By Philip Nothard

Monthly year-on-year gains and a record half-year for new car registrations have given the industry plenty to shout about and made for some eye-catching headlines. However, behind the top-line figures, we have a more complex picture.

It’s clear that dealers are under pressure on their retained margins and the annual increases are not wholly due to natural private registrations. The market is becoming more diverse at all levels.

Naturally, as an industry, we begin to wonder how sustainable the current volumes are and what the impact will be when all these vehicles hit the used market. Will the European markets recover to take some of the strain?

Away from the big trends, smaller franchised dealers are wondering how much more pressure their balance sheets, and cash flow, can take. Dealers are looking to manufacturers to provide low rate finance, generous deposit contributions, and strong new car offers to help the situation. This is largely concentrated around PCP, with suspected subvented GFV (guaranteed future values).

The generous offers on new cars are having a knock-on effect on used, as consumers want to see deals that match the marketing they see on TV or online. How often do used car departments hear ‘’I can buy a brand-new car for less per month than you are quoting me this used car”.

Pre-registration is also having a profound effect on the used market, as smaller franchised or used dealers are unable to compete. Take this example from a well-known website: a pre-registered 2015 Golf 1.4TSI for £19,150 versus in the same search results as an identically specced 2014/64 plate with 5,000 miles, for £345 more.

If you were a consumer in the market for this car, which one would you choose? And that is without comparing the finance payments on offer.

Such are the volumes of stock, that we are seeing the words ‘pre-reg’ popping up in adverts and features in the national press advising motorists on the best deals.

A recent AM-online poll asked ‘’what percentage of your new car business each month is pre-registration?’’, and just under a quarter of those responding indicated it was as high as 11-20%.

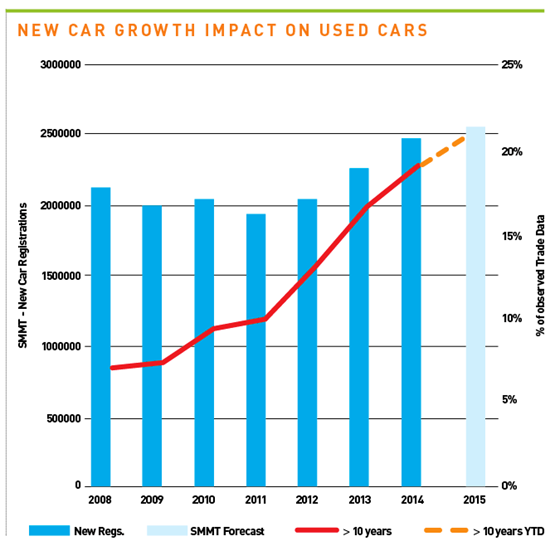

The graph, left, shows how registrations have risen since 2011 alongside CAP’s observed disposal data on the volumes of 10-year+ used cars, which have risen from single digits to the low twenties today, and continue to trend upward. What impact is this level of registrations having on the overall volume of the aged used cars on the road?

The graph, left, shows how registrations have risen since 2011 alongside CAP’s observed disposal data on the volumes of 10-year+ used cars, which have risen from single digits to the low twenties today, and continue to trend upward. What impact is this level of registrations having on the overall volume of the aged used cars on the road?

Does an increasing ageing used vehicle parc and the pressures on older, inefficient vehicles make the case for another scrappage scheme? Ageing vehicles are struggling to find a home at the auctions as dealers shy away from the time it can take to make these vehicles retail-ready.

There are no short-term fixes to the challenges these pressures create within both markets and if there is going to be another scrappage scheme, it won’t be anytime soon. Many are looking or already offering the consumer alternatives to the PCP offers they see from the manufacturers and working with finance companies to ensure used PCP is visible.

While pre-registrations can hurt retained margins, many dealers are taking a strategic approach to managing their way through the issue.

It’s clear the market for new and used is undergoing some seismic changes and the dynamics between both markets are shifting. So while our industry will continue to make headlines for the rest of the year, it also creates opportunities for the dealer with a keen eye on the market and pricing.

Login to comment

Comments

No comments have been made yet.