now greater residual value strength in petrol cars at this age and mileage profile.

This chart gives better clarity to the performance of ex PCP cars over the past 2 years and it is obvious that there is now greater residual value strength in petrol cars at this age and mileage profile.

In February 2017 diesel powered vehicles had a one percentage point premium over petrol which has now swapped to a three-percentage point premium in favour of petrol cars.

The chart also demonstrates the steady performance of petrol propelled vehicles in contrast to diesel models over the period and the trendlines highlight the pricing patterns for both fuel types.

Ultimately this graph demonstrates that detailed analysis gives better insight and as such a competitive advantage.

Diesel-powered vehicles have in fact dropped as a retail price percentage of original cost new by some 3ppts.

It will be important to monitor this going forward as this may be the beginning of a downward trend in used diesel car values although it may be due to volumes in the market.

With Brexit almost upon the country and evidence of consumer concern over the future of the economy on a backdrop of poor news from the car manufacturing sector in the UK, the strength of the new and used market must be seen in a positive light that in many ways contradicts what is often seen in the national press.

Last month we showed a consumer confidence chart depicting the behaviour patterns of consumers over the preceding 12 months.

Despite the fact that the automotive sector out performed this pattern it is wise to be aware of the economy as a whole and factor in potential changes as the month passes.

Consumer demand prevails

In conclusion, February brought good new car registration news for the industry at a time when many would have the country believe the economy and prospects are in dire straits.

The used car market whilst more challenging, has also been encouraging and this is made clear by the resilience and stability of used car pricing which just would not have behaved in the way it did if there was no retail consumer demand.

The coming month will be a busy new car period although used car activity will ramp up as the days pass and retail pricing is likely to remain firm which will naturally drive wholesale demand and trade prices.

Login to comment

Comments

No comments have been made yet.